MagnifyMoney

AE Wealth Management is a registered investment advisory firm that operates through a network of advisors throughout the country that provide wealth management and financial planning services. The firm provides both personalized investment advice and model portfolios, both of which require a comparatively modest minimum of $10,000. AE Wealth Management advisors charge varying fees, and are often separately licensed to sell annuities and other insurance products.

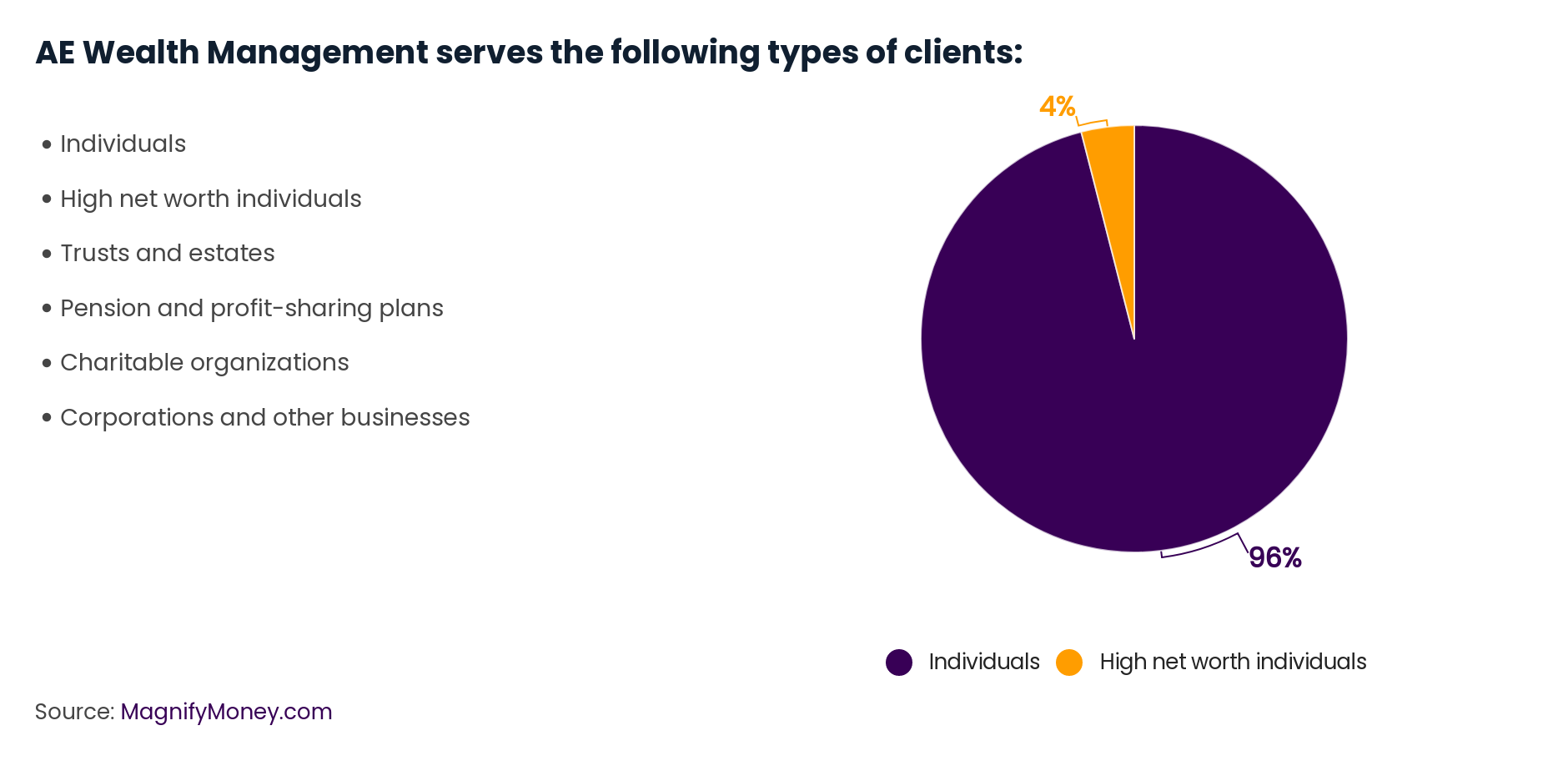

The bottom line: AE Wealth Management offers portfolio management and financial planning services and works largely with non-high net worth individuals.

| Assets under management: $12,637,103,953 | |

| Minimum investment: $10,000 | |

| Individual investor to advisor ratio: 120:1 | |

| Fee structure: A percentage of AUM, hourly charges, fixed fees | |

| Headquarters: 2950 SW McClure Rd, Suite B Topeka, Kansas 66614 Website: www.aewealthmanagement.com Phone: 866-363-9595 |

All information included in this profile is accurate as of September 8, 2021. For more information, please consult AE Wealth Management’s website.

AE Wealth Management is affiliated with an insurance marketing organization called Advisors Excel, which helps financial advisors grow their business. Two of the founders of Advisors Excel — David Callanan and Cody Foster — primarily own AE Wealth Management through affiliated trusts and a holding company.

Typically, your AE Wealth advisor is an independent contractor — not an employee — who partners with the firm for investment management services and technology. The firm currently has a team of over 500 employees, including more than 430 who perform investment advisory and research functions. Many of AE Wealth Management’s advisors focus on retirement planning, and may recommend insurance or annuities in addition to traditional portfolio instruments such as stocks, bonds and mutual funds.

The prolific personal finance author and commentator David Bach co-founded the firm, which became a registered investment advisor in 2016, along with Callanan, Foster and Derek Thompson, college friends who also founded Advisors Excel.

Bach is a bestselling financial author whose books include “The Automatic Millionaire,” “The Latte Factor” and “Smart Couples Finish Rich.” He has been a regular contributor to NBC’s “Today Show” and appeared on shows and networks including “The Oprah Winfrey Show,” “The View,” ABC, CBS, Fox, CNBC, CNN and PBS.

Today, Bach is an LLC member of the firm, which Callanan and Foster primarily own.

Non-high net worth individuals make up the bulk of AE Wealth Management’s clients. However, it also serves a number of high net worth individuals, defined by the SEC as those with at least $750,000 under an advisor’s management or a net worth of at least $1.5 million. Rounding out the firm’s current client base are various institutional investors as well as retirement plans.

AE Wealth Management generally requires clients to maintain a $10,000 minimum per account, which is a relatively low requirement in comparison to many other firms. Additionally, the firm may grant exceptions for a client’s immediate family member or if the advisor anticipates you will bring additional funds in the near future.

Financial advisors working with AE Wealth Management primarily focus on managing an individual’s investment accounts for a set annual fee. They’ll craft a portfolio specifically tailored to your situation, and execute it by buying and selling in that account, without needing to get your approval for each transaction.

Advisors generally administer clients’ investments in one of two ways: They can personally choose certain investments solely for you and serve as your portfolio manager, or they can put your money in specific model portfolios, managed either by AE Wealth Management or an outside party.

AE Wealth Management’s advisor representatives are also available to help you navigate a wide variety of financial issues through financial planning or consulting services. They can provide formal written guidance or one-time verbal consultations on topics such as investments, retirement, insurance, taxes and education.

Here is a complete list of services offered by AE Wealth Management:

As mentioned previously, AE Wealth Management can manage client funds in one of two ways:

To determine how to directly invest your money, or which model portfolio might be best for you, clients of AE Wealth Management will fill out a questionnaire addressing their financial situation, investment objectives and risk tolerance. Your investment advisor will then review that information and craft a plan tailored to your needs.

The investment team uses numerous analytical methods to determine which investments to recommend to clients. They analyze statistical and chart factors, such as price movements, volume and open interest, to try to anticipate future asset price movements, and look at which investments are sensitive to business and economic cycles. They also dig for investments they think are undervalued relative to the fundamentals of the company, such as the strength of the management team, industry conditions and other qualitative factors.

To select which model portfolios they offer clients, the team also consults the investment wisdom of an outside firm.

Asset management fees: Generally speaking, on both model portfolios and accounts managed directly by the advisor, an annual fee of up to 2.50% of your assets under management is permitted.

Clients can choose to pay that percentage annual fee bundled with transaction commissions, ticket charges and custodian fees, known as a wrap fee. There’s also the option to pay a separate management fee to AE Wealth Management and, in addition, pay separately for custody and transaction fees. Your fees are automatically deducted from your account each month.

In addition to the fees above, you could owe fees to third parties, including mutual fund and exchange-traded fund (ETF) sales loads and surrender charges, as well as variable annuity fees and surrender charges.

Financial planning and consulting fees: Beyond your investment management fee, clients may pay additional fees for financial planning and consulting, either based on an hourly rate or per project. Again the fees will vary, ranging from $0 all the way up to a maximum of $500 per hour or $10,000 per project. Before starting any work, advisors provide an estimate of the number of hours to complete the project, and will contact you to receive approval before billing more than the initial estimate if more time is required to complete the necessary work.

Bear in mind that within that financial plan, the advisor may recommend you sell securities in order to buy annuities, life or disability insurance. In that situation, always ask the advisor your specific costs for commissions, deferred sales charges as well as any other fees and expenses.

AE Wealth Management does report disciplinary disclosures. As a registered investment advisor, the firm is required by the SEC to disclose in its Form ADV any legal or disciplinary event that is material to a client’s evaluation of the advisory business or the integrity of the management personnel that occurred within the last 10 years.

Specifically, AE Wealth discloses a few events related to specific individual advisory affiliates. Additionally, the firm discloses a settlement with a private individual and a $12,600 fine related to investments in a real estate mortgage fund.

For more information on AE Wealth Management and its disciplinary history, visit its IAPD page.

AE Wealth Management has over 360 offices throughout the U.S. Specifically, it lists office locations in the following states in its Form ADV:

Additionally, AE Wealth Management is registered to serve clients in all 50 states, plus the District of Columbia and the Virgin Islands, though it does not necessarily have physical locations in all of those states.

Middle-income investors who live in an area with an AE Wealth Management-affiliated advisor may appreciate the availability of a $10,000 account minimum. Still, you would need to meet with the advisor to find out how much they charge and if any financial planning services are included, as prices vary by advisor and are negotiable.

Remember that advisor representatives wear multiple hats and often also work as insurance agents and for broker-dealers. Be aware the advisor may try to sell you annuities or life insurance products, or securities, mutual funds or other investments through a brokerage account where they earn a commission. Always ask why advisors are recommending a particular product, and what they stand to earn if you go with their recommendations.

When shopping for a financial advisor, it’s your job to untangle the web of who gets paid what for what particular services and make sure you’re comfortable with what you uncover. Be sure to research multiple firms to ensure you find the right advisor for you.

Amanda Gengler

Amanda GenglerAmanda Gengler has been researching and writing about finance for more than 15 years. She honed her personal finance writing as a journalist at Money magazine for a decade.

Read More