MagnifyMoney

Stifel, Nicolaus & Company is a large broker-dealer and registered investment advisory firm that serves individuals and institutions. The firm claims a dual designation as a broker-dealer and investment advisor. This means that clients have the choice of paying a one-time fee each time they buy or sell a security, or paying a continuous fee for ongoing advice from a financial advisor. Headquartered in St. Louis, the group has over 430 additional offices across the country.

The bottom line: Stifel, Nicolaus & Company offers portfolio management and financial planning services to individuals and institutions around the country.

| Assets under management (AUM): $117,820,023,852 | |

| Minimum investment: Varies by program, ranging from $5,000 to $1 million or more | |

| Individual investor to advisor ratio: 46:1 | |

| Fee structure: A percentage of AUM, fixed fees, commissions | |

| Headquarters: 501 N. Broadway St. Louis, Missouri 63102 Website: www.stifel.com Phone: 314-342-2000 |

All information included in this profile is accurate as of September 21, 2021. For more information, please consult Stifel, Nicolaus & Company’s website.

Stifel, Nicolaus & Company traces its roots back to 1890, when its predecessor firm opened its doors primarily as a Midwestern brokerage firm that provided advice to individuals. The group first registered as a broker-dealer in 1936, and as a registered investment advisor in 1975. Stifel, Nicolaus & Company has continued to grow over many decades due to large acquisitions it has made as well as through organic growth.

Today, the firm employs more than 6,300 workers, most of whom are licensed as brokers. Indeed, the company’s main source of revenue comes from its brokerage operations. That said, about half of its workforce performs investment advisory roles including research. Many advisors also sell insurance.

The firm is owned by the publicly traded company Stifel Financial Corp. It operates many other brands across the financial industry including in wealth management, investment banking, securities brokerage and lending and trust services, among others.

Stifel, Nicolaus & Company dates back to 1890, when Benjamin Altheimer and Edward Rawlings first began giving financial advice to individuals. Seven years later, Herman Stifel joined as treasurer. The company credits Stifel for growing the firm over the next 40 years. Henry Nicolaus and his son joined the company in 1910, and the firm was rebranded as Stifel, Nicolaus Investment Company in 1923.

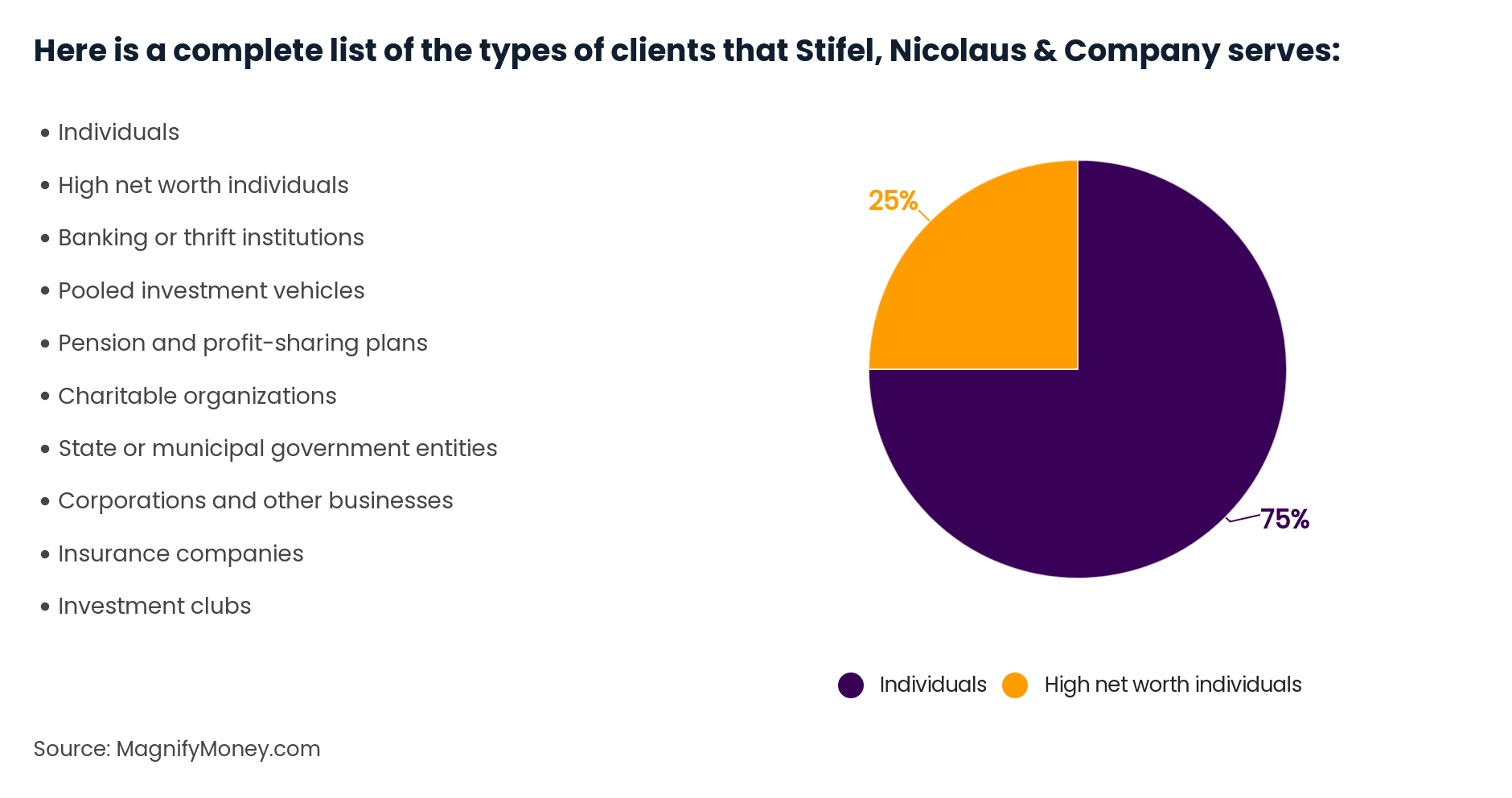

Stifel, Nicolaus & Company boasts a wide variety of individuals and institutions on its client list. The bulk of the firm’s assets under management come from individuals, both who are and are not high net worth clients. (For reference, the SEC defines high net worth individuals as those with at least $750,000 of assets to invest or a total net worth of $1.5 million.) Rounding out the firm’s client list are a few thousand institutions, including employee benefits plans, educational institutions and insurance companies, among others.

The minimum amount clients need to invest varies by program, ranging from $5,000 to $1 million or more. There is no minimum account size requirement for financial planning.

Stifel, Nicolaus & Company offers portfolio management and financial planning to individuals. For portfolio management services, clients can decide how involved they want to be. The firm offers discretionary relationships, where advisors have the power to make the daily trading decisions in the account, as well as non-discretionary management, where clients must approve each trade before it is executed. The firm even offers a program for its financial advisors to weigh in on assets held elsewhere.

Financial planning clients receive a written plan that can address a mix of financial issues. Possible topics include a client’s overall net worth, their retirement outlook, insurance needs, estate planning and the appropriate asset allocation. Financial plans do not include specific investment recommendations. Once an advisor has supplied the plan, it is up to the clients to decide if they’d like to implement the recommendations and, if so, as a brokerage or financial advisory client.

Given the firm’s dual designation as a broker-dealer and registered investment advisor, clients can work with the firm either through a brokerage account, an advisory account or both if they choose.

Here is a complete list of services offered by Stifel, Nicolaus & Company:

The firm offers numerous account programs and strategies, depending on your needs and how much you want to be involved in investment decisions. For clients looking for discretionary management of their accounts, they have the option of enlisting their financial advisor, an affiliated advisor or a third party as their portfolio manager. Or, they can hold on to that authority by opting for a non-discretionary account, where they have the final say on trading decisions. Clients also have the choice to bundle in transaction costs along with advisory fees, known as wrap accounts, or pay separately for advisory and trading costs.

The primary investments used in the firm’s programs are equities, exchange-traded funds (ETFs), mutual funds, options and fixed income securities. Other investment recommendations may include certificates of deposit (CDs), unit investment trusts, real estate investment trusts (REITs), publicly traded master limited partnerships and private investment vehicles (e.g. hedge funds and private equity funds).

The firm has specific groups that select the recommended investment products in the various investment categories, such as mutual funds or alternatives. To come up with their investment recommendations, the team does not stick to one type of research but relies on a mix of methods including fundamental, quantitative and technical analysis.

The table below outlines the various investment programs offered by Stifel, Nicolaus & Company:

| Stifel, Nicolaus & Company Investment Programs | |

|---|---|

| Program name | Investment strategy |

| Wrap fee accounts | |

| Fundamentals Program | Advisors help clients choose from model portfolios of mutual funds, ETFs and equities |

| Horizon Program | Provides non-discretionary management services like recommending and advising on specific investments |

| Custom Advisory Portfolio Program | Management of various investments, including ETFs, mutual funds and various portfolios, within a single account |

| Opportunity Program | Designed for high net worth investors who want comprehensive, discretionary investment management, offered by independent or affiliated groups |

| Solutions | Individualized investment management offered through a client’s Stifel advisor on a discretionary basis |

| Connect Program | Stifel advisor connects clients to another advisor for account management, with whom a separate agreements is signed |

| Non-wrap fee accounts | |

| Summit Program | Stifel advisor consults on assets held elsewhere; intended for high net worth individuals or institutions |

| Vantage Program | Offered only by certain Stifel advisors, this program manages client money on a discretionary basis according to an appropriate strategy; clients pay through broker commissions |

Investment management fees: For ongoing investment management, most clients of Stifel, Nicolaus & Company will pay an advisory fee that is calculated as a percentage of assets under management. In some cases, the firm may agree to a fixed fee instead. The advisory fee is typically negotiable, with the rate determined based on factors including the amount you have invested, the nature and level of advice you want to receive and the investment products you prefer. The firm does have set limits on how much its advisors can charge. Maximum fees range from 1% for non-wrap accounts to 2.50% for wrap accounts.

On top of the advisory fees, clients may face additional product and other fees, such as third-party management fees, custodial fees and transaction fees for non-wrap accounts, among other costs.

Financial planning fees: The financial planning fee charged by Stifel, Nicolaus & Company is also negotiable but typically has a maximum limit of $5,000, with the exact rate dependent on the complexity of a client’s situation, the amount of assets being considered and the scope and range of services provided . That said, the firm notes that most financial planners provide this service at no charge to clients.

Stifel, Nicolaus & Company discloses a number of disciplinary actions over the prior decade, which is not necessarily out of the ordinary for large firms employing thousands of workers. For reference, the Securities and Exchange Commission (SEC) requires all registered investment advisory firms to disclose to the public on their Form ADV any criminal, civil or regulatory actions against the firms or its employees or affiliates that a potential client would deem material when evaluating the firm and the integrity of their leaders.

Some of the disciplinary disclosures against Stifel, Nicolaus & Company over the last 10 years include:

Additionally, the firm discloses many actions against specific individuals or advisory affiliates, so be sure to check your potential advisor’s disciplinary history on FINRA’s Brokercheck or the SEC’s Action Lookup tool.

For more information about Stifel, Nicolaus & Company’s disciplinary disclosures, visit its IAPD page to read its Form ADV and ensuing disclosures.

Stifel, Nicolaus & Company has a large national network across the United States, with over 430 offices in total. On the firm’s formal ADV disclosure, the firm lists some of the states it houses advisory offices. The list of those states is below. That said, the firm has many more offices in other states not listed here.

To find out if there is an office near you, check out the firm’s branch directory for a complete list of states where the firm has a wealth management office.

Clients looking for a local advisor who will accept accounts smaller than six figures can consider Stifel, Nicolaus & Company as a potential fit. Many advisors will even include basic financial planning information for no additional cost, which is not always the case for financial advisory firms.

Advisors do potentially face conflicts of interest, however, since they receive compensation for selling certain investment products. Also, fees are unclear since there is no set schedule, and may run high if advisors charge close to the maximums the firm allows for wrap fee programs. Thus, if clients aren’t comfortable negotiating their fees, or would prefer that their advisors aren’t paid by investment firms to recommend products, they may want to consider other firms.

The bottom line is that how financial advisors are paid varies across the industry. It’s the client’s job to understand how any potential advisor is paid, and make sure they are comfortable with the arrangement. Before choosing an advisor, take the time to research a few options to ensure you find the right advisor for you.

Amanda Gengler

Amanda GenglerAmanda Gengler has been researching and writing about finance for more than 15 years. She honed her personal finance writing as a journalist at Money magazine for a decade.

Read More