MagnifyMoney

As inflation continues to rise, Americans are feeling the effects at the grocery store, gas pump and elsewhere. But inflation isn’t only impacting short-term spending. In fact, most consumers say they’re putting off major financial milestones like buying a house, beginning a family or working toward retirement.

LendingTree chief credit analyst Matt Schulz says inflation’s impact has been seismic.

“The financial margin for error has shrunk to near-zero,” he says. “When that happens, it forces people to change plans and make tough decisions. People are delaying having children because they don’t think they can afford it. They’re putting off buying a house because they can’t save for a down payment. They’re putting off retirement because inflation has wrecked all of their calculations for how much money they’d need to have to get by in their golden years. It’s a difficult time for many Americans. Unfortunately, it seems like it’s going to get worse before it gets better.”

MagnifyMoney asked more than 1,500 U.S. consumers about their financial confidence and security. In addition to going over who feels most prepared for the next stage of life, we’ll discuss how investment strategies have changed in the past two years.

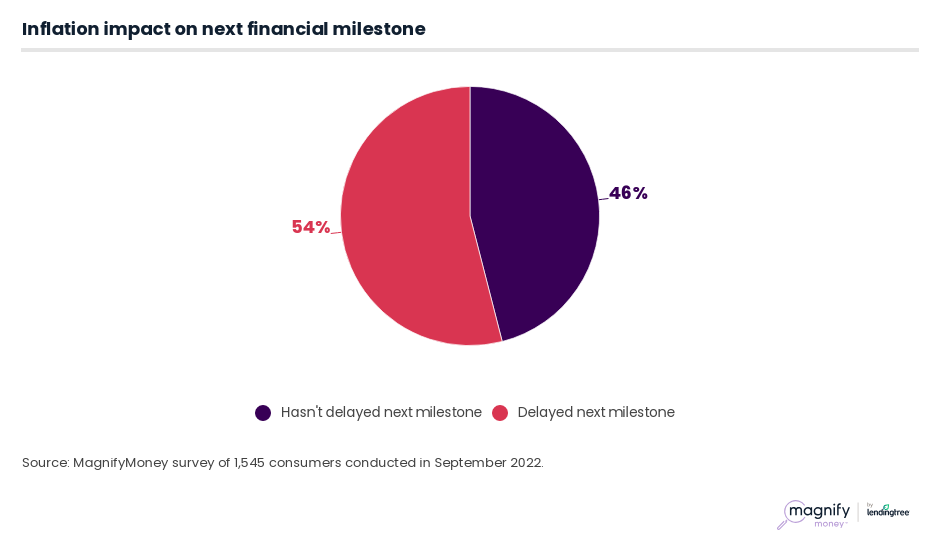

As the U.S. grapples with the possibility of a recession, the American dream grows further out of reach for many. In total, 54% of consumers say inflation has delayed their next financial milestone.

Millennials, the generation that saw some members begin their careers after the dot-com bubble burst and during the Great Recession of 2007 to 2009, can’t seem to catch a break. More than 6 in 10 (63%) millennials ages 26 to 41 put off their next major financial milestone — the highest among any age group.

Schulz says millennials are most impacted because they’re in one of the most expensive periods of life.

“Millennials are facing one significant milestone after another,” he says. “They’re starting families, buying houses, starting businesses, contributing to kids’ college funds and more — or at least they would be if they could afford to do so. The problem is that millennials have taken gut punch after gut punch since joining the workforce, which has made it really hard for them to get ahead.”

Meanwhile, just 32% of baby boomers ages 57 to 76 say inflation has delayed their next financial milestone, making them the least likely age group to say so. Not all older consumers are doing so well, though. Among Gen Xers ages 42 to 56, meanwhile, 60% are putting off their next milestone due to inflation. Gen Zers ages 18 to 25 aren’t far behind at 58%.

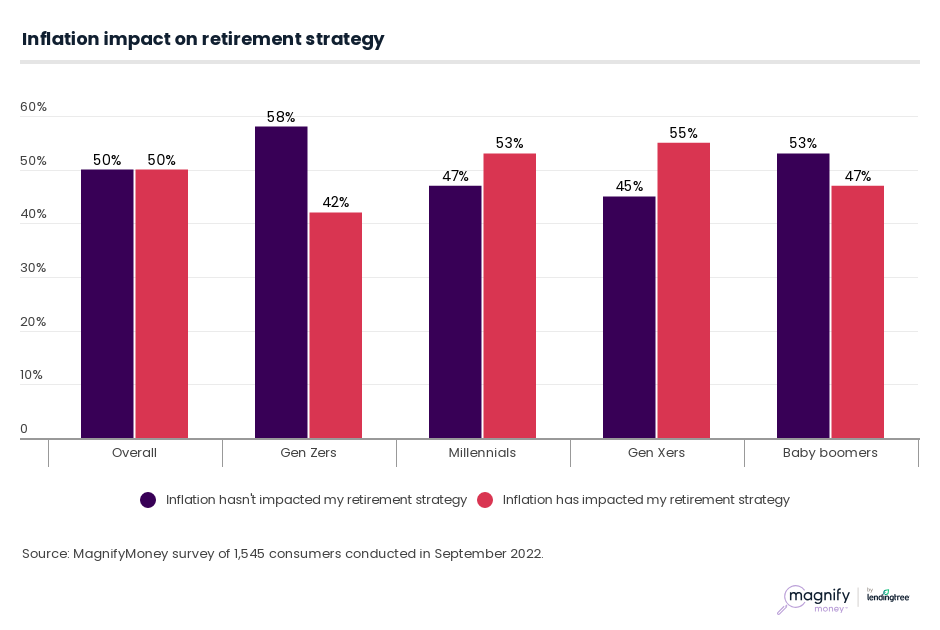

Inflation hasn’t just affected the next financial milestone, but the final one (for many) as well. Exactly half (50%) of Americans report inflation has impacted their retirement strategy. Unsurprisingly, that figure is highest for Gen Xers, some of whom may be nearing retirement. Of this group, 55% say they’ve had to adjust their retirement strategy due to inflation.

Millennials are the second most likely generation to adjust their retirement strategies due to inflation at 53%. That’s followed by 47% of baby boomers and 42% of Gen Zers.

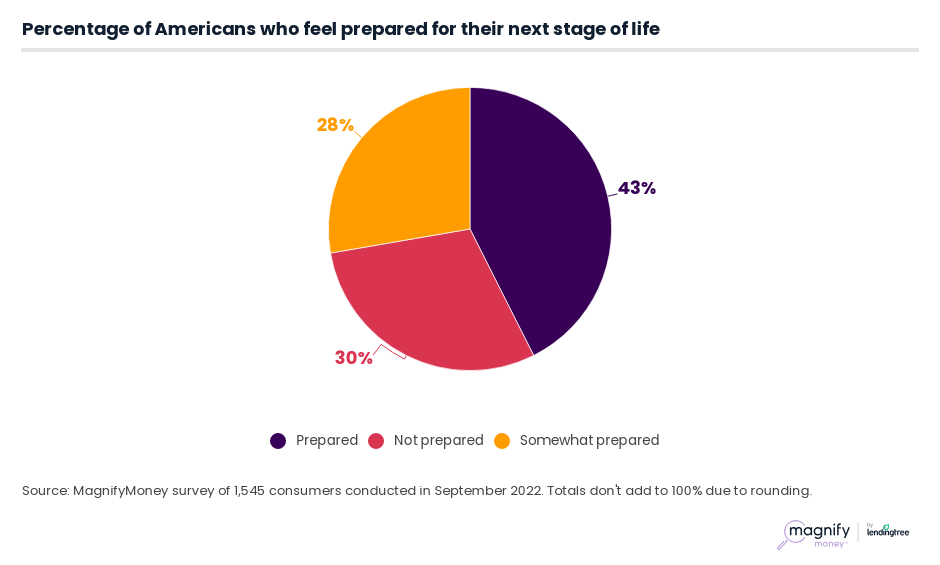

Regardless of their next financial milestone, few Americans feel fully prepared for it. When asked how prepared they feel for the next stage of life, only 43% of Americans say they feel fully prepared. Another 28% say they’re somewhat prepared.

There are some significant disparities among demographics. Men (51%) are far more likely to report they feel fully prepared for their next stage of life than women (35%). Additionally, those with good to exceptional FICO credit scores are far more likely to feel prepared than those with poor to fair scores. By score, here’s a breakdown of the groups most likely to feel fully prepared for the next stage of life:

Additionally, a quarter (25%) of consumers who don’t know their credit scores say they feel fully prepared.

Given the economy’s tumultuous nature, it’s not surprising that most Americans aren’t feeling quite prepared for their next financial milestone. But it’s not just that they’re feeling unprepared. In fact, some are feeling less prepared than before the pandemic began.

Overall, more than one-fifth (21%) of Americans say they no longer feel as prepared for their next stage of life as they did two years ago. An additional 27% say they didn’t feel prepared then and don’t feel prepared now. But not all Americans are feeling unsure. In fact, 37% say they felt prepared then and feel prepared now, though people with exceptional credit scores (67%), six-figure earners (57%) and baby boomers (53%) are the most likely to say so.

Consumers don’t only lack financial confidence, but their recent decisions reveal that many may also lack critical financial security — and it’s likely impacting their ability to reach that final financial milestone.

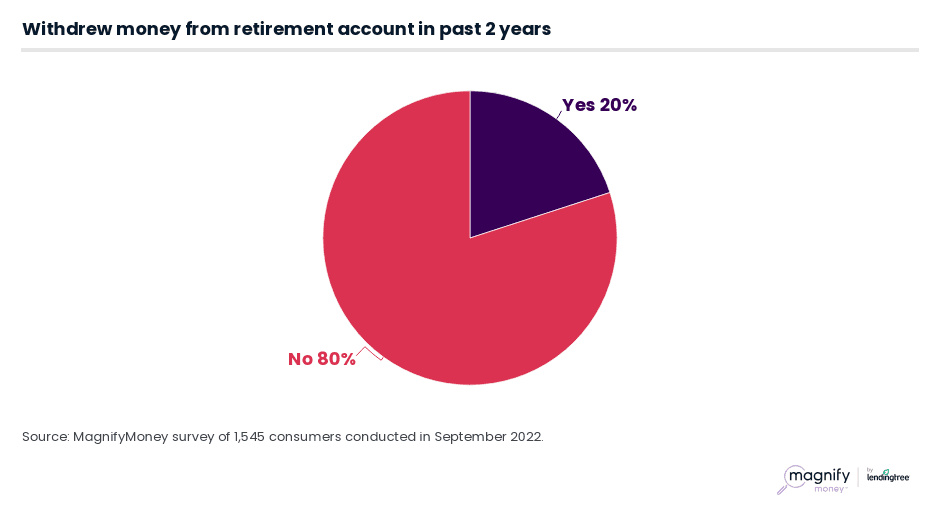

In total, 20% of consumers have had to take money out of their retirement accounts over the past two years. High earners are more likely to pull from retirement than low earners, though that may be because high earners are more likely to have retirement accounts. Among those with annual household incomes between $75,000 and $99,999, 31% have pulled from their retirement accounts. That’s followed by 30% of six-figure earners.

Generally, consumers are pulling from retirement to deal with unexpected expenses. Of those who’ve withdrawn money from their retirement accounts, 21% say it was to pay for emergency expenses — the most common reason. That’s followed by medical expenses (12%).

Meanwhile, rising costs have also eaten into consumers’ retirement accounts, as 11% say they withdrew from retirement to afford regular household expenses like groceries or utilities. That ties with home repairs as the third most common reason to pull from retirement.

While Schulz says pulling from retirement is sometimes necessary, there are hefty costs.

“The biggest problem is the opportunity cost,” Schulz says. “That $1,000 you take out today is $1,000 that won’t be invested or saved going forward, meaning that it won’t have the chance to grow into more money in the future, and that’s a really big deal. There’s no more powerful asset for investors than time, and when you pull money out of retirement accounts, you squander that advantage. Yes, sometimes it may be the best of a bunch of bad choices, but it’s still something to avoid if possible.”

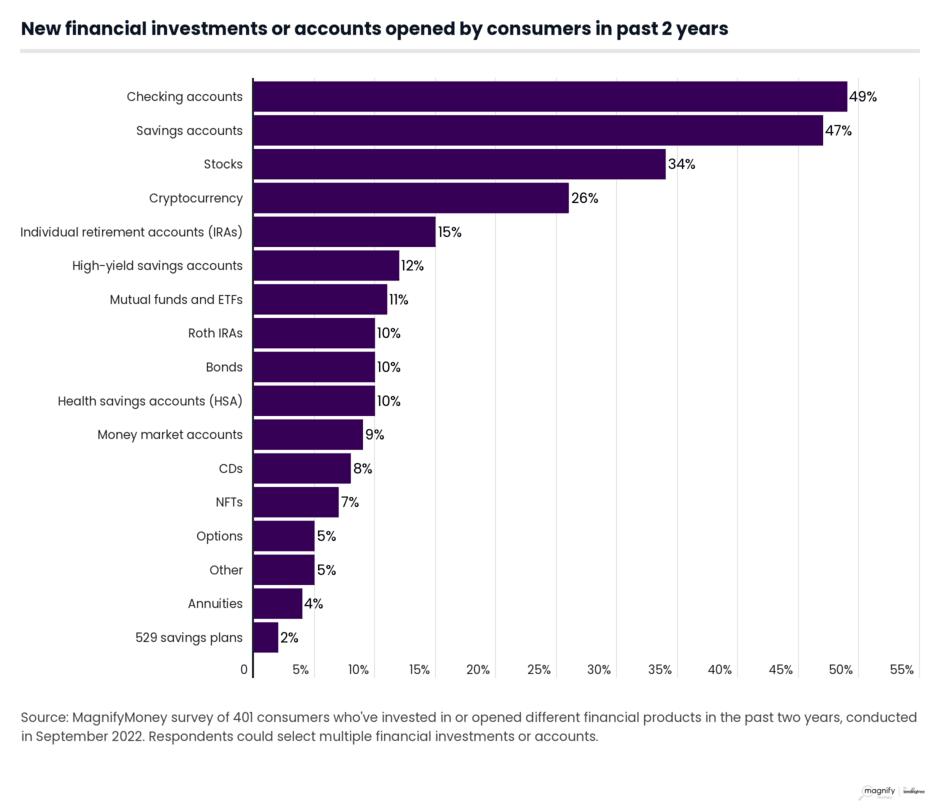

Consumers’ investment strategies are shifting due to the uncertainty many Americans have felt in the past two years. In fact, over a quarter (26%) of Americans report investing in or opening different financial products in the past two years, with most choosing some of the safest options out there.

Of all financial products, consumers are most commonly opening checking accounts (49%) and savings accounts (47%). However, some haven’t been swayed from making more risky decisions. In fact, 26% say they invested in cryptocurrency over the past two years, making it the fourth most common financial product.

With the stock market consistently in the red of late, Americans are more likely to invest in stocks now than before 2020, as many may expect high returns when the market rebounds. Over the past two years, 34% invested in the stock market, compared with the 19% who invested before 2020. Meanwhile, the percentage of consumers investing in bonds and mutual funds and exchange-traded funds (ETFs) are also up by a few percentage points.

Amid increased interest in investing, though, most haven’t begun seeking advice from an advisor over the past two years. In fact, just 16% have added a financial advisor over that period. Six-figure earners are the most likely to have done so at 37%. That compares with 6% of Americans who earn less than $35,000. By age group, millennials (22%) are the most likely to have sought a financial advisor, while baby boomers (11%) are the least likely.

However, not all consumers are forgoing financial advisors — some have likely been relying on a financial advisor since before the pandemic began. A recent MagnifyMoney survey found about 4 in 10 (41%) Americans have a financial advisor.

While the market may look bleak, high APYs and low stock prices can benefit consumers — even if they may have to delay a few financial milestones.

“As nerve-wracking as it might be, younger consumers can just hold tight with their investments, trusting that the market will move higher over time,” Schulz says. “Older consumers may not have that luxury, so they’d be wise to speak with a financial professional (such as a financial advisor) about their options.”

No matter your age, however, Schulz recommends the following options for building wealth:

MagnifyMoney commissioned Qualtrics to conduct an online survey of 1,545 U.S. consumers ages 18 to 76 from Sept. 20 to 23, 2022. The survey was administered using a nonprobability-based sample, and quotas were used to ensure the sample base represented the overall population. All responses were reviewed by researchers for quality control.

We defined generations as the following ages in 2022:

Maggie Davis

Maggie DavisMaggie Davis is a staff writer for studies and surveys at MagnifyMoney. A journalism graduate from Pepperdine University in Malibu, Calif., she has previously held public relations and journalism roles.

Read More