MagnifyMoney

One of the best ways to build wealth over time and meet your long-term financial goals is to create an investing plan using asset allocation — and stick with it.

At some point, though, market conditions can lead to your portfolio moving away from your planned allocation. When that happens, a portfolio rebalance is in order.

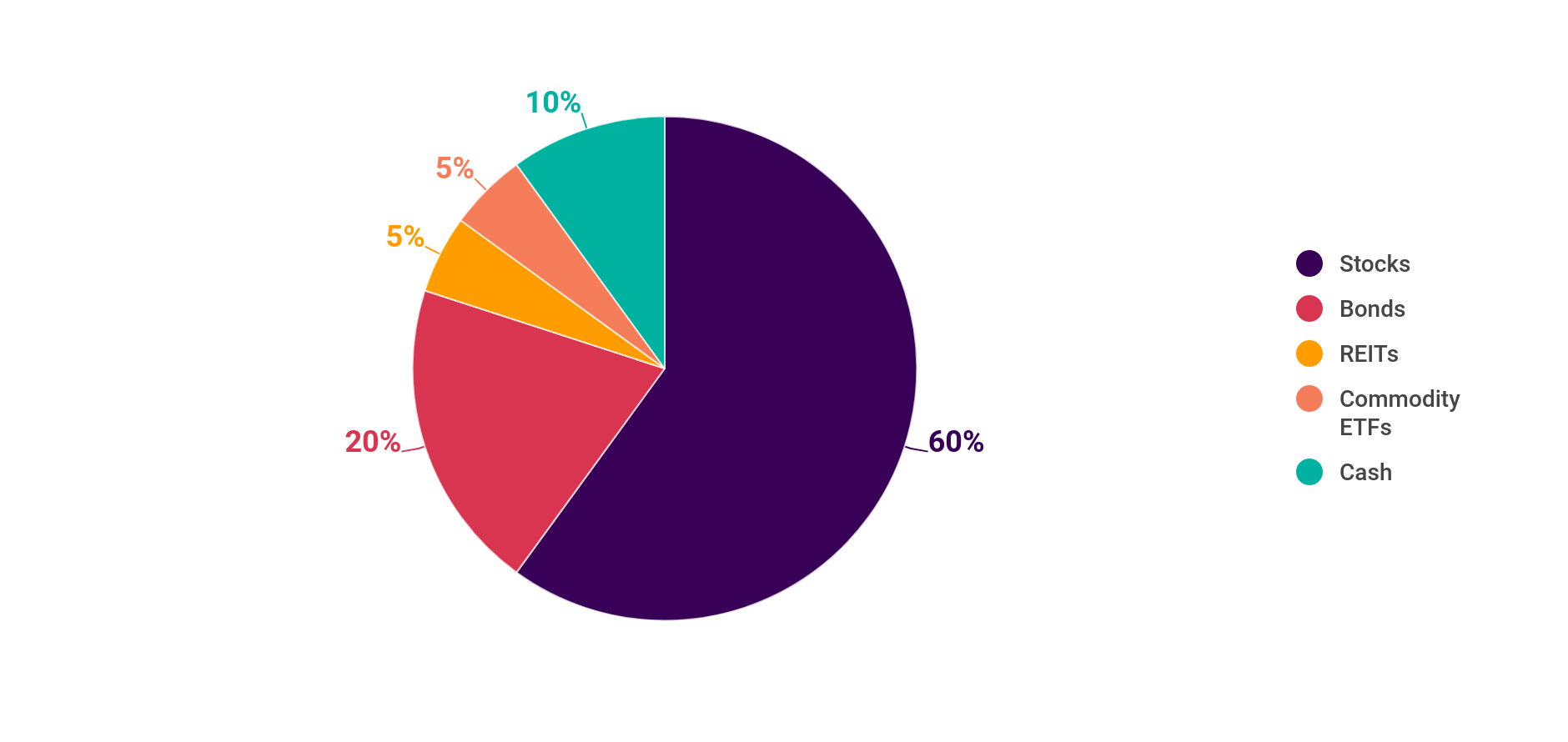

In many cases, a portfolio contains a mix of assets to help you diversify while still allowing you to reach your goals.

“When we lay out a portfolio allocation, it’s because we understand the potential risk and return, and how to align it with client goals,” said Eric Roberge, a CFP and founder of financial education website Beyond Your Hammock. “Over time, though, an asset class can go up or down, doing well or underperforming. That can cause the portfolio to go out of balance.”

For example, your portfolio might rely heavily on stocks and bonds but have some diversification with real estate, commodities, and cash.

If one asset class is doing well, it starts to take up a more significant portion of your portfolio’s value, while a worse-performing asset will take up a smaller slice of the pie. If stocks are doing well, bonds and REITs are underperforming, the idea is to sell the stocks and then buy the assets that aren’t doing as well. You take the excess profits and purchase other assets at a lower price.

“The idea is that you’re forced to do what you’re supposed to be doing anyway,” said Roberge. “You sell high and then buy something else low.”

Roberge said that it’s a good idea to maintain the asset mix you decided on since it can help you continue working toward your goals while still protecting you to some degree.

Rebalancing your portfolio isn’t something you should do all the time, said Roberge. While you want to maintain your general asset allocation, he points out that markets change regularly enough that you don’t want to respond to every move.

Here are five times to consider a portfolio rebalance.

It can be tempting to let your portfolio grow at a fast pace, especially if you see a huge outperformance somewhere. However, Roberge pointed out, when one asset’s value starts overshadowing the rest of the portfolio, there is a chance for devastation when things take a different turn.

“Your portfolio allocation was chosen to help diversify and protect your portfolio while helping you reach your goals,” according to Roberge. “If profits are high in one area, it’s a good time to take those profits and then buy something else that is undervalued.”

Eventually, the asset class will run into a rough patch, and if you’re over-invested in it, you could lose all your recent gains without portfolio rebalancing.

“Perhaps you had a goal for withdrawing some of your money for 20 years out, but you realize you need some of the money in seven years,” said Roberge. “When you tweak your goals, it makes sense to look at your portfolio and perhaps rebalance.”

Portfolio allocation involves understanding that some assets are better-suited for long-term goals and others might work better for short-term goals. For example, when you know you won’t need the money for more than 20 years, stocks make sense. However, if you need money immediately, having enough of your portfolio in cash is vital.

As your use for the money changes, you might need to change your allocation to reflect better when the money will be used.

Another reason for a portfolio rebalance is if you’re experiencing a major life event.

“A marriage or divorce can change your financial goals and money use,” said Roberge. “Additionally, if you have a child, you might tweak your portfolio to reflect an interest in saving for college.”

The main life event that often prompts portfolio rebalancing is retirement. As you approach retirement, Roberge pointed out, you start changing your allocation to reflect a need for fixed income rather than growth.

However, even in retirement, it makes sense to continue keeping a portion of your portfolio in stocks to take advantage of continued growth. “It’s important to keep your goals in mind and think of the end result — make sure your allocation is working for you.”

If you can move some of your portfolio into more tax-efficient assets, it can make sense to rebalance. For example, if you sold some outperformers earlier in the year and had large profits, you can offset some of the gains by selling some underperforming assets for a loss. The losses can offset your gains, allowing you to save money in taxes.

Roberge warned that you need to understand where various parts of your portfolio are housed. “Something in a tax-advantaged retirement account isn’t going to do much to help you with taxes because you don’t have to worry about the assets inside the account,” he said. “Know which assets, like those with already-favorable status, should be in a taxable account and which should be in a tax-advantaged account.”

Roberge said that an annual check-in with your overall portfolio makes sense. He suggested scheduling the review for the end of the year so you can use tax-loss harvesting as part of your strategy if it makes sense.

“Looking at things regularly can give you a feel for what’s happening, and help you make changes without overdoing it,” Roberge said.

There are always costs associated with investing and rebalancing. First of all, you’re likely to pay a management fee, no matter where you keep your money, so keep that in mind.

When it comes to the actual costs of a portfolio rebalance, Roberge said you’re likely to see two main expenses:

Even with the costs, though, it can be worth it to rebalance your portfolio in a way that keeps it in line with your goals and financial needs.

Rebalancing your portfolio can be a good strategy to help you maintain your portfolio and stay on track with your goals. However, said Roberge, it’s important to avoid getting too caught up in changing things. “Don’t try to do it at exactly the right time. That’s more like market timing, and it can get costly.”

Instead, he recommended rebalancing once a year, toward the end. “In early December, see if things are out of line and rebalance if needed,” he suggested. “Then, you can just set it and forget it for another year.”

Miranda Marquit

Miranda MarquitMiranda Marquit has been a financial journalist for more than 12 years and has contributed to numerous national and local media outlets, including Forbes, NPR, CNBC, FOX Business, and The Wall Street Journal.

Read More