MagnifyMoney

Congress Wealth Management is a registered investment advisor (RIA) headquartered in Boston with additional locations across the U.S. The firm describes itself as a “manager of managers,” as it often invests client funds with other investment managers. It also offers financial planning and family office services. The firm’s clients are largely high net worth individuals.

The bottom line: Congress Wealth Management is largely a “manager of managers” that focuses on investors who have at least $1 million to place with the firm.

| Assets under management (AUM): $3,040,622,381 | |

| Minimum investment: $1 million | |

| Individual investor to advisor ratio: 52:1 | |

| Fee structure: A percentage of AUM, fixed fees | |

| Headquarters: 155 Seaport Blvd, 3rd Floor Boston, MA 02210 Website: www.congresswealth.com Phone: 617-428-7600 |

All information included in this profile is accurate as of March 28, 2022. For more information, please consult Congress Wealth Management’s website.

Congress Wealth Management, which operates as a Delaware LLC, was established in 2020. It was previously registered under the same name as a Massachusetts LLC, which was established in March 2009, at the height of the global financial crisis. Today, the firm is primarily owned by Harborview Partners 2012, LLC, CI US Holding, Inc., and Lagan Wildwood Investments LLC.

The firm has over 30 employees, nearly 20 of whom provide investment advisory functions. Several of the firm’s employees hold the chartered financial analyst (CFA) designation.

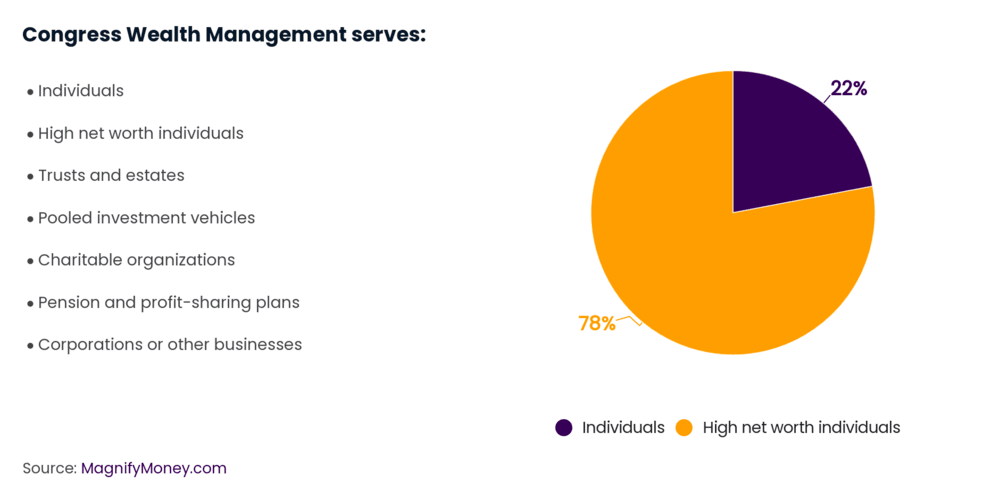

The vast majority of the firm’s AUM currently comes from serving high net worth individuals. However, they also work with a number of non-high net worth individuals. The firm has clients from a variety of industries including technology, medicine, higher education, entertainment and finance. The firm also takes clients from a range of backgrounds and ages.

To work with the firm, a client must have at least $1 million in investable assets. However, they can also make exceptions at its discretion based on factors including a client having a longstanding relationship with the firm, expectations that the client will grow their AUM and the type of strategy and investment advisor a client selects.

Congress Wealth Management primarily provides investment and wealth management services. Nearly all of the firm’s clients use a discretionary management system, meaning your advisor has the authority to make trading decisions on their behalf. Only a small number of the firm’s accounts are non-discretionary, which means the client must approve all trades.

The firm often works as a “manager of managers” for its clients, meaning it builds a portfolio of funds run by outside advisors and then supervises the arrangement to make sure it meets their clients’ goals.

The firm also offers financial planning services, both as part of one of its investment management agreements or as a standalone service. For extremely high net worth clients, they also offers a family office service to help with more complex issues such as estate planning, charitable giving and wealth distribution.

Here is a full list of services offered by the firm:

Advisors create a customized portfolio for each client based on their goals, risk tolerance, time horizon, cash flow needs and other factors. The firm’s investment philosophy is centered on the belief that returns come from a portfolio’s overall asset allocation. Rather than trying to pick individual stocks, bonds and other investments that might generate higher returns, advisors focus instead on finding the right balance of different assets for its clients.

The firm does this by dividing client portfolios into two parts, known as a Core and Satellite approach. The first part focuses on core strategies and invests in more traditional assets, including the following:

The second part is allocated to satellite strategies, which invest in more exotic and riskier but potentially higher-earning assets, such as:

Since the firm often uses funds from outside investment managers for these strategies, it performs due diligence on each outside advisor to make sure they can meet a client’s goals. Congress Wealth Management then reviews the arrangement at least once a year to make sure the outside manager continues to be a good fit.

The firm primarily charges for its portfolio management services based on a fixed percentage of a client’s assets under management. When someone signs up, the firm will set their rate based on the size of their portfolio, the complexity of their account and the strategies and managers they want to use.

The client’s rate will also depend on whether they only hire Congress Wealth Management, in a single contract agreement, or if they work with an outside investment manager recommended by Congress Wealth Management under a dual contract agreement. The firm charges a lower fee for dual contracts because the outside investment manager will charge its own fee in addition to the fee charged by Congress Wealth Management.

| Congress Wealth Management Fee Schedule | |

|---|---|

| Contract agreement | Annual asset-based fee |

| Dual contact agreement (Congress Wealth Management plus an outside investment manager) | Between 0.50% to 1.00%, plus the outside manager’s fees |

| Single contact agreement (only Congress Wealth Management) | Between 0.65% to 1.25% |

Additionally, clients will cover investment fees in their portfolio, though that money will not go to Congress Wealth Management.

Generally, financial planning is included under the firm’s wealth management fee. However, for services beyond the usual scope in terms of depth and breadth, the firm may charge an additional fee as either a percentage of assets under management or as a fixed fee. The rate is negotiable.

For family office services, fees are generally based on a percentage of assets under management, though in some cases may include a fixed fee where an asset-based fee wouldn’t be appropriate. The rate is negotiated between the advisor and the client and depends on the size, complexity and breadth of the client’s needs.

Congress Wealth Management has one disciplinary disclosure on its Form ADV. If a firm registered with the Securities and Exchange Commission (SEC) faces some sort of serious disciplinary action, whether a criminal charge, a government sanction or a lawsuit, the firm must report what happened on its Form ADV, paperwork that all registered firms must file with the SEC.

The disciplinary disclosure was the result of an SEC fraud case brought against another investment manager, F-Squared Investments, Inc., in December 2014. F-Squared admitted to making false claims about its AlphaSector Index strategy and its performance. The firm invested some of its client assets in this strategy from May 2009 to Oct. 2013 and repeated F-Squared’s claims about investment performance in its marketing materials. In December 2013, Congress Wealth Management began to question the accuracy of F-Squared’s claims and terminated the relationship.

Still, the SEC believed that the firm was negligent by publishing this inaccurate information in its materials. The firm didn’t admit to any wrongdoing but agreed to pay a $100,000 fine to settle the matter.

For more information, visit the firm’s Investment Adviser Public Disclosure (IAPD) page.

The firm has offices in the following cities:

If you can meet the $1 million investment minimum and want a customized, sophisticated portfolio, Congress Wealth Management could be a good fit. The firm’s highly credentialed team goes beyond the standard asset classes of stocks and bonds and instead uses more sophisticated products in an attempt to increase returns. Since the firm partners with outside investment managers, this also provides more options for designing portfolios.

But this approach does have its downsides. Fees can be higher than average at Congress Wealth Management, and you won’t know exactly how much you may end up paying until you meet with a representative. Be sure to research multiple firms to ensure you find the right advisor for you.

David Rodeck

David RodeckDavid Rodeck is a financial freelance writer for MagnifyMoney. He has been writing for over a decade and also contributes to Forbes Advisor, Kiplinger and other financial publications. Before writing full-time, David was a financial advisor.

Read More