MagnifyMoney

Perhaps you’ve heard of Venmo, a PayPal-owned social payments platform that caught like wildfire among millennials, and serves as a popular way for people to split the bill. The digital peer-to-peer (P2P) payment service is ubiquitous to the point of being a verb — “Venmo me” — but that’s not stopping the big banks from making a play for the market.

In 2017, the banks responded with Zelle, a P2P transaction platform that can process payments between accounts at different banks within minutes, for free. When using apps like Venmo, PayPal and Square Cash, consumers may have to wait up to two or three days to access deposits in their bank accounts or pay a fee for instant access.

Zelle is a peer-to-peer payment service created by Early Warning Services, a company owned by Bank of America, BB&T, Capital One, JPMorgan Chase, PNC Bank, U.S. Bank and Wells Fargo. Zelle users can send, receive or request money directly to and from friends’ and family members’ bank accounts using only an email address or phone number, even if the other party has an account with a different bank. Zelle claims to process payments between accounts at different banks within minutes, for free.

As of this writing, Zelle partners with more than 65 banks and is accessible to more than 85 million U.S. consumers through its partners’ mobile banking applications. If your bank isn’t partnered with Zelle, you can still create an account using the Zelle app to send, receive and request money much like other P2P payment services.

Zelle, formerly known as ClearXchange, has grown rapidly since it’s rebranding and rollout to banking applications in 2017. It’s now a serious competitor in the P2P space. Early Warning reported the payments company processed $75 billion in payments in 2017. Meanwhile, its main competitor, Venmo, processed more than $40 billion in payments on its free mobile app in the 12-month period ending March 31, 2018. Early Warning said Zelle processed more than $25 billion in the first quarter of 2018, and Venmo processed $12 billion in the same period.

Zelle is advertised as a service for sending money to friends, family and people you know personally. The company does not offer a protection program for purchases or sales made through its platform, and neither do its participating financial institutions.

If you initiate the transfer, you are not covered for fraud by Zelle or your bank. For example, if you send someone money for event tickets using Zelle and it turns out the tickets are fake, there is no recourse against the person via Zelle or your bank, and you will lose your money like this woman did.

However, consumers are not liable for “unauthorized activity,” like if someone else uses Zelle to hack into your bank account. Zelle provides fraud protections as required by the Federal Reserve’s Regulation E.

Know the recipient personally

Sending money on Zelle is akin to handing cash to someone. To avoid losing your money to a fraudster, ensure you are only sending money to people you know and trust.

Confirm the recipient’s information

Zelle transactions cannot be disputed or reversed, so you want to double-check with the recipient that you’re using the correct email address or phone number. If you initiate a transaction to the wrong person, Zelle has no obligation to help you get your money back.

Enroll with only one bank

To avoid delays in sending and receiving funds using Zelle, make sure the email and/or phone number you want to use is only enrolled at one bank or credit union, and that it matches what the bank has on file.

If the same phone number and/or email is registered with your Zelle profile at more than one institution, you may run into issues sending and receiving payments using this service. Money sent to you using the phone number or email address you provide friends and family may be sent to the wrong bank account or to an old Zelle account. The funds may also get held up until you sort out the mix-up.

If you were previously enrolled in ClearXchange or the Zelle app before your bank integrated Zelle into its banking app, you may already have an active Zelle account using your phone number and/or email. If you want to enroll in Zelle with your bank, you’ll first need to contact customer support team and deactivate your old account there.

Zelle plays up its ease of use: Because it’s integrated into mobile banking apps, customers of banks using Zelle can use a single app to schedule bill pay, make deposits and complete fee-free P2P transactions. That means users don’t have to download an extra app to use Zelle on a mobile device, unlike stand-alone apps like Venmo and PayPal. Zelle does, however, have a stand-alone app, if you’d prefer to use that.

Zelle withdraws money directly from the sender’s bank account and deposits it directly into the recipient’s bank account. Users can send, request or receive money using an enrolled email address or mobile phone number.

On your mobile banking app

Zelle works a little differently on each of its partners’ mobile banking apps, but the main steps to send money are the same.

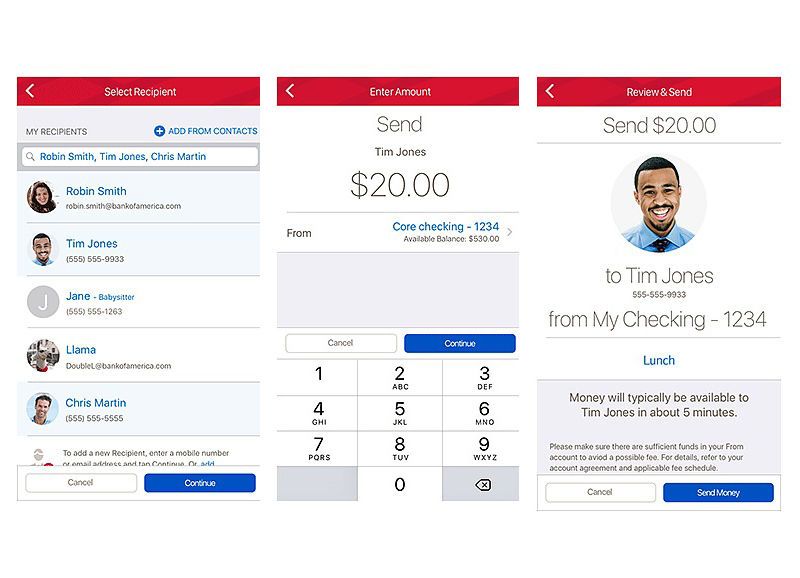

You’ll first select a recipient from (either from your contacts list or by adding them manually) and whether you’re sending money to them using their phone number or email address. Then, you enter the amount you want to send. At that point, you may have the option to set a sending date and add an optional note. Then, hit send. Your recipient should get a notification and see the funds in their bank account within minutes.

Here are some examples of how this service has been integrated into mobile banking:

Send money on Chase mobile app

Send money on Bank of America mobile app

Split expenses with Zelle on Bank of America mobile app

Sending money on the Zelle app

To reach customers whose banks aren’t part of the Zelle network, Early Warning partnered with Mastercard and Visa to make a Zelle app that allows transfers to those at nonparticipating banks and just about everyone with a U.S.-based debit card. However, at least one person involved in a Zelle transaction must have access to it through their bank or credit union.

Sending money on the Zelle app is similar to using other P2P apps like Venmo.

When someone sends you money using Zelle, the funds should show up in your bank account within a few minutes, unless it’s your first time using this service.

If you’re not already enrolled with Zelle, you should get an email or text saying someone sent you money using Zelle. You’ll then need to follow the enrollment instructions to get set up with the service. After you’re enrolled, it may take up to three days to receive the money in the bank account associated with your profile.

Zelle transfers money directly between U.S. bank accounts. Transfers occur typically within minutes, unless the recipient is not already enrolled in Zelle. If the recipient is not yet enrolled, it may take up to three business days for the money to become available in their bank account.

There are no limits to the amount of money you can receive, but there may be limits on how much money you can send, depending on your bank and the type of account you’re using. Zelle recommends you contact your bank or credit union to learn about any sending limits.

For example, Chase caps transfers from personal checking accounts at $2,000 per transaction, and customers can send up to $2,000 a day and $16,000 in a calendar month. However, customers sending money from a Chase Private Client or Private Banking client account can send up to $5,000 per day and $40,000 per calendar month.

If your institution doesn’t offer Zelle and you use the Zelle app, Zelle bases your weekly send limit on your track record using the app.

There are no fees to use the service. The company recommended you confirm with your bank or credit union that there are no additional fees.

No credit card transactions: You won’t be able to send money using a credit card at all; you can for a 3% fee on Venmo.

No international transfers: As of this writing, Zelle’s system doesn’t support international payments. The service only works with U.S.-based bank accounts, so you won’t be able to send money directly to family abroad. However, if you are traveling and have access to your bank account overseas, you can receive transfers made to your U.S.-based bank account.

By leveraging its network of bank partnerships, Zelle claimed consumers should be able to make transactions between different institutions within minutes. However, if your recipient does not have access to Zelle through their bank or credit union, or their partnered bank does not yet support real-time payments, Zelle loses its advantage. Transactions would then take between one and three days to complete, no better than the likes of PayPal or Venmo.

When you send money to a friend using Venmo, they instantly receive that amount as their Venmo balance, but then need to initiate a bank transfer to access the funds. The same goes for PayPal and Square Cash. With Popmoney, a service that sends money directly between bank accounts, there’s no need to initiate a deposit, but it takes a couple of days for the transactions to clear. With these services, it can take one to three days for a deposit to become available in your bank account.

Though Zelle touts transaction speed as one of its greatest strengths. While the instant transfer feature made the company stand out when it first rolled out in 2017, its competitors weren’t far behind. The Cash App, by Square, Inc. offers instant access to transferred funds for a 1.5% fee of the deposit amount, PayPal and Venmo both offer instant transfers for $0.25 per transfer.

What also made Zelle stand from the crowd was its free instant transfers. But now Google Pay offers that, too. Money sent using a debit card or Google Pay balance is transferred instantly to the person’s debit account — if it’s set as their default payment method — for free.

There are several ways you can can send money to friends, family members or the person you picked up your coffee table from on Craigslist. They range from social media options like Snapcash or Facebook Messenger, to full-fledged mobile and web apps like the PayPal app or Google Wallet.

Here’s how some of the big players in the P2P payments space to compare with Zelle:

| Feature | Zelle | Venmo | PayPal | Square Cash | Popmoney | Google Pay Send | Facebook Messenger |

|---|---|---|---|---|---|---|---|

| Who you can send money to | Anyone whose bank offers Zelle (85 million consumers) or anyone who is set up with the Zelle app | Anyone with a Venmo account | Anyone with a PayPal account (237 million customer accounts) | Anyone with a Square account | Anyone at any of nearly 2,500 financial institutions | Anyone; no need to have a Google account or the Google Pay Send app | Anyone with a Facebook account who is 18+ years old |

| Time it takes deposit to become available in recipient’s bank account | Minutes, unless the recipient’s bank doesn’t support instant transfers or isn’t a partnered institution | 1 to 3 business days after transferring from Venmo account to bank. Instant transfers for a fee of $0.25 per transaction. |

Transfers made before 7 p.m. EST typically arrive the following business day. Transfers made after 7 p.m. EST or on weekends or holidays will typically arrive on the second business day. Instant transfers are available for a fee of $0.25 per transaction. |

Up to 3 business days. Instant deposits are available for a fee of 1.5% of the deposit amount. |

Up to 3 business days | Money received transfers automatically to your default payment method Funds are available typically within minutes if a debit card is set as your default payment method Transfers to a bank account may take up to three business days |

Up to 5 business days |

| Has a stand-alone app | Yes. In addition, this service is integrated directly into existing bank mobile apps. | Yes | Yes | Yes | No. PopMoney is integrated into existing mobile banking apps | Yes | Yes |

| Has a web version | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Fees | None | Free to send money from a bank account or debit card 3% fee to send money from a credit card $0.25 to make an instant transfer |

Free when you send funds via a bank account 2.9% plus 30 cents (U.S.) of the amount you send using a debit or credit card $0.25 to make an instant transfer |

Free to send money from a bank account or debit card. 3% fee to send money from a credit card |

Free to receive money or pay a request $0.95 to send or request funds |

None | None |

| Accepts credit card transactions | No | Yes | Yes | Yes | No | No | No |

| Transaction limits | None, but your bank may impose transfer limits | Send up to $2,999.99 per 7 days after identity verification; no receiving limit. Cash out up to up to $19,999.99 per week after identity verification. |

Send and receive up to $10,000 per transaction | Send up to $2,500 a week after identity verification; receive more than $1,000 per 30 days after identity verification | Daily transaction limit for a debit card: $500 Daily transaction limit for a bank account: $2,000 30-day transaction limit for a debit card: $1,000 30-day transaction limit for a bank account: $5,000 |

Send up to $9,999 per transaction or up to $50,000 in 5 days If you live in Florida, you can send up to $3,000 every 24 hours |

Unclear. The terms and FAQs say nothing about limits, and Facebook did not respond to our request for information. A community forum post from 2016 says you can send up to $9,999 within 30 days |

| Supports international transfers | No | No | Yes – Fees for sending in other currencies vary | No | No | No | No |

| Lets you store funds on an in-app account | No | Yes | Yes | Yes | No | Yes | No |

| Fraud protection | None if you, the consumer, initiated the transfer. You are covered if someone makes an unauthorized transaction on your Zelle account if reported within 4 days after learning of the unauthorized transaction. |

Venmo does not offer buyer or seller protection.

You are covered if someone uses your Venmo account to make an unauthorized transactions if reported within 60 days. |

Yes: Paypal offers purchase protection to buyers and sellers of goods and services for claims reported within 180 days Paypal covers unauthorized transactions if reported within 60 days Paypal does not provide protections for personal transactions sending money to “friends and family.” |

Sellers protection only Square is not responsible for any unauthorized access or use of the services on your square account |

Varies by state | No protection for authorized transactions. Google Pay offers fraud protection for all verified unauthorized transactions if reported within 120 days of the transaction date |

Facebook is not liable for payments you send via Messenger Facebook provides protection for unauthorized transactions on your account if you submit a claim within 30 days |

Zelle partners with the following banks and credit unions, as of this writing:

Brittney Laryea

Brittney LaryeaBrittney Laryea is a personal finance writer for MagnifyMoney.com. She recieved her bachelor’s degree from the University of Georgia in digital and broadcast journalism and digital marketing.

Read More

Venmo

Venmo PayPal

PayPal Square Cash

Square Cash Popmoney

Popmoney Google Pay Send

Google Pay Send Facebook Messenger

Facebook Messenger