MagnifyMoney

Creating a monthly budget can help you track your spending, save money and reach your financial goals. However, many Americans don’t budget their money, perhaps because the prospect of combing through bank statements and bill payments can seem daunting.

It’s easier than you might think to learn how to make a budget. With the help of a reliable budgeting strategy and a little dedication, you’ll know how to manage your money in no time at all.

Here’s how to budget your money in five simple steps:

This first step is to find out how much money you bring in each month. Track down your pay stubs from the past few months for a more accurate picture. If you are married or sharing expenses with a partner, you’ll need to work together to figure out your joint income. Use your pay schedule to determine your monthly take-home income:

→ Semimonthly/monthly salaried workers: If you’re paid twice per month on static dates (like the 25th and the last day of the month), simply double your paycheck to determine your monthly income. If you get one paycheck per month, that is your monthly take-home income.

→ Weekly/biweekly salaried workers: If you’re paid weekly or biweekly (like every other Friday), keep in mind that some months you’ll get an extra paycheck, so you can’t simply multiply your paycheck by two or four to get your monthly income. Instead, use last year’s W-2 to divide your take-home income by 12. If you don’t have last year’s W-2, divide your gross annual income by 12 and then subtract taxes and payroll deductions, such as health insurance and retirement contributions.

→ Hourly and freelance workers: Since your paychecks may vary from month to month, do your best to estimate your monthly take-home income based on your invoices and pay stubs from the past few months.

This should include everything from big expenses, such as your mortgage or rent payment, to your “fun” money for eating out or spur-of-the-moment purchases.

Make note of your fixed expenses and your variable expenses. Your fixed expenses will stay static month over month, such as your cable bill, mortgage payment and any other fixed-rate installment loan payments you may have. Your variable expenses are a bit harder to estimate, and include purchases like groceries, clothing and utility bills.

See a list of common monthly expenses below:

| Fixed expenses | Variable expenses |

|---|---|

| Mortgage or rent payment | Groceries |

| Auto loan payment and insurance | Utilities, including electricity and water |

| Student loan payment | Out-of-pocket medical expenses |

| Internet, cable and streaming subscriptions | Transportation costs, like gas and train tickets |

| Health insurance premiums | Discretionary expenses, like clothing and home goods |

| Gym memberships | Entertainment, like dining out and event tickets |

| Cellphone bill | Gifts for holidays, anniversaries and birthdays |

Smartphone technology has made it easier than ever to create a budget and track your expenses. You can download many budget apps for free, although some offer premium features for a cost. Check out some popular budget apps available for download in the table below:

| App | Features | Cost |

|---|---|---|

| Albert |

| Free or $4+/month for Albert Genius |

| Mint |

| Free |

| You Need a Budget |

| $11.99/month or $84/year |

Reflect on your financial wellness in the past year to see how you’d like to improve. Did you take out more credit card debt than you’d like? Did you struggle to build your savings or emergency fund? You can tailor your budget so that it helps you reach your financial goals.

Here are a few simple budgeting solutions based on common money goals:

Some of the goals above are best achieved through specific budgeting strategies. See a few common ways to budget in the section below.

Once you’ve compiled your income and spending data and thought through your saving goals, it’s time to choose a budget style. Keep in mind that there is no best way to budget — any method that helps you manage your spending and save money will benefit you financially.

Best for: Growing your savings

The 50/30/20 rule is popular among personal finance experts because it’s a simple budget rule to determine if you’re overspending on discretionary purchases or if you should find a way to cut down on your living expenses. Here’s how it works:

Best for: Paying off debt

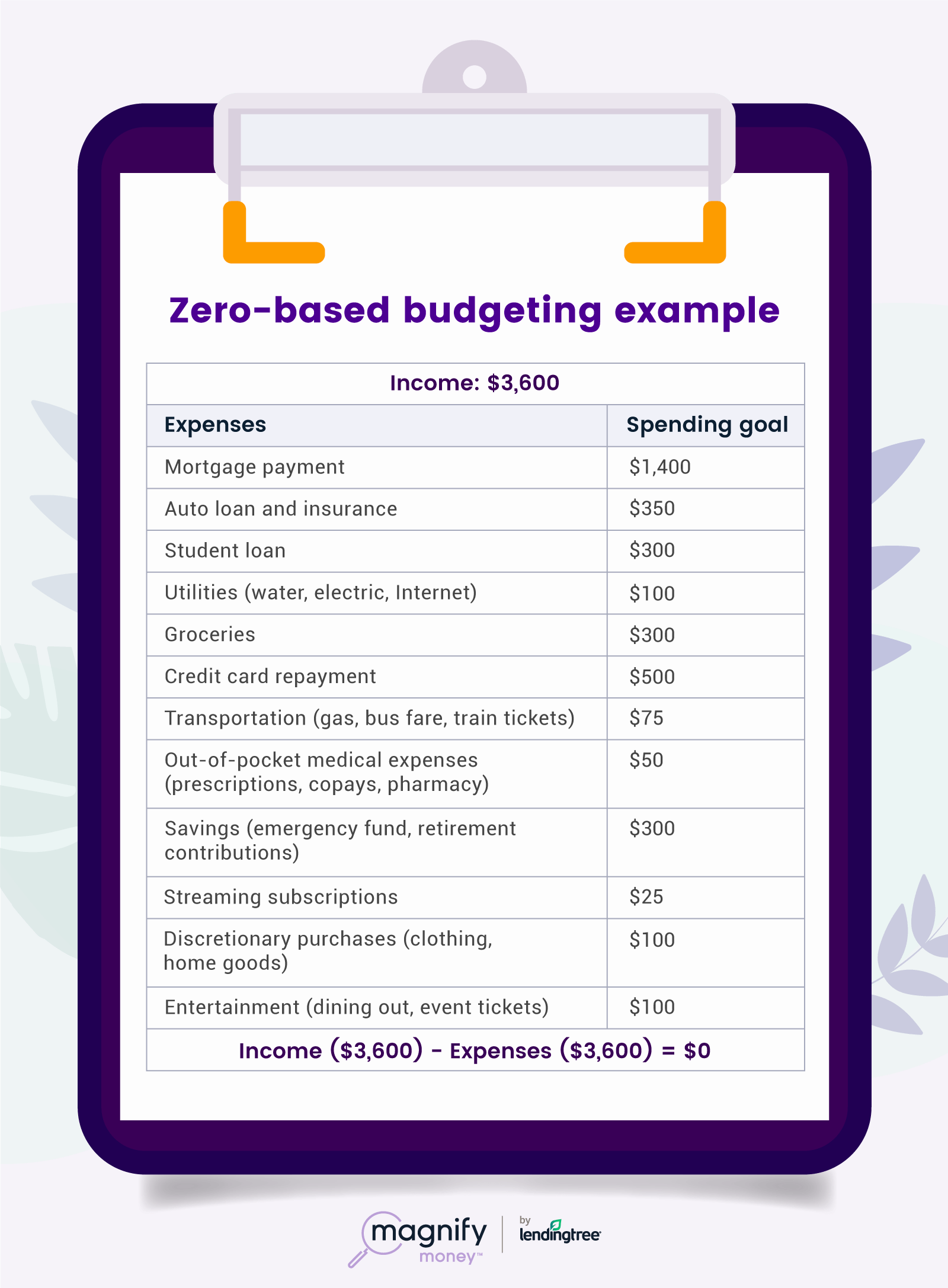

Give every dollar of your income a job by utilizing the zero-based budgeting strategy. Rather than just allocating all your “leftover” money to savings or repaying debt, you should set a specific repayment amount for these goals to help you reach them faster.

At the end of the month, your income minus your expenses should equal zero. Here’s how that looks in practice, with a focus on aggressive credit card repayment:

Best for: Cutting down on spending

You may have heard of your parents (or grandparents) putting cash in envelopes to create a budget and stick to it. You can still utilize this budgeting rule virtually. Categorize your spending using virtual “envelopes,” in which you allocate a set amount toward certain purchases.

Certain budgeting apps, such as Goodbudget, utilize the envelope method. This is similar to the zero-based budgeting method, in that you set a spending goal at the beginning of the month.

Creating a budget is only half the battle. Sticking to your budget will help you keep control of your finances throughout the year. Use these personal budgeting tips to help you stay on top of your money goals:

One of the most significant factors of your credit score is your on-time payment history. It’s easy to miss a payment, though, even if you account for a bill in your budget. Avoid missing payments altogether by setting up automatic bill payments. Many financial institutions let you manage automatic payments right in their app or online portal.

One of the most significant factors of your credit score is your on-time payment history. It’s easy to miss a payment, though, even if you account for a bill in your budget. Avoid missing payments altogether by setting up automatic bill payments. Many financial institutions let you manage automatic payments right in their app or online portal.

You can budget for many predictable expenses, but there are certain emergencies that you might not have in your monthly budget. For example, a pricey car repair or unforeseen medical expense can thwart even the most intricate budget.

You can budget for many predictable expenses, but there are certain emergencies that you might not have in your monthly budget. For example, a pricey car repair or unforeseen medical expense can thwart even the most intricate budget.

Experts agree that you should have three to six months’ worth of expenses in your emergency fund. Determine a goal for your emergency fund based on this rule of thumb, and contribute a set amount of savings from your budget into this fund until you’ve reached your goals. Once you have a sufficient emergency fund, you can use extra income to repay more toward your debts or save up for retirement.

Unexpected expenses will crop up, which likely means you’ll need to reevaluate your budget. Or, you may find yourself spending more in one category than you anticipated, and you’ll need to reduce another category to make up for it.

Unexpected expenses will crop up, which likely means you’ll need to reevaluate your budget. Or, you may find yourself spending more in one category than you anticipated, and you’ll need to reduce another category to make up for it.

If you stray from your budget, don’t give up or punish yourself. Give yourself a reward if you have a little space in your budget at times. Get that take-out meal or buy that small item you’ve had your eye on.

The most important factor in budgeting is that you do it. Take the time to organize your financial information, track your spending, and personalize a budget style to fit your needs.

Erika Giovanetti

Erika GiovanettiErika Giovanetti is the debt and personal loans writer for LendingTree. She has reported on a multitude of subjects, from personal finance to human interest to politics.

Read More