MagnifyMoney

Captrust is a fee-based financial advisory firm headquartered in Raleigh, N.C. Named one of the nation’s largest registered investment advisory firms by Financial Advisor magazine, Captrust has a 20-year history of serving emerging and affluent investors, including a deep commitment to community-based initiatives in the cities the firm serves. Our Captrust review takes a deep dive into the firm’s services, fees and more.

Captrust might be best suited for:

- Emerging investors who’d like access to more comprehensive financial planning.

- High net worth investors who prefer all-inclusive wrap fee programs.

| Assets under management: $655,054,291,754 | |

| Minimum investment: $50,000, but can be waived | |

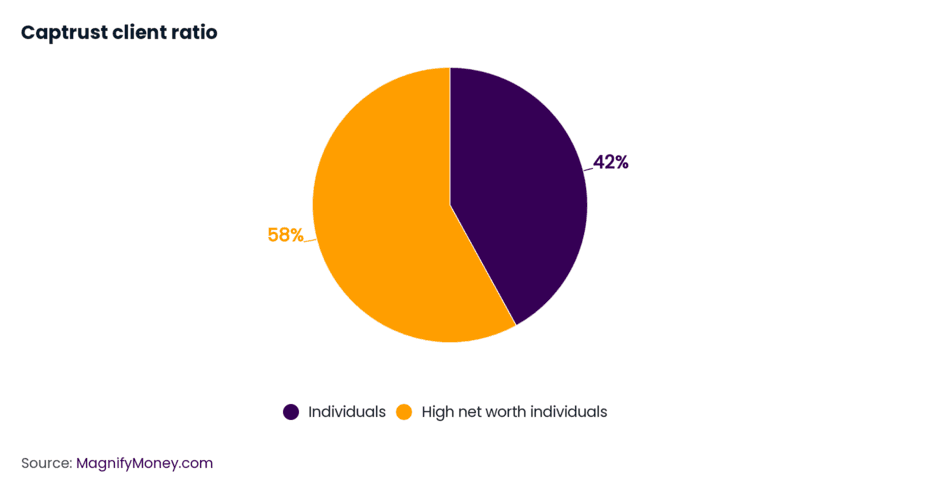

| Individual investor-to-advisor ratio: 38:1 | |

| Fee structure: A percentage of AUM, fixed fees, hourly charges, performance-based fees | |

| Headquarters: 4208 Six Forks Road, Suite 1700 Raleigh, NC 27609

Phone: 800-216-0645 |

All information included in this profile is accurate as of Aug. 4, 2022. For more information, please consult Captrust’s website.

Captrust is one of the largest advisory firms in the US, with over $600 billion in assets under management (AUM). Based in North Carolina and with offices throughout the U.S., the firm boasts a roster of 520 advisors nationwide who manage roughly 20,000 client accounts.

Fielding Miller, CEO of Captrust, founded the advisory firm in 1986. As a broker, Miller grew discontent with conflicts of interest undermining the integrity of client-advisor relationships. As a result, Miller founded Captrust, offering investors fee-based investment services instead of the more familiar commission-based business model. Captrust continues to pride itself on offering objective investment advice and fulfilling its fiduciary duty.

While not the ideal firm for new investors just starting their investing journeys, Captust could be the ideal fit for:

Captrust’s AUM fees are slightly higher than the industry average. For example, MagnifyMoney recently examined financial advisor fees and found that the average AUM fee was between 0.59% to 1.18%. With Captrust, AUM fees range from 1% to 2.25%, with smaller accounts bearing the brunt of higher fees.

| Captrust AUM fees by account size* | ||

|---|---|---|

| $0-$500,000 | Up to 2.25% | |

| $500,001-$1,000,000 | Up to 2.00% | |

| $1,000,001-$2,000,000 | Up to 1.75% | |

| $2,000,001-$5,000,000 | Up to 1.25% | |

| Over $5,000,001 | Up to 1.00% | |

However, if you have substantial assets with the firm, you can opt into the firm’s wrap-fee program. While these programs vary by firm, they typically include all custodial fees, commissions and more. It’s important to ask your Captrust advisor for full details of their wrap-fee program benefits.

| Captrust AUM wrap fees by account size | ||

|---|---|---|

| $1 million+ | Up to 2.25% | |

| $4 million+ | Up to 1.75% | |

| $5 million+ | Up to 1.25% | |

Captrust offers the typical suite of services you’d expect to find in a firm this large, including but not limited to:

As with all firms we review, Captrust is a fiduciary, which means advisors must always put your interest above their own. With that in mind, let’s have a look at how advisors at Captrust may invest your funds.

Captrust’s Form ADV is fairly vague on its investment strategies and relies on standard industry verbiage. They use common types of asset research, such as quantitative and qualitative. They also mention that you might receive a custom asset allocation or be a fit for one of the firm’s pre-built investment portfolios managed by their Investments Committee. Because of the lack of detail, we recommend asking detailed questions when you meet with your Captrust advisor to explore how they would manage your assets.

And while the firm is a fiduciary, your advisor may receive compensation for certain products they recommend — which is perfectly normal.

Many Captrust advisors serve as broker-dealers, meaning they may earn a commission on securities they recommend. Additionally, advisors may earn a commission on the sale of life insurance products. Captrust also acts as a consultant for three Excelsior funds and receives 50% of those funds’ management fees as compensation.

None reported in the past 10 years.

If you’re an emerging or affluent investor looking to partner with a nationwide advisory firm, Captrust’s capabilities could be worth exploring. However, your client experience will likely depend on your advisor and ability to justify the firm’s higher-than-average fees against other firms offering similar services.

And if for any reason Captrust isn’t the right fit for you and your needs, MagnifyMoney can help match you with an advisor. The form below will start a simple process to connect you with the trusted financial professional that you and your money deserve.

Alani Asis

Alani AsisAlani Asis is a former staff writer at MagnifyMoney covering investments, financial advisors and retirement. Alani previously contributed to Business Insider, Clever Girl Finance and Sound Dollar.

Read More