MagnifyMoney

You’ve heard this line over and over again: To be smart with your money, you need to both build your savings and invest. The savings part is easy: Stash money away in a savings account — a little at a time — to pay for particular goals, like an emergency fund or a new car. Investing is a different story, and learning how to buy securities that will grow in value over time isn’t quite so simple.

Investments are made for the long term, and investing involves taking on risk. That might make you nervous, but investing is essential for your financial health. Compound interest and market gains can help your money grow a much higher rate than a savings account, helping you build long-term wealth for your retirement.

The idea of investing might be intimidating, but don’t worry, it’s not as hard as you think. In fact, you can learn how to invest and get started in just five simple steps.

When you’re young, time is on your side. That’s especially true when it comes to investing. And the earlier you start the better, according to Brandon Renfro, a certified financial planner and an assistant professor of finance at East Texas Baptist University.

“Earnings from investments compound over time,” Renfro said. “The longer you give yourself to earn that compound return, the more money you will have when you reach a goal, such as retirement.”

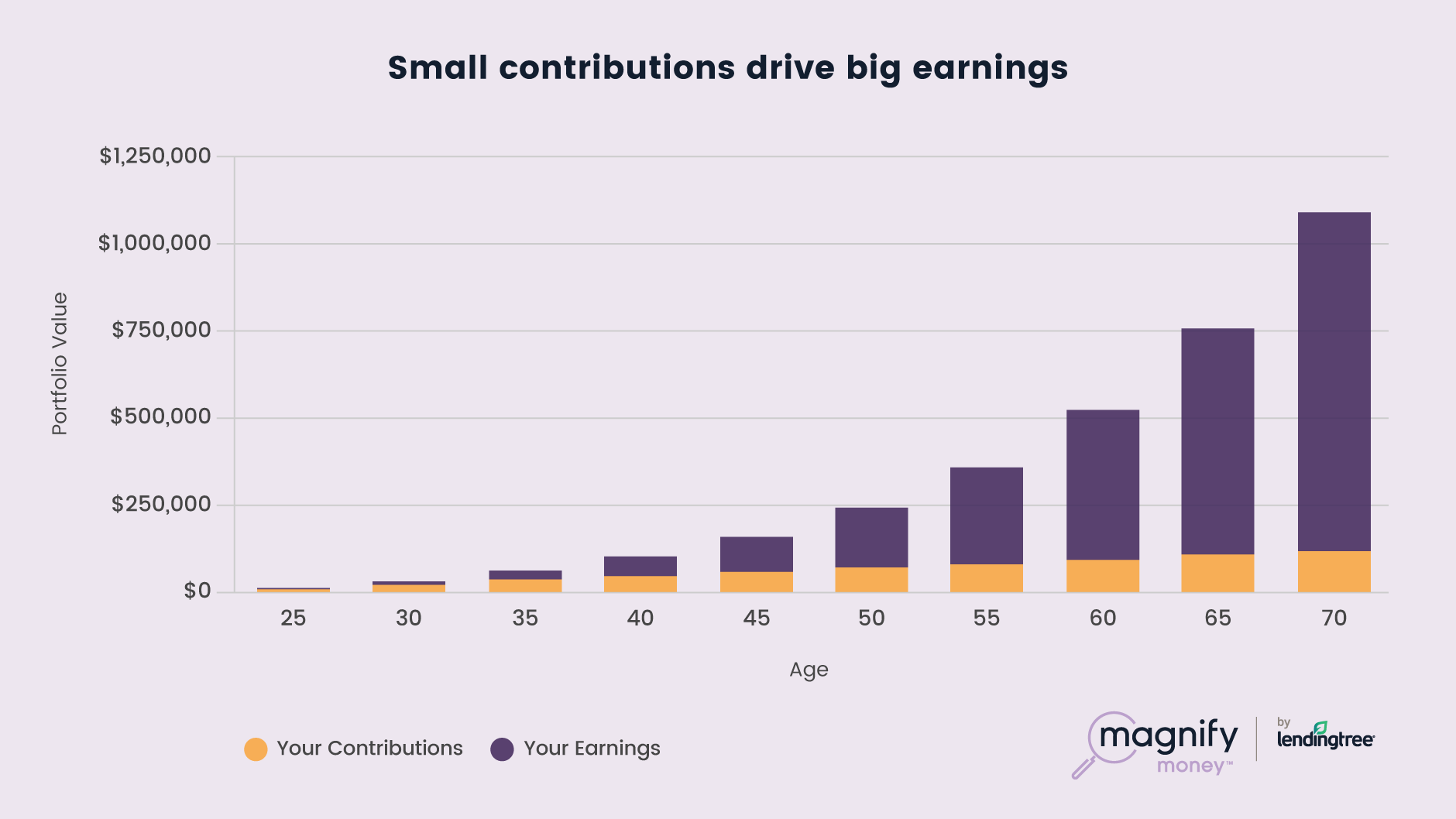

Returns from your investing start slow, but compounding yields big gains over the long term. Let’s say that you start investing $200 per month at age 25 at a 7% annual return. After five years, you would have saved $12,000 and earned only $2,400.

However, if you keep adding $200 to your investing portfolio every month until age 70, you’ll have contributed $120,000—and earned almost $976,000, for a total portfolio value of $1.1 million.

You don’t always get a steady return on your investment, as in the example above. The market fluctuates, moving up and down, dramatically sometimes. But over the long term, the market produces regular returns. According to the financial firm Morningstar, the long-term average return from the stock market is near 10%.

Investing while you’re young allows you to ride out any short-term losses so you can take advantage of gains over the long-term. Even if the market dips over the near term, over the 20- to 30-year time frame, you’ll see reliable growth rates.

When deciding how much to invest, it’s important to take your goals into consideration. If you have high-interest debt or if you don’t have an emergency fund, it may make more sense to pay down your debt and build a small savings account before you invest.

After that, think about your long-term goals, such as planning for retirement. You’ve likely heard experts recommend that you save millions of dollars, but don’t let that scare you. When you’re just starting out, it’s important to start saving whatever you can and to keep contributing consistently.

Vanguard, one of the biggest investment companies, recommends that you save 12% to 15% of your income for retirement. If that sounds impossible right now, save what you can afford, even if it’s just $25 per month. Over time, those small amounts will snowball, helping you build a sizable nest egg.

If your employer offers a 401(k) retirement plan and matches contributions, try to contribute enough to qualify for the full match.

When you’re ready to start investing, it’s important to think about what kind of account you want to open. There are three core investment account types:

According to Natalie Pine, a certified financial planner and managing partner of Briaud Financial Advisors, IRAs and employer-sponsored accounts are strong starting points.

“There is no wrong way to save, but when you are young, a Roth IRA, 401(k), 403(b) is a great option,” Pine said. “You pay low taxes now and have tax-free growth for the rest of your life and the lives of your beneficiaries.”

Once you’ve chosen an account structure, you can think about what type of asset classes and investments you want to make. There are several different investment options:

Next, think about your investment strategy. Consider your own risk tolerance. Some people are comfortable taking on more risk, thinking it’s worth it to potentially see high returns. Others get panicky when they see the market dip, and prefer more conservative investments that offer lower, steadier returns. Choose an investment strategy that works for your comfort level.

The most important part is simply getting started. “While it is important to plan, don’t let the details overwhelm you to the point of inaction,” advised Renfro. “It’s better to get started now understanding just the basics than to keep putting it off.”

According to Pine, consistency is key to your success as an investor.

“With regard to investing, consistency is essential to avoid emotions driving decisions that ultimately lead to poor performance,” she said. “If you stick with a system, whatever that may be, you are more likely to weather various storms than if you trade around a lot and catch investments at the wrong time.”

Making regular contributions will help you build long term wealth. When you’re short on cash each month, finding extra money to invest may feel impossible. However, there are different strategies you can use to invest, even if you don’t have a lot of cash:

Kat Tretina

Kat TretinaKat Tretina is a freelance finance writer and certified student loan counselor based in Orlando. Her work has been featured in publications like The Huffington Post, Entrepreneur, Forbes, and more.

Read More