MagnifyMoney

First comes love. Then comes marriage. Then comes a joint bank account?

Many couples choose to merge their finances, so MagnifyMoney commissioned a survey of over 1,000 Americans regarding their feelings about doing so with a spouse or partner. About half of those surveyed are married or living with a partner.

The survey revealed that some feel regret or tension over combining their finances. Before you run along and open a joint bank account, keep reading for more findings. These are helpful discoveries when you consider that MagnifyMoney in 2017 found that 21% cited money as the cause of their divorce.

Joint bank accounts are not reserved solely for married couples. Those living with a partner can join their finances as well.

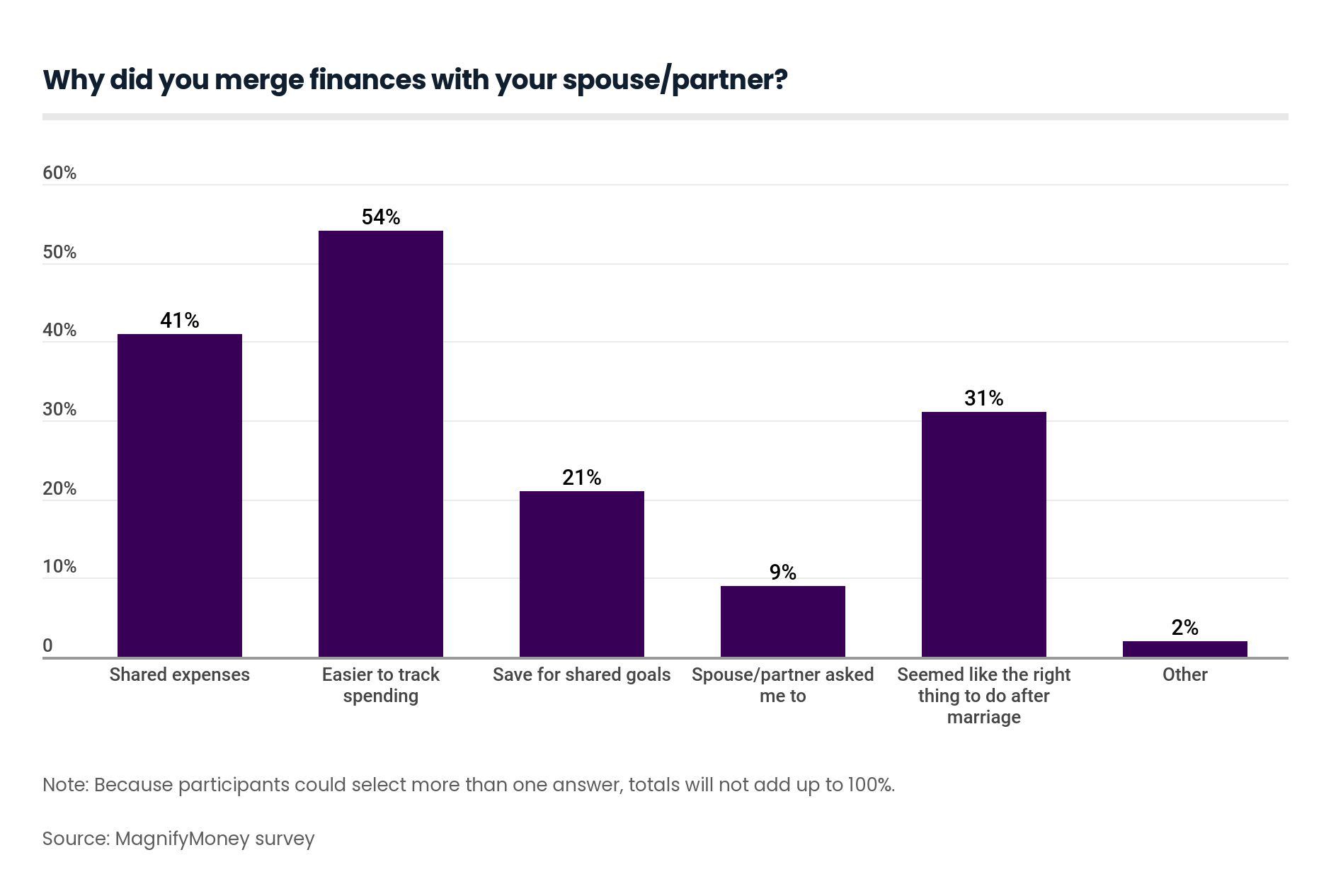

In fact, 43% of unmarried couples who live together have entirely joint bank accounts or at least have some of their money in a joint bank account with their partner. There is no guarantee married couples will merge their bank accounts either, as 16% keep separate bank accounts.

Even married couples who share bank accounts don’t necessarily combine all their finances. While 65% of married couples merged their financial accounts, 19% reported keeping some of their finances separate.

Couples are more likely to merge their finances on their own timeline. In fact, 69% of married couples opened their joint account after the wedding, while 16% did so after getting engaged. Even without marriage plans on the horizon, 13% chose to merge their finances after moving in together.

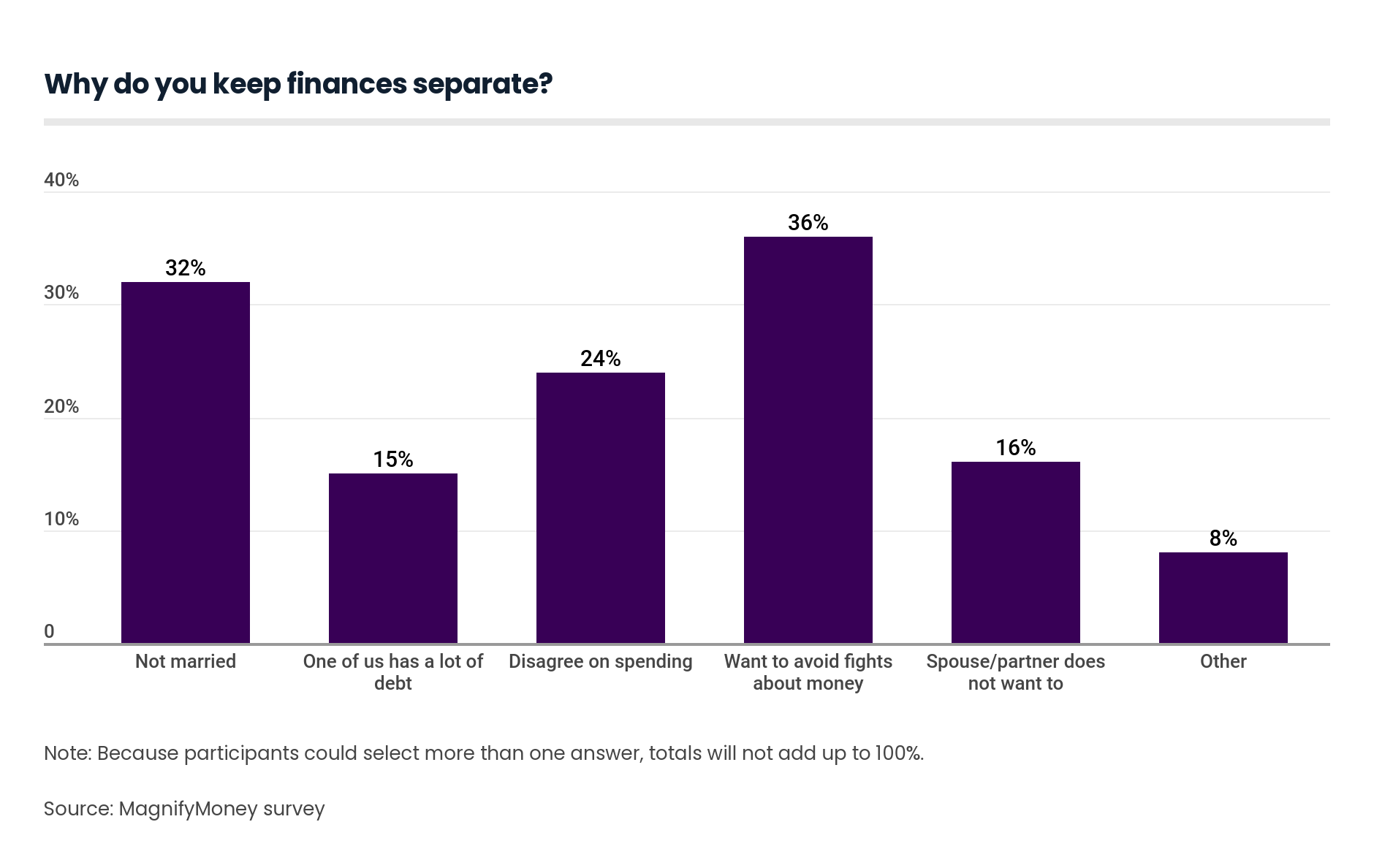

But not everyone is ready to jump on the shared finances bandwagon. Of those with separate accounts, 73% said they never plan on joining their finances. Meanwhile, 21% plan to combine their finances after marriage, with just 4% waiting for an engagement and 3% waiting until they have a child to do so.

As with other areas of life, couples can have varying opinions regarding how they should best manage their finances.

Whether couples are joining their finances, many still plan together financially. In fact, 30% of couples reported sharing responsibility for managing the household finances.

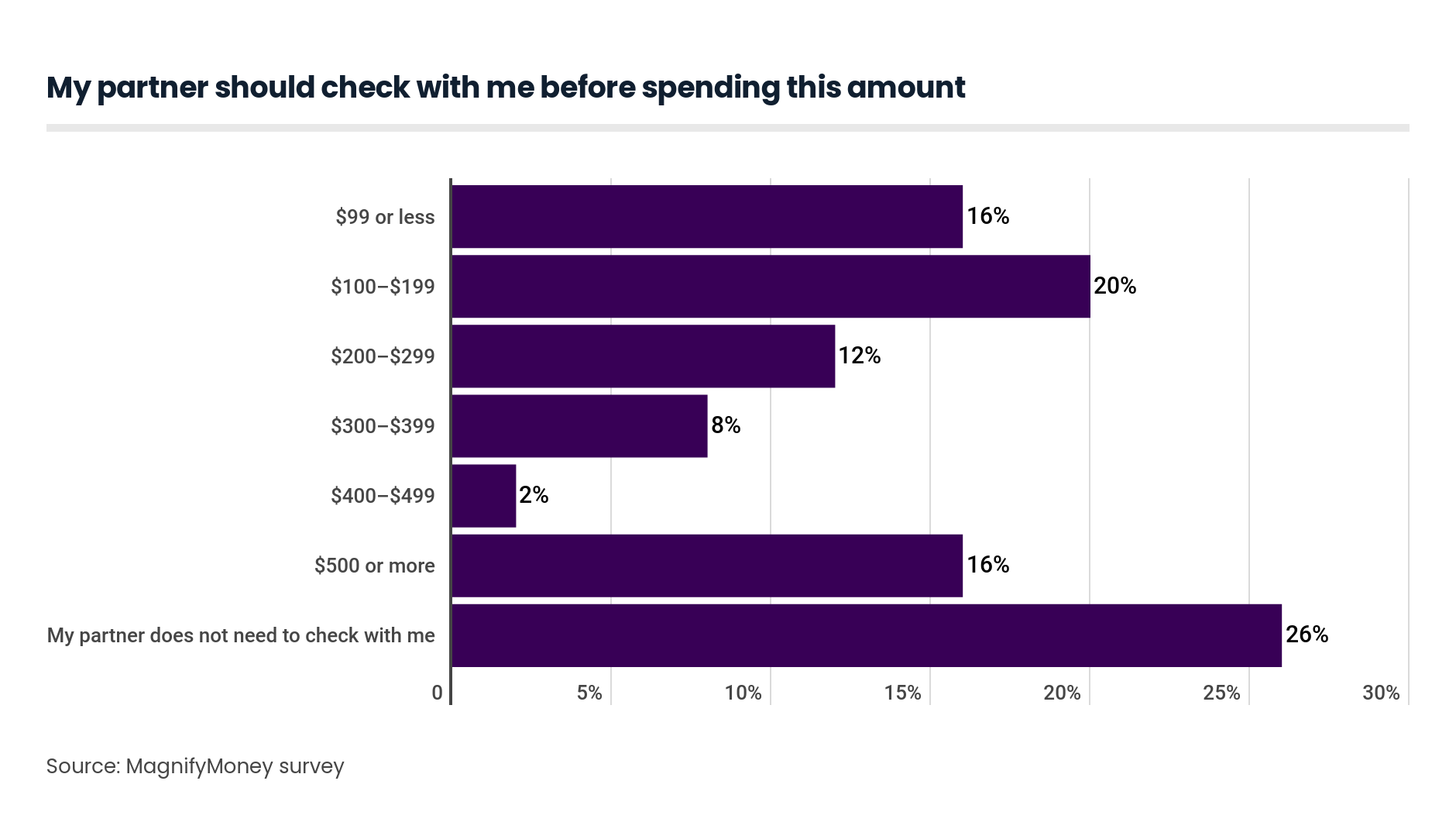

You might want to check with your beloved before you make a pricey purchase. Of those surveyed, 60% reported they would be angry if their partner or spouse spent $500 without telling them first. Women were even more likely to express anger if they weren’t informed of such a purchase.

Not being on the same page about what constitutes as overspending could lead to anger and resentment, which are feelings most couples would like to avoid. The amount that members of a couple are content with spending can vary.

Considering the fact that 36% of people feel their spouse or partner spends too much money, it’s wise to get on the same page and determine an appropriate budget.

| Earns more | Earns less | Earns the same | |

|---|---|---|---|

| Regret merging finances | 0.29 | 0.16 | 0.11 |

| Concerned spouse/partner spends too much | 0.42 | 0.34 | 0.28 |

| Argued about money within last month | 0.37 | 0.28 | 0.23 |

| Satisfied with how finances are managed | 0.63 | 0.59 | 0.7 |

Source: MagnifyMoney.com

For many couples, combining finances feels like a no-brainer. It’s just the next step after the honeymoon. But some couples may find that this seemingly obvious financial step doesn’t work for them.

In fact, 20% of couples reported regretting merging their finances with a spouse or partner. Those who earn more than their romantic partner feel more regret after merging finances. Almost 29% of respondents who earn more than their partner regret doing so. The higher-earning partners were also about twice as likely to report arguing with their partner about money at least once a week.

This is a reminder why it’s important to speak with your partner about important financial issues before you merge your lives together. Planning how you’ll work together to pay off debt, create an emergency fund, buy a home and manage your living expenses is an important part of keeping your relationship financially and emotionally healthy.

MagnifyMoney by LendingTree commissioned Qualtrics to conduct an online survey of 1,070 Americans, 573 of whom are either married or living with their partner. The survey was fielded July 26-30, with the sample base proportioned to represent the general population.

Jacqueline DeMarco

Jacqueline DeMarcoJacqueline DeMarco is a freelance writer who is particularly passionate about finance. She began her career in the retirement industry. Today, she works with more than a dozen financial brands to create entertaining and educational money content.

Read More