MagnifyMoney

It’s 2020, and if you want dinner delivered to your doorstep or a date for Friday night, rest assured, there’s an app for that. Financial apps in particular have flooded online app stores, all angling to helping you save, spend and invest your hard-earned cash.

Banks have gotten in on the action, too. From megabanks like Wells Fargo and Bank of America, to digital-only platforms like Simple and Aspiration, everybody is pushing their customers to join the app-based ecosystem.

MagnifyMoney has been rating apps of the largest banks and credit unions since 2014, back when only one-third of Americans with cell phones engaged in mobile banking. As we usher in a new decade, not only have banking apps become as ubiquitous as smartphones themselves — one survey found that after checking the weather and social media, banking apps are what smartphones access the most — our research has shown they’ve also become more sophisticated, with users becoming increasingly satisfied with their mobile experience.

For the 2020 ranking of the best mobile bank apps, we recorded nearly 20 million app user ratings on the Google Play and the Apple App Store (in December 2019). The overall MagnifyMoney score for each app is based on these ratings, via a weighted average of iOS and Android ratings that factored in the number of reviews on each platform.

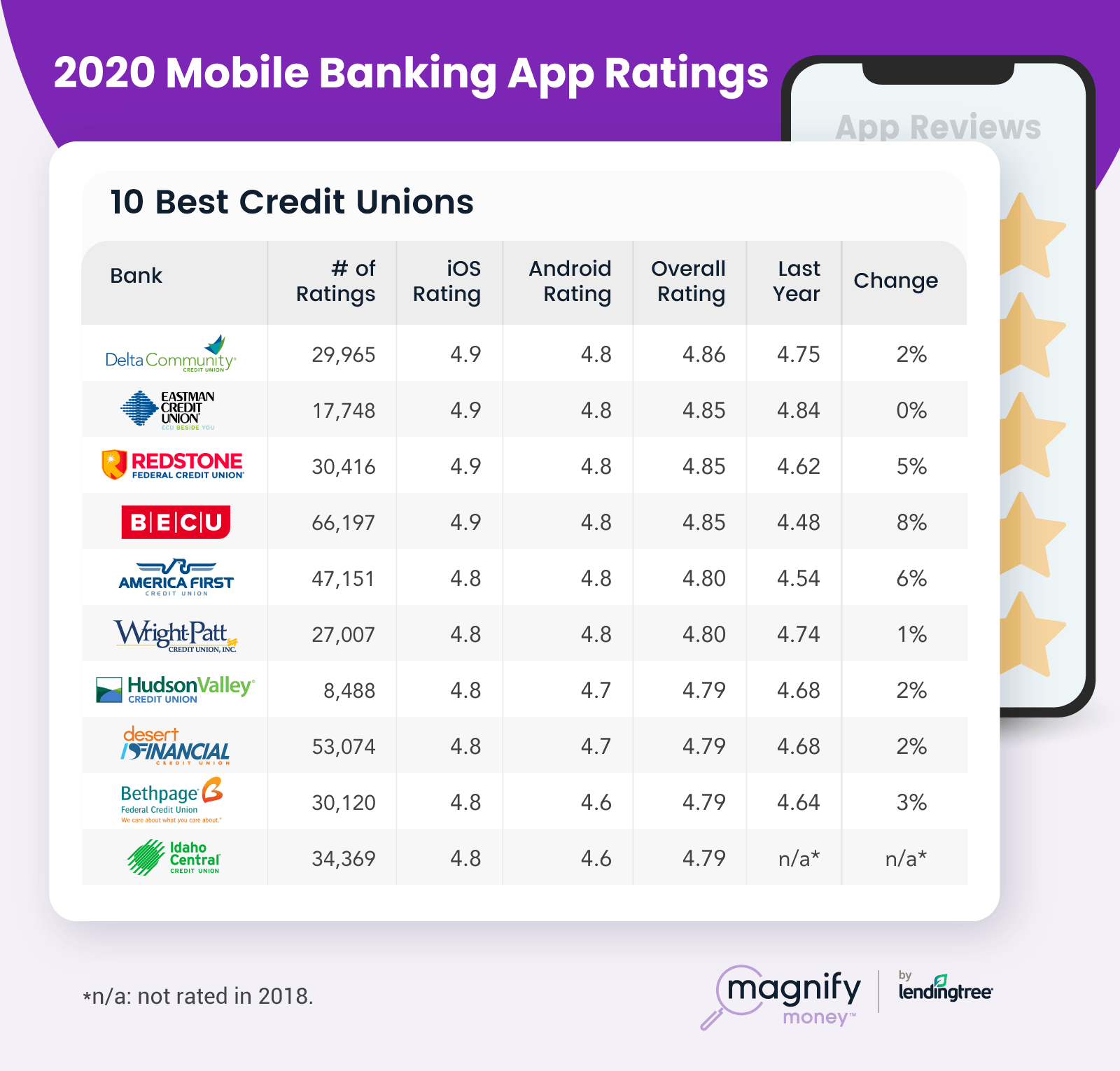

The Delta Community Credit Union has the best overall bank app for 2020, taking the title from Discover Bank, the reigning champion for the past two years. Delta Community Credit Union’s 29,965 app reviews boasted an average iOS rating of 4.9 and an average Android rating of 4.8, resulting in an overall MagnifyMoney score of 4.86. That’s a 2% increase from last year’s score.

The Delta Community Credit Union has the best overall bank app for 2020, taking the title from Discover Bank, the reigning champion for the past two years. Delta Community Credit Union’s 29,965 app reviews boasted an average iOS rating of 4.9 and an average Android rating of 4.8, resulting in an overall MagnifyMoney score of 4.86. That’s a 2% increase from last year’s score.

The Atlanta-based Delta Community Credit Union was established in 1940 by a group of Delta Airlines employees. It has since grown to be Georgia’s largest credit union, with over 400,000 members and 29 branches. Membership eligibility includes factors like living in certain areas of Georgia (mainly in the Atlanta metro area), working for a select group of companies or belonging to one of several organizations.

Delta Community Credit Union’s app includes features that allow users to review their balances and transactions, transfer funds between accounts, pay bills, view copies of cleared checks and locate ATMs. Reviewers of the app on the iOS app store have applauded it, writing that with “every upgrade it gets better” and that the app is “simple” and “clear.”

Other close contenders for the top spot of the best overall banking app for 2020 include Eastman Credit Union, Redstone Federal Credit Union and BECU, all of which had MagnifyMoney scores of 4.85.

Credit unions have had an interesting history with mobile technology. For years, many eschewed mobile apps altogether, since they were quite costly for smaller financial institutions to implement. However, credit unions that embrace technology often hit it out of the park with their customers, who tend to be very loyal. In fact, the only non-credit union institution to crack the top 10 for the best overall bank app for 2020 was Discover Bank, which took ninth place, with an average ranking of 4.79.

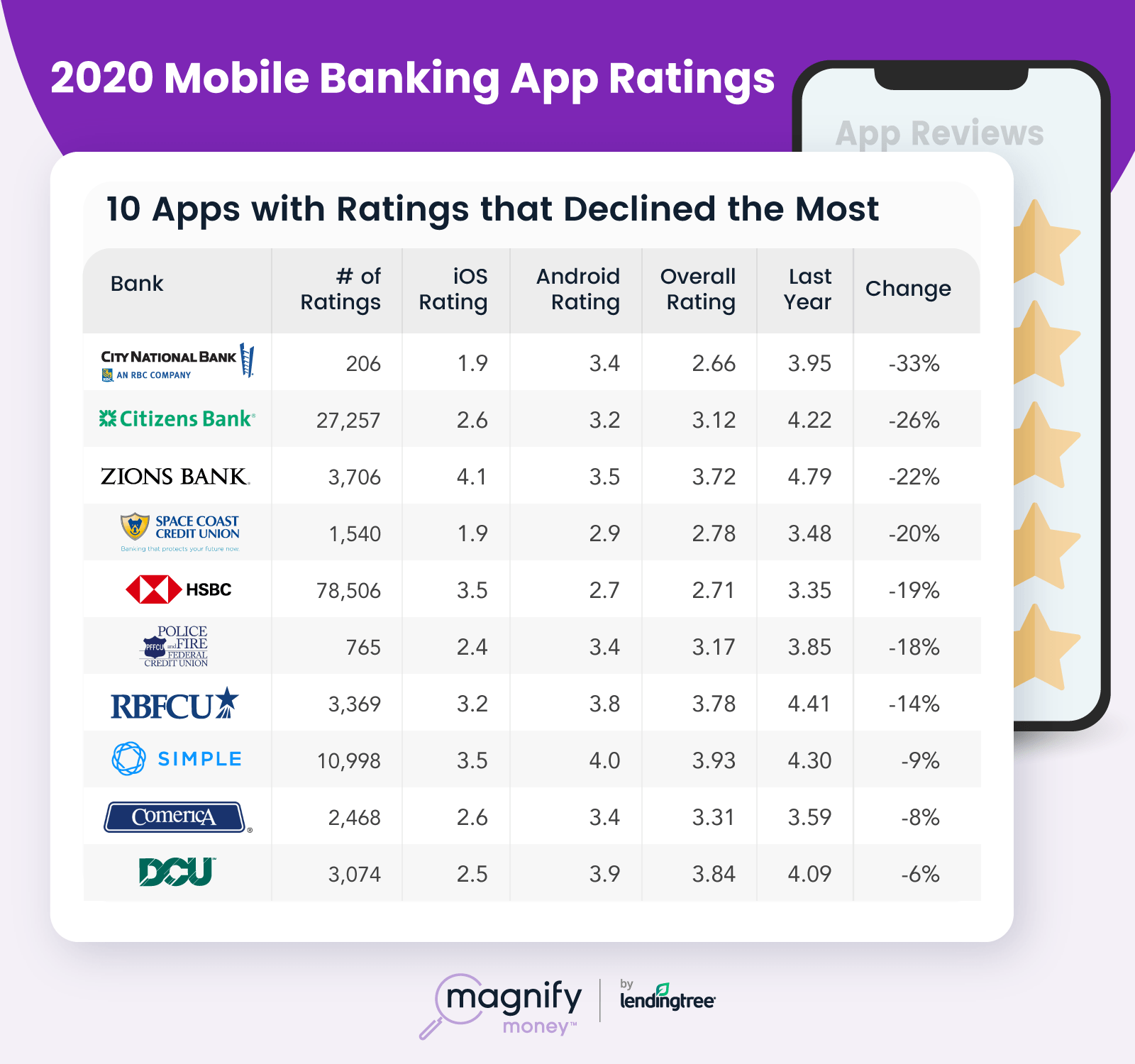

") MagnifyMoney’s annual ranking of the best mobile bank apps would not be complete without acknowledging the apps that just don’t stack up. Overall, the worst bank app for 2020 comes from City National Bank. Out of the bank’s 206 reviews, it had an overall iOS average rating of 1.9 and an average Android rating of 3.4, resulting in an overall score of 2.66. That’s a 33% decline from last year’s score of 3.95.

MagnifyMoney’s annual ranking of the best mobile bank apps would not be complete without acknowledging the apps that just don’t stack up. Overall, the worst bank app for 2020 comes from City National Bank. Out of the bank’s 206 reviews, it had an overall iOS average rating of 1.9 and an average Android rating of 3.4, resulting in an overall score of 2.66. That’s a 33% decline from last year’s score of 3.95.

Founded in 1954, Los Angeles-based City National Bank is a subsidiary of Royal Bank of Canada. The bank has 73 offices and 19 full-service regional centers in a slew of cities across the U.S., and boasts over 60 billion in assets. Its app features a number of features typical for mobile banking apps, including viewing account balances and transaction history, transferring funds, paying bills, depositing checks and personalizing accounts.

However, users of the app slammed it in reviews on the iOS app store, saying they consistently get error messages when trying to launch the app, with one reviewer even calling it “the worst banking app ever.”

Also making the list for worst overall bank apps for 2020 are HSBC (with an overall score of 2.71), San Diego County Credit Union (2.74), Space Coast Credit Union (2.78) and Star One Credit Union (2.9).

The top spot for the best big bank app of 2020 is a tie between Wells Fargo and BB&T. For this study, we defined big banks as those institutions having the largest deposits per FDIC data from June 2019. Note, however, that Wells Fargo and BB&T tied only a hair ahead of the competition — many of the apps from the largest banks had overall scores within a few percentage points of each other. This suggests that many customers are broadly satisfied by the banking apps offered by the largest institutions.

The top spot for the best big bank app of 2020 is a tie between Wells Fargo and BB&T. For this study, we defined big banks as those institutions having the largest deposits per FDIC data from June 2019. Note, however, that Wells Fargo and BB&T tied only a hair ahead of the competition — many of the apps from the largest banks had overall scores within a few percentage points of each other. This suggests that many customers are broadly satisfied by the banking apps offered by the largest institutions.

Wells Fargo had a massive 3,582,112 reviews, with an average iOS rating of 4.8 and an average Android rating of 4.7, resulting in an overall score of 4.79 — the same score it had last year. BB&T had 342,506 reviews and the same average ratings and overall score as Wells Fargo, tying for the top spot.

Down the list, other big banks present included Citibank (with a MagnifyMoney score of 4.78), Bank of America (4.77), U.S. Bank (4.75), PNC Bank (4.75), TD Bank (4.71), Capital One (4.70) and Chase (4.63). While the ratings of many of the big banks remained relatively unchanged from the prior year’s survey, there were some highlights: Bank of America appears to have listened to its customers, as its app’s MagnifyMoney score improved 13%.

On the flip side, one notable slide was the Chase app. With the largest user base of any mobile banking app — we counted more than 3.6 million ratings — Chase’s MagnifyMoney score slipped 1% in the 2020 ranking, earning it the ninth place ranking among apps from the big banks this time around.

The big outlier among the list of 10 big bank apps was SunTrust, with a MagnifyMoney score that paled in comparison to its peers. SunTrust had 67,276 reviews, an average iOS rating of 4.1 and an average Android rating of 4.4 — earning it a MagnifyMoney score of just 4.35. It’s worth noting, though, that it’s a 5% increase from SunTrust’s score in the 2019 edition: 4.14.

The big outlier among the list of 10 big bank apps was SunTrust, with a MagnifyMoney score that paled in comparison to its peers. SunTrust had 67,276 reviews, an average iOS rating of 4.1 and an average Android rating of 4.4 — earning it a MagnifyMoney score of just 4.35. It’s worth noting, though, that it’s a 5% increase from SunTrust’s score in the 2019 edition: 4.14.

SunTrust offers all the bells and whistles that are commonplace for banking apps, such as viewing account balances, transactions and making payments, but reviewers complained that the app is constantly unavailable without notice, and that it lacks functionality.

One reason for SunTrust’s shabby service could be chalked up to the bank’s forthcoming merger with BB&T. The two banks reportedly plan to merge and operate under the new name Truist. The merger has been in the works for over a year, and a possible reason for SunTrust’s lack of investment in its app could be due to increased allocation of resources on its merging efforts. Note that BB&T tied for first in our study of the best big banking apps of 2020.

We looked at the 50 largest credit unions by assets, according to September 2019 data from Credit Union National Association (CUNA). As noted above, Delta Community Credit Union was crowned the best bank app for 2020 overall, so it also wins the category as the best large credit union app.

Credit unions that came close to Delta’s overall score of 4.86 included Eastman Credit Union, Redstone Federal Credit Union and BECU, who all had MagnifyMoney scores of 4.85. Credit unions trailing the top spots included America First Credit Union and Wright-Patt Credit Union, who both had MagnifyMoney scores of 4.80. Hudson Valley Federal Credit Union, Desert Financial Credit Union, Bethpage Federal Credit Union and Idaho Central were not far behind, with overall MagnifyMoney scores of 4.79.

As noted above, credit unions swept the competition in 2020. Our study found that the average overall MagnifyMoney score for bank apps was 4.05, but for credit unions it was 4.15.

Despite being the best of a very good field this year, credit unions still offer some clunkers. In particular, San Diego County Credit Union is the worst large credit union app of 2020, with an iOS average rating of just 1.8 and an average Android average rating of 2.8, resulting in a MagnifyMoney score of 2.74. This app also ranked as the third worst bank app of 2020 overall. Originally chartered in 1938, San Diego County Credit Union says it now has over 8.3 billion in assets and over 400,000 members.

Despite being the best of a very good field this year, credit unions still offer some clunkers. In particular, San Diego County Credit Union is the worst large credit union app of 2020, with an iOS average rating of just 1.8 and an average Android average rating of 2.8, resulting in a MagnifyMoney score of 2.74. This app also ranked as the third worst bank app of 2020 overall. Originally chartered in 1938, San Diego County Credit Union says it now has over 8.3 billion in assets and over 400,000 members.

While the app says it allows its members to access their accounts, make deposits, transfer funds and pay bills, users slammed the product in their reviews. Common complaints were that the app was extremely slow and there were issues with logging in.

Other large credit unions that came close to San Diego County Credit Union’s poor score include Space Coast Credit Union, with a MagnifyMoney score of 2.78, and Star One Credit Union, with a score of 2.9.

When you’re a bank that only exists online with no physical branches, it stands to reason that your mobile app product needs to be well above average. For this category, we ranked the 10 largest online banks, and as in prior years Discover Bank wins for the most highly rated app. Discover Bank had an impressive 2,513,870 reviews, an average iOS rating of 4.8 and an average Android rating of 4.6, resulting in a MagnifyMoney score of 4.79 — the same score it had last year.

When you’re a bank that only exists online with no physical branches, it stands to reason that your mobile app product needs to be well above average. For this category, we ranked the 10 largest online banks, and as in prior years Discover Bank wins for the most highly rated app. Discover Bank had an impressive 2,513,870 reviews, an average iOS rating of 4.8 and an average Android rating of 4.6, resulting in a MagnifyMoney score of 4.79 — the same score it had last year.

Discover Bank is a full-service operation that offers everything from checking accounts to IRA CDs. Its app has standard features, like being able to see account information and deposit checks, but also has a number of noteworthy tools, such as facial recognition, plus the ability to spend cashback bonuses or miles at online stores. In reviews, app users gush about Discover’s customer service and the app’s great features.

Other large digital-only banks that deserve honorable mentions for their high scores include Aspiration Summit, with a MagnifyMoney score of 4.78, State Farm Bank (4.71) and Ally Bank (4.68).

Unfortunately, being a virtual bank doesn’t mean you have a great app. In fact, two of the 10 digital-only banks we looked at actually saw a decrease in their MagnifyMoney score from last year: Go Bank, which fell 2% to a MagnifyMoney score of 4.25, and Simple, which slid 9% to a MagnifyMoney score of 3.93.

Unfortunately, being a virtual bank doesn’t mean you have a great app. In fact, two of the 10 digital-only banks we looked at actually saw a decrease in their MagnifyMoney score from last year: Go Bank, which fell 2% to a MagnifyMoney score of 4.25, and Simple, which slid 9% to a MagnifyMoney score of 3.93.

Indeed, Simple ranks as the worst large, digital-only bank app for 2020. Ironically, Simple says it was designed especially with its mobile app in mind, and says while you’ll be able to access many of its features on its web interface, customers will get the most from Simple with its mobile app.

Simple’s app includes features like automated budgeting, automated savings tools, photo check deposit and more, going above and beyond the standard features offered by many bank apps. However, reviewers of the app have complained about updates that ended up hurting the user experience — for example, one that swapped one navigation tool for another, less efficient one — and poor customer service. Simple, apparently, isn’t that simple to use.

With each new year brings a new opportunity to improve, and many bank apps showed up for the challenge. For 2020, the most improved bank app goes to TIAA Bank which saw an eye-popping 94% increase in its MagnifyMoney score from last year. In the 2019 edition, TIAA Bank — then named EverBank, had a really poor MagnifyMoney score of 2.30. A year later, TIAA Bank’s app is getting an average iOS rating of 4.6 and an average Android rating of 4.4, for a MagnifyMoney score of 4.46. One possible reason for the sudden shift in app performance? TIAA Bank acquired Everbank, and under new ownership there was likely a renewed focus and attention on the app.

Other bank apps that showed the most improvement for 2020 include OnPoint Community Credit Union, which saw a 72% increase in score from last year, followed by TCF Bank (71%), American Airlines Federal Credit Union (70%), Hancock Whitney (62%) BBVA Compass (61%), Webster Bank (58%), Associated Bank (52%), and BMO Harris and First Citizens (both at 45%).

While a number of bank apps took significant strides, a good chunk of them also spiraled downward. The most deteriorated bank app for 2020 goes to City National Bank, also named the worst overall bank app for 2020. Since last year, City National Bank experienced a swift downfall, dropping from last year’s MagnifyMoney score of 3.95 to 2.66 — a 33% decrease in score.

City National Bank has company, though, with other bank apps facing some serious deterioration in 2020. The second most deteriorated app is Citizens Bank, with a 26% decrease since last year, followed by Zions Bank (22% decrease), Space Coast Credit Union (20% decrease), HSBC (19% decrease), Police and Fire Federal Credit Union (18% decrease), Randolph-Brooks Federal Credit Union (14% decrease), Simple (9%), Comerica Bank (8% decrease) and DCU (6% decrease). If you’re interested in learning more about our choice for top online savings account options read our review here.

App ratings from the Google Play (Android platform) and the App Store (Apple iOS platform) were recorded December 2019, and the overall MagnifyMoney score combines the user ratings of each. Overall ratings are a weighted average of iOS and Android ratings based on the number of reviews for each platform. Institutions with no mobile apps were excluded from ranking summaries.

The 50 largest banks, defined as those with the largest deposits per FDIC data June 2019, with a mobile banking app available on Google Play and the Apple Store were examined. Those without meaningful consumer checking product offerings were excluded. The 50 largest credit unions by assets according to the CUNA in September 2019 were also examined. A separate category ranks the 10 largest online direct banks defined by the number app ratings.

Sarah Berger

Sarah BergerSarah Berger is a former writer at LendingTree, where she covered personal finance, specifically focusing on challenges and opportunities facing millennials. Before joining LendingTree, she was a writer for CNBC and Bankrate.

Read More