MagnifyMoney

You can compare apples and oranges all you want (nutrition, convenience, taste, etc.), but how people feel at snack time determines which they eat, if either. The same goes for financial advisors and tech-based tools that provide automated, algorithm-driven financial planning services — aka robo-advisors. Plenty of sites compare financial advisors and robo-advisors on everything from cost to complexity, but it’s how people feel about entrusting their hard-earned dollars to one or the other (or neither) that we wanted to explore further.

The latest MagnifyMoney study of nearly 1,600 Americans finds that 63% of consumers are open to using a robo-advisor to manage their investments, with millennials being the most open (75%). That said, only 41% of Americans with investments use a financial advisor — and just 1% say they use a robo-advisor. Here, we look at why that may be and other beliefs about financial advisors and robo-advisors.

Americans are generally warm to robo-advisors, with only 36% saying they’re not open to using one to manage their investments. The rest haven’t ruled them out. Some are lukewarm, with 38% saying they may be open to using a robo-advisor, while 26% answered yes. Just 1% of respondents currently use a robo-advisor.

Of course, some generations are more open to robo-advisors than others. As we mentioned, millennials ages 26 to 41 are the most likely to embrace the idea, with only 25% giving a hard no when asked if they’re open to using one. The rest of the millennials are equally split, with 37% responding yes and 37% answering maybe they’re open to using one. Baby boomers ages 57 to 76 are the least likely to embrace robo-advisors, with 57% saying they’re not open to using one, which is more than double the 25% of millennials who say no.

Men are warmer to robo-advisors than women, with just 31% of men saying they’re not open to using one, versus 42% of women. However, an almost equal percentage — 38% of men and 37% of women — say they may be open to the idea.

Also, the higher one’s income, the more open they are to using a robo-advisor. For example, while 41% of those who make less than $35,000 say they’re not open to using one, only 32% of those who make $100,000 or more say they’re not. Robo-advisor services are generally less personalized, so it’s interesting that the highest earners — likely those who can invest the most — are more open to it.

Even though robo-advisors aren’t for everyone, they offer some distinct advantages, according to MagnifyMoney executive editor Ismat Mangla. For one, they’re typically less expensive than working with a financial advisor, and they’re usually easy to access with low account minimums. They can also offer automatic rebalancing options so your asset allocation is always on target.

What you don’t get: Personal attention. “You’re not working with a human being, and that does come with its own limitations,” Mangla says.

It’s not that Americans aren’t investing. The majority — 57% — report some type of investments, be it stocks, bitcoin, retirement savings or something else. And they’re not all that opposed to risk. The majority of people with investments say their investing risk tolerance falls in the moderate range (53%), while 10% report an aggressive risk tolerance.

In general, the younger you are, the more aggressive you can be in saving for retirement, Mangla says. As you get closer to retirement, you probably want to take on less risk.

Investors embrace that line of thinking at least to some degree, as 44% of baby boomers who invest say their risk tolerance is conservative, while just 31% of Gen Zers ages 18 to 25 report the same. In the middle are 38% of Gen Xers ages 42 to 56 and 35% of millennials.

Will conservative investments help meet their goals? Well, that’s one thing financial advisors help people determine, along with other key factors. Still, only 41% of those with investments report having a financial advisor. In some cases, that may not be for want though, as 16% of these respondents say they don’t have a financial advisor but want to get one.

While an equal rate of men and women report having a financial advisor, there are greater differences among generations. Baby boomers with investments are significantly more likely to have one than Gen Zers — 50% versus 32%. However, millennials (42%) are more likely than Gen Xers (37%) to have one. Gen Zers are most likely to report not having a financial advisor but wanting one — 30%, versus 18% of millennials and Gen Xers and 6% of baby boomers who report the same.

Among those who invest, those who earn the biggest salaries are most likely to have a financial advisor, with 56% of those who make $100,000 or more having one, versus just 30% of those who make less than $35,000.

Why do people make the leap and enlist the help of a financial advisor? The biggest reason given: Help managing money and finances (65%). Other top reasons include helping with retirement (49%), discussing money goals (47%) and helping manage investment risk (45%).

As for how they get that help from their advisor, the telephone is key, with 79% of those with financial advisors saying they communicate via phone, while 62% say they communicate with their advisor in person. Communication via email (66%) is more prevalent than text (36%), with a meager few interacting via fax (4%).

Why don’t people have a financial advisor? Well, 44% say they’re too expensive, while 43% say it’s because they manage their own investments/finances. Other reasons cited include not having enough assets yet (31%), having yet to find an advisor they like (17%), being able to find plenty of free resources online (16%) and not trusting financial advisors (12%).

What kind of cost are we talking about? In most cases, financial advisor fees are a percentage of your assets under management (AUM), i.e., the value of the investments you’re asking them to manage. So, for example, if the annual AUM fee is 1.00% and you deposit $20,000, you’d pay $200 a year.

The percentage varies based on the advisor. But, in general, financial advisors charge a higher fee than robo-advisors. On average, financial advisors charge AUM fees of 0.59% to 1.18%, while robo-advisors’ average AUM fees run from 0.00% to 0.40%.

Are the fees worth it? The answer depends on your comfort with managing your own investments.

“If you need guidance from a professional because you don’t have the time or ability to learn on your own, then it can really pay off in the long run,” Mangla says.

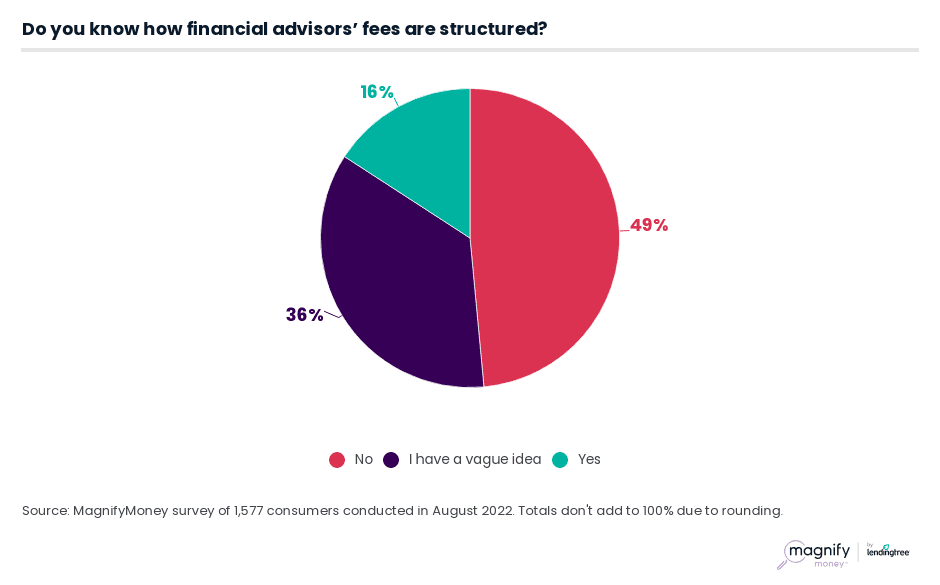

Also, while fees are important when choosing a financial advisor, our survey showed how few Americans really understand those fees.

The fact is nearly half (49%) of Americans say they don’t know how financial advisors’ fees are structured, while 36% say they have a vague idea about them. Only 16% say they understand them. Millennials and baby boomers are the most likely to say they understand advisor fees — 18% of each responded yes — while just 13% of Gen X and 11% of Gen Z respondents claim the same.

Almost all Securities and Exchange Commission (SEC)-registered advisors charge based on a client’s AUM, according to a 2022 snapshot from the Investment Adviser Association. But even though 95.5% charge based on AUM, only 17.4% of advisors charge only asset-based fees. Other fee types include fixed, hourly, performance, commission and subscription.

A lack of knowledge about fees can come at a significant cost.

“I always caution people to pay close attention to fees, because they can really eat into your returns,” Mangla says. “Make sure you know how much your financial advisor is charging and how.”

Many people also seem to think you need to have a significant amount of assets before you should get a financial advisor. Only 28% say you should get one if you have less than $25,000 in assets. Just over one-third of respondents say they think you need $100,000 or more.

When it comes down to it though, even though cost is the primary reason people cite for not having a financial advisor, low cost doesn’t top the list of the most important qualities people want in an advisor. It’s trustworthiness that’s most important, with 49% selecting it as most important, which is far ahead of the 16% who cited a high return on investments and 7% who cited low cost as the most important quality in an advisor.

Knowing what’s important to you is a good first step when choosing between a financial advisor and a robo-advisor. If you like in-person communication and aren’t as worried about fees, a financial advisor may be the way to go. If you’re OK with letting technology take the lead and want to save on fees, a robo-advisor may be right for you. Here are some other things to consider when deciding between the best robo-advisors and financial advisors:

Ultimately, finding a fiduciary advisor who is legally and ethically bound to have your best interests is important.

MagnifyMoney commissioned Qualtrics to conduct an online survey of 1,577 U.S. consumers ages 18 to 76 from Aug. 19-26, 2022. The survey was administered using a nonprobability-based sample, and quotas were used to ensure the sample base represented the overall population. All responses were reviewed by researchers for quality control.

We defined generations as the following ages in 2022:

Julie Ryan Evans

Julie Ryan EvansJulie Ryan Evans is a writer and editor who has covered small business, real estate and personal finance for nearly a decade. She has written for an array of publications, including USA Today, Realtor.com, LendingTree and Debt.com.

Read More