MagnifyMoney

There’s been a lot of turbulence in the stock market over the past few years: the shock from the onset of the COVID-19 crisis in early 2020, a massive rally through 2021 and a downturn in 2022. During periods of growth, people may regret not having invested their money, but investors who try to time the market can experience losses.

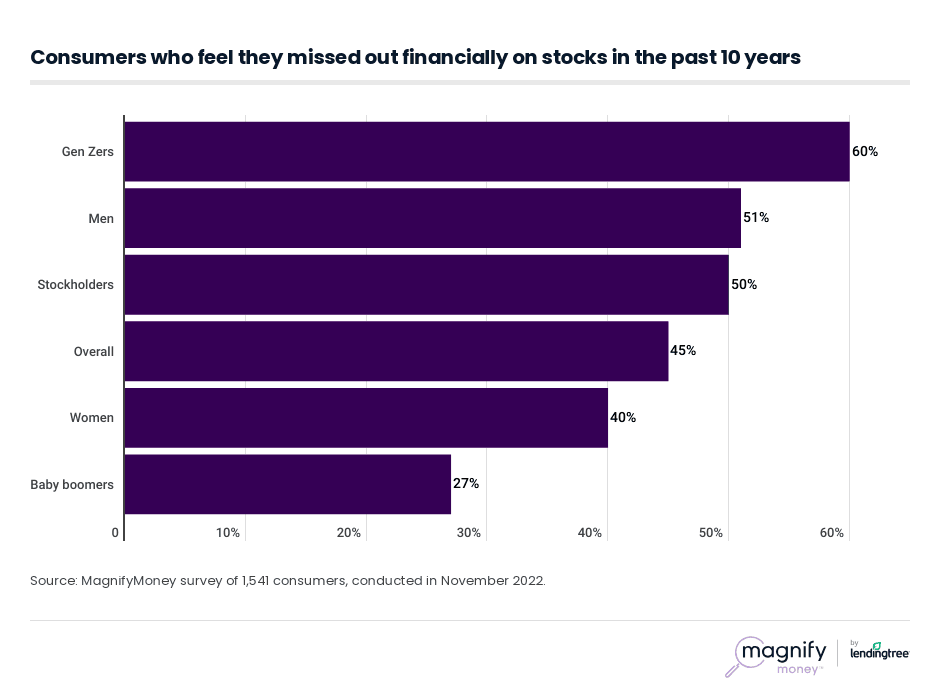

According to the newest MagnifyMoney survey, 45.1% of Americans feel they’ve missed out on financial opportunities by not investing more or at all over the past decade. Stock investments have historically grown over long time horizons.

But, as we’ve seen in 2022, trying to time your investments might backfire. “Timing the market is very risky,” according to MagnifyMoney Executive Editor Ismat Mangla. “Research shows that timing the market perfectly is virtually impossible.”

Our findings show a significant generational split among those who wish they’d invested more or at all in the past 10 years, with younger people saying they had more regrets:

That trend was even more pronounced among people who’ve never owned stock. More than half (57%) of the Gen Z respondents who haven’t owned stock say they feel they’ve missed out, but just a small fraction (16%) of baby boomers feel the same. Perhaps older respondents feel more secure in their financial situation, even if they haven’t invested in stocks.

Many wealthier respondents own stock (85% of those with an annual household income of $100,000 or more), but more than half of them regret not investing more. Those with the highest educational attainment levels are also very likely to own stock, but they tend to have fewer regrets.

By contrast, half of people with an annual household income below $35,000 have never owned stock, and almost two-thirds of those respondents don’t regret not investing at all. The most common reasons people haven’t owned stock or changed investment strategies are because they didn’t have enough money (58%) or didn’t understand the market or how to invest in it (40%).

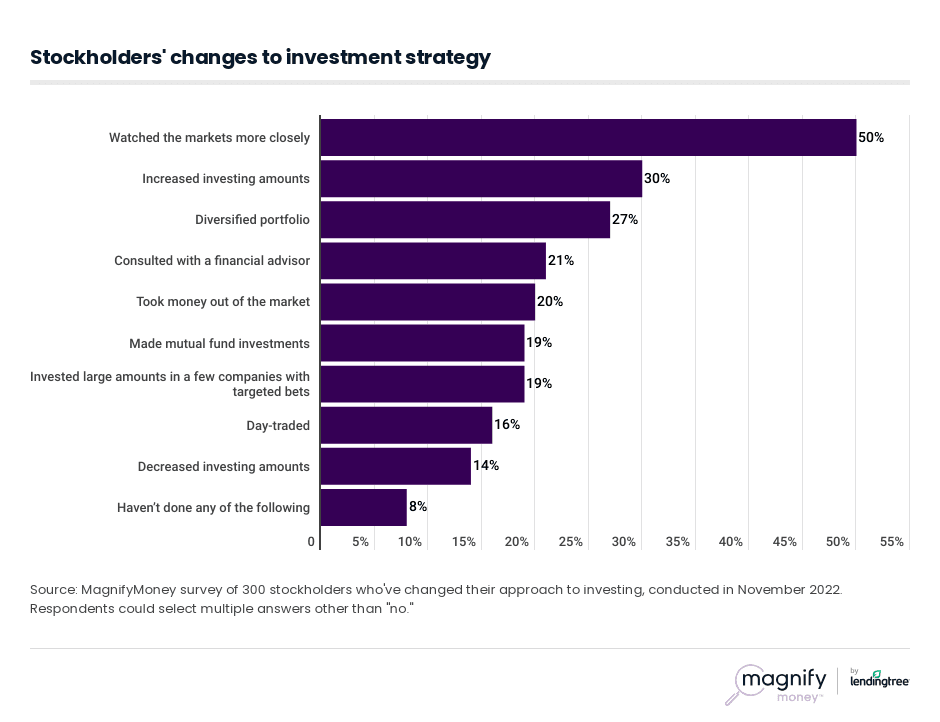

Among those who feel they missed out on financial opportunities in the stock market, slightly more than half of respondents (51%) say they changed their approach to investing (including 61% of men and 40% of women). Some started investing in the market (21%), while others tweaked their investments to a more conservative (18%) or aggressive (13%) approach.

For stockholders who updated their approaches, those strategy changes often included following the market more closely, as well as other investing tactics:

Men tended to have more aggressive investment changes than women, as 34% of men increased their investment amounts, compared to 15% of women (men and women decreased investment amounts at 15% and 14%, respectively). A higher rate of men started day trading or made large, targeted stock investments, but a higher percentage of women consulted with a financial advisor.

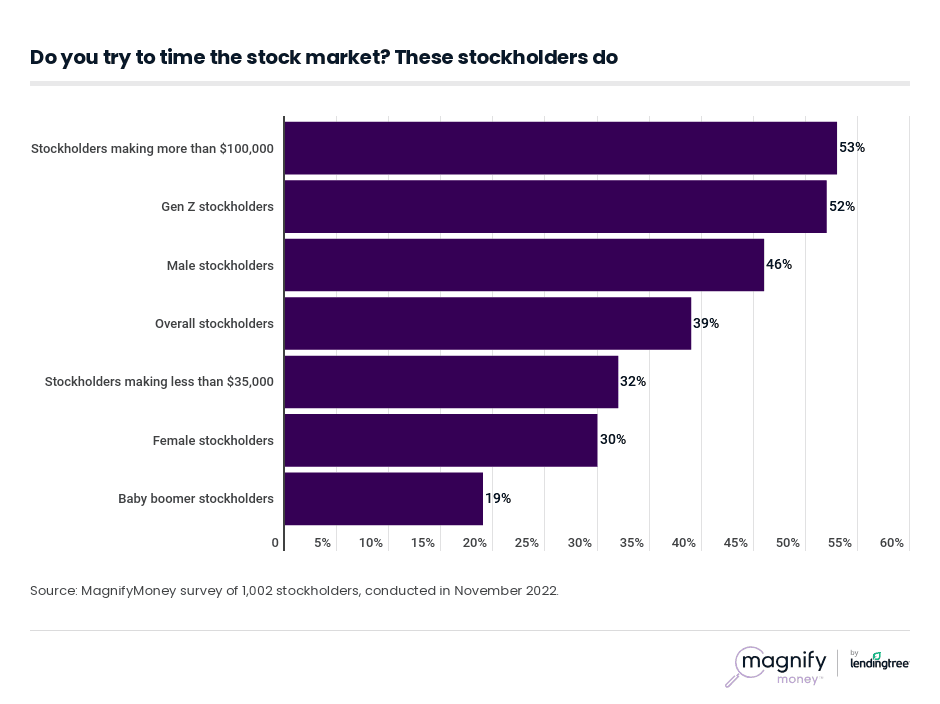

Trying to time your stock investments perfectly is tempting — everyone wants to buy low and sell high. But our survey finds that less than half of stockholders (39%) try to time their investments. A lot of investors prefer a buy and hold investment strategy for the long haul rather than trading stocks.

Some investor demographics do try to time the market, including wealthier and younger investors:

Not only does timing market investments carry risk, but Mangla notes that it costs investors over time. Instead of timing the market, she suggests focusing on time in the market. “You want to stay invested during turbulent times so that you can recover any losses in the long run,” she says.

Investors with a long time horizon, including workers saving for retirement in tax-advantaged accounts, tend to be able to weather the storm.

MagnifyMoney researchers gathered S&P data to see how stock investments made the day before certain large crashes would have fared over time. This is based on a hypothetical investment in the S&P. (Because the S&P is an index, interested investors would need to put money in an index fund or exchange-traded fund — ETF — to replicate the companies within).

Our data finds that most investments hadn’t recovered after a year. Here’s how $1,000 invested in the S&P 500 (except for during the Wall Street crash of 1929, when the index featured 90 stocks) the day before the crash would have fared a year later:

Among the five crashes we examined, there was one where you’d have more money a year later: the COVID-19 crisis crash in early 2020. Those who invested $1,000 the day before the market crash in February 2020 would have gained 14%, putting their investment at $1,145, had they not pulled their money.

For investors who could afford to keep their money in the market, the impact of those losses grew smaller over time. But traders looking to turn around and profit from most of those investments lost money — some more significantly than others. Especially for those who trade on margin — by using money loaned from brokerages to place bets on market movements — those losses were devastating.

Eventually, the market recovered. In some cases, the market posted huge gains in the decade following the crash, but there were some prolonged downturns (most notably during the Great Depression). Here’s how those $1,000 investments in the S&P right before crashes performed 10 years later:

Here’s a complete look after one, five and 10 years (when available):

| Value | % change | Gain/loss | ||||

|---|---|---|---|---|---|---|

| Wall Street crash of 1929 | ||||||

| 1 year | $685 | -31% | -$315 | |||

| 5 years | $339 | -66% | -$661 | |||

| 10 years | $504 | -50% | -$496 | |||

| Black Monday 1987 | ||||||

| 1 year | $978 | -2% | -$22 | |||

| 5 years | $1,456 | 46% | $456 | |||

| 10 years | $3,379 | 238% | $2,379 | |||

| Dot-com bubble 2000 | ||||||

| 1 year | $880 | -12% | -$120 | |||

| 5 years | $861 | -14% | -$139 | |||

| 10 years | $814 | -19% | -$186 | |||

| Financial crisis of 2007–2009 | ||||||

| 1 year | $861 | -14% | -$139 | |||

| 5 years | $1,400 | 40% | $400 | |||

| 10 years | $2,395 | 140% | $1,395 | |||

| Coronavirus pandemic 2020 | ||||||

| 1 year | $1,145 | 14% | $145 | |||

| Nov. 1, 2022 | $1,139 | 14% | $139 | |||

Source: MagnifyMoney analysis of Stooq data, cross-checked with Nasdaq and Yahoo.

Mangla says that while market downturns are inevitable, recoveries are pretty swift in most cases.

“Of course, there are certain periods when a very steep recession ends up requiring a very long recovery period,” she says. “But generally, the research shows that staying invested over the long haul is the best way to recover losses.” Market investments tend to gain value over time — on average, according to McKinsey & Company, the stock market has grown an inflation-adjusted 6.5% to 7.0% since about 1800.

As investors get closer to retirement, they should transition to a more conservative investment strategy to minimize downside risk, as the market can fall significantly during a given year. While the market does tend to recover after downturns, it can take a while. Investors should know that all stock investments carry risk, even as part of a diversified, well-balanced portfolio.

MagnifyMoney researchers analyzed the S&P stock market index from 1929 through October 2022. Researchers calculated what investing $1,000 the business day before the largest market stock crashes would return in one, five and 10 years.

Researchers examined the following stock market crashes:

Calculations for each market crash are based on investing that $1,000 in the hypothetical S&P index. The S&P index was first founded in 1923. In 1926, it was indexed based on 90 stocks. The S&P 500 was introduced in 1957. Data for this study is from Stooq and was cross-checked with Nasdaq and Yahoo.

Separately, MagnifyMoney commissioned Qualtrics to conduct an online survey of 1,541 U.S. consumers ages 18 to 76 from Nov. 15 to 21, 2022. The survey was administered using a nonprobability-based sample, and quotas were used to ensure the sample base represented the overall population. All responses were reviewed by researchers for quality control.

We defined generations as the following ages in 2022:

Alex Cook

Alex Cook