MagnifyMoney

Unexpected personal expenses can disrupt your budget, and too much credit card spending can push your debt balance into the red — at times like these, you might want to stop contributing to your 401(k). Although saving for retirement should always be one of your core financial goals, there are times when you may need to stop contributing to your 401(k) retirement plan. Read on, and we’ll review them all.

One of the biggest benefits offered by the 401(k) is matching contributions. With matching contributions, your employer matches the money you deposit in your 401(k) dollar-for-dollar, up to a certain threshold. This helps turbocharge your retirement savings at no extra cost to you.

However, not all employers offer matching contributions. You can still contribute to your 401(k) even if your employer doesn’t offer a match, but a lack of matching contributions might make you consider other retirement savings options, such as an individual retirement account (IRA), depending on your savings goals.

If your employer doesn’t offer matching contributions, a good way to gauge whether the 401(k) plan is a good choice for your retirement savings is to look at the fees. If the fees charged by your employer’s 401(k) plan are higher than you like, consider other retirement savings options.

Fees charged by 401(k) plans fall into three broad categories: investment fees, 12b-1 fees and administrative fees.

Total fees charged on your 401(k) can range from 10 basis points to 2% to 3%. You pay the plan administrator these fees out of your investment balance, and while a few percentage points a year may not sound like much, these fees add up over the life of your 401(k).

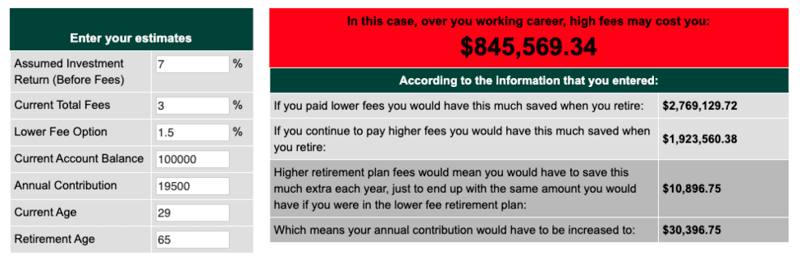

Imagine a 29-year-old investor who contributes $19,500 per year to her company’s 401(k) and plans to retire at age 65. Her current 401(k) balance is $100,000, and fees are 3%. Just by switching to a plan that cuts fees in half, to 1.5%, she could save $845,569 by the time she retires. Instead of having $1.9 million upon retirement, she could have more than $2.7 million.

Check out the fee calculator we used to find out just how much your fees are costing you

Remember, even if your 401(k) has high fees, an employer match is still worth considering. Many times, the match will more than cover the fees.

While it’s always possible to both pay down debt and make 401(k) contributions, large debt loads charging high interest rates may require more budgetary attention. Very high APRs from your credit card issuers or a debt-to-income ratio that’s too high may mean you should prioritize paying off debt ahead of saving for retirement.

The key thing to consider is how much you’re paying in interest on your debt compared to the returns you’re getting on your investments. If you’re paying an APR of 15% to 20% to a credit card company but you’re only seeing an annual return of 5% to 8% on your 401(k) investments, you may be losing money. That said, pausing contributions to accelerate your debt payoff means you’ll need to play catch-up on your retirement savings later.

Sometimes life gets in the way of your financial goals, especially when emergency spending disrupts your budget. We always advise our readers to build a healthy emergency fund to be prepared for large, unexpected costs or major medical emergencies, but if your fund is low or non-existent, it might be time to hit pause on your 401(k) contributions.

Think hard about expenses that are high enough to make you consider pausing your 401(k) contributions. Can you meet them by cutting out other spending, or refining your budget? Our rule of thumb for when to dip into your emergency fund holds good here as well: Ask yourself whether the expenses are unplanned and uncontrollable. Only true emergencies that are both unplanned and uncontrollable should require you to stop contributing to your 401(k).

The ultimate end point to your 401(k) contributions is when you stop working. Remember, 401(k) plans are sponsored by your employer, so when you retire and stop working, your days of making contributions to your 401(k) plan are over. However, this may not be the end of your retirement savings journey.

Halting 401(k) contributions might be financially necessary, but you should keep in mind what you’re giving up in exchange.

If you stop contributing to your 401(k), that doesn’t mean you should stop saving altogether. Keep saving in these other accounts if you have the money to spare: