MagnifyMoney

CUNA Brokerage Services, Inc. is a dually registered investment advisor and broker-dealer headquartered in Waverly, Iowa. The firm generally provides its services through financial services networking agreements with different institutions across the country, the majority of which are credit unions. Currently, CUNA Brokerage Services has nearly 750 employees on staff and over $3 billion in assets under management (AUM).

The bottom line: CUNA Brokerage Services offers a range of services, including investment management and financial planning, through its network agreements with various institutions.

| Assets under management: $3,029,704,984 |

| Minimum investment: Varies by account type |

| Individual investor to advisor ratio: 20:1 |

| Fee structure: A percentage of AUM, hourly charges, other fee types |

| Headquarters: 200 Heritage Way Waverly, IA 50677 Website: www.cunamutual.com/products/investments/cuna-brokerage-services/individual-investors Phone: 319-352-4090 |

All information included in this profile is accurate as of January 24, 2022. For more information, please consult CUNA Brokerage Services’ website.

CUNA Brokerage Services is a wholly owned subsidiary of CUNA Mutual Investment Corporation, which was founded in 1935 as a credit union. CUNA Brokerage Services was established later, in 1983. It operates separately as an advisor, although many of its services are often based inside credit unions.

Of the company’s nearly 750 employees, over 580 provide investment advisory functions. In addition, more than 580 employees are licensed insurance agents and almost 750 are registered representatives of broker-dealers.

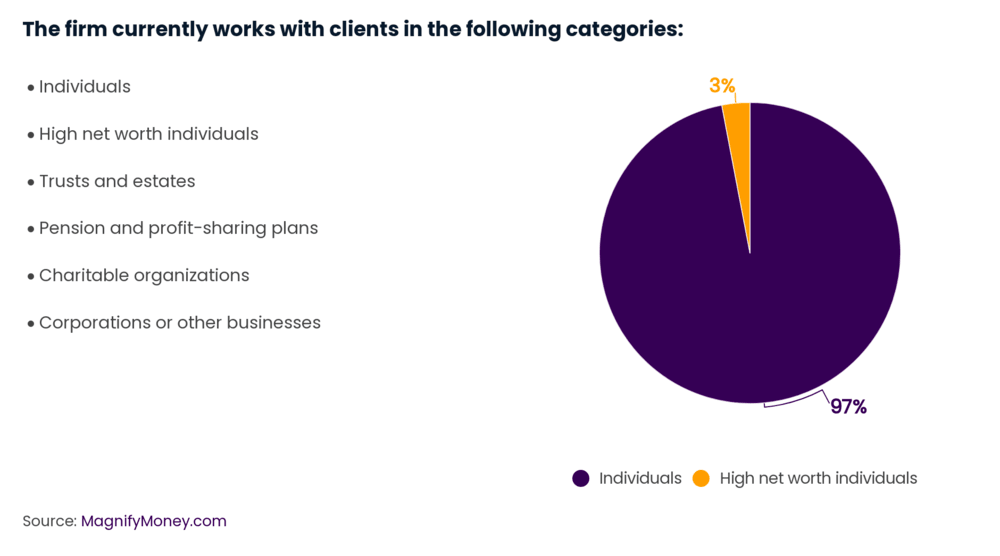

The firm primarily serves individual investors, including those who are high net worth individuals — defined by the Securities and Exchange Commission (SEC) as those with at least $750,000 under a firm’s management or a net worth of at least $1.5 million. The firm also works with businesses, charitable organizations and pension and profit-sharing plans, though it serves relatively few of these institutional clients when compared to its number of individual clients.

Minimum account balances required for managed portfolios will vary, depending on the advisor and strategy selected. Mutual fund accounts and exchange-traded funds (ETF) accounts may also have varying minimum investments.

CUNA offers client portfolio management services through its own platform, as well as through programs sponsored by other investment advisors. In addition, CUNA Brokerage Services offers financial planning and consultation services, and can also help with trust management. The firm also provides advisory services to employee benefit plan sponsors.

Here is a full list of services that clients can access through CUNA in its role as an investment advisor:

CUNA gives clients the ability to choose from different platforms and portfolio programs. The firm decides which offerings are included in its available programs and platforms.

Clients can choose from the available platforms and programs, and their investment advisor representative will then provide advice on which investments to use in the portfolio based on the client’s goals and risk tolerance. Depending on the program chosen, there might be a reliance on mutual funds and ETFs, or there might be the ability to construct a portfolio of individual equities.

It is also possible for clients to choose programs with either discretionary and non-discretionary management. With discretionary management, clients give the firm the ability to manage their portfolios and make trades without first getting their approval. On the other hand, with a non-discretionary account, the investor must approve all trades before they are made.

Investment management fees: The firm’s fees for investment management services depend on the program or platform chosen by the client. In general, the firm charges a tiered fee based on a percentage of assets under management, with rates decreasing as the amount of assets under management increases. In addition, any mutual funds or ETFs used are likely to come with expense ratios.

It’s important to note that the firm’s programs also come with additional platform and third-party fees on top of the advisory fee charged by the firm. Total maximum fees for clients, including these additional charges, can range from 1.20% to 2.20% depending on the program selected.

Financial planning fees: Clients will pay a flat fee for financial planning services, with the rate negotiated between the client and the advisor. The flat fee can be up to $7,500 annually for the initial plan and up to $8,000 per year for ongoing financial planning services. Clients who opt to implement the plan may face additional costs, such as for brokerage, transaction, custody, mutual fund management and administration and for annuity contracts.

The firm has no major disciplinary actions on its record from the last 10 years. While there might have been disciplinary actions in the past, it’s no longer required to disclose them in its filings because of the amount of time that has passed.

For reference, the SEC requires all registered investment advisors to disclose in their Form ADV whether the firm or its employees or affiliates have been subject to any disciplinary actions that would be material to a client evaluating the firm or the integrity of its management team. This includes any civil, criminal or regulatory actions that took place within the last 10 years.

CUNA Brokerage Services has 262 physical locations across the country. It lists its largest office locations in its Form ADV, which are in the following states:

CUNA Brokerage Services is registered to serve clients in all states, with the exception of Wyoming, and in the District of Columbia.

If you use other financial services at an affiliated credit union, and want everything from your banking products to face-to-face investment advice in one place, CUNA Brokerage Services may be worth considering. In addition, the firm offers a wide variety of investing programs and portfolios, which it will further customize to each client, as well as locations throughout the U.S.

However, it’s important to be aware of the fees charged by CUNA Brokerage Services. The firm’s fee structure is complex, and there are extra layers of fees that can get confusing for the average investor. In addition, advisors’ affiliations with insurance agencies and broker-dealers can create potential conflicts of interest. Before signing up, make sure you understand all of the costs involved to ensure you find an advisor who is right for you.

Miranda Marquit

Miranda MarquitMiranda Marquit has been a financial journalist for more than 12 years and has contributed to numerous national and local media outlets, including Forbes, NPR, CNBC, FOX Business, and The Wall Street Journal.

Read More