MagnifyMoney

Most people experience regret at some point in their lives, like remorse over past relationships or unnecessary impulse purchases. Investing, it turns out, is also not immune to feelings of regret.

A new survey from MagnifyMoney found that the biggest regret among Americans is not investing sooner. Even many members of Gen Z (ages 18 to 22), who have time on their side, feel that they should have invested sooner.

The biggest investing regret among the respondents in this survey was procrastination. Our survey found that an overwhelming number of Americans (77%) regret not investing earlier in life. The most common regrets were not saving for retirement sooner (31%) and not investing in stocks sooner (24%).

| Americans' investing regrets | ||

|---|---|---|

| Not saving for retirement sooner | 0.31 | |

| Not investing in stocks sooner | 0.24 | |

| Not purchasing a certain stock earlier | 0.21 | |

| Selling a stock too early | 0.16 | |

| Hold on to a stock for too long | 0.14 | |

| Taking money out of retirement account | 0.14 | |

| Not monitoring portfolio | 0.09 | |

| Putting too much money in an individual stock | 0.09 | |

| Not diversifying portfolio | 0.1 | |

| Trading too frequently | 0.07 | |

| Not using an investment advisor | 0.07 | |

| Basing investment decisions on the news | 0.07 | |

| Other | 0.02 | |

Source: MagnifyMoney survey, 2019

Note: Respondents could select more than one answer, so totals will not add up to 100%

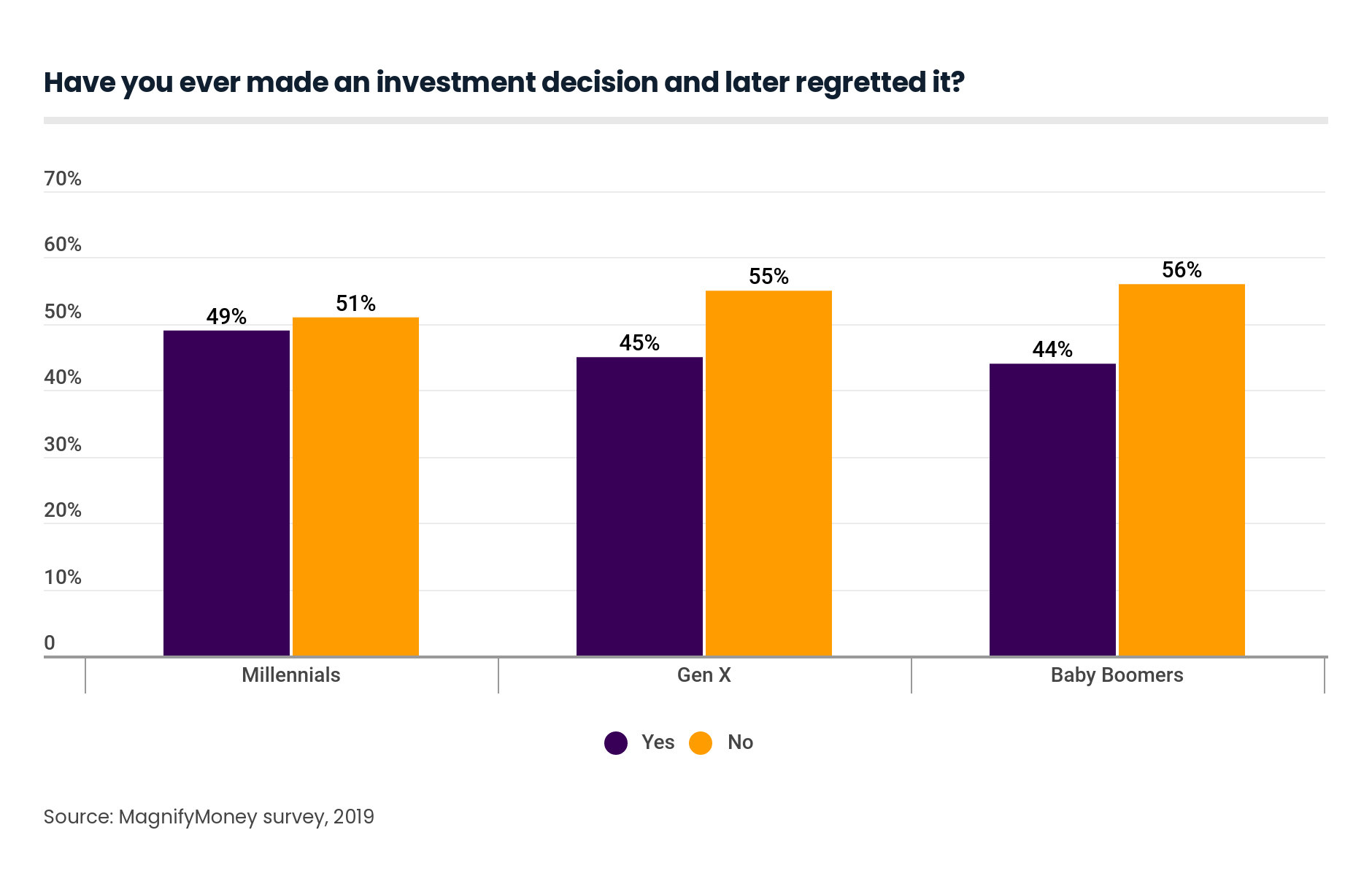

It’s noteworthy that this sentiment remained true across generations, with younger respondents also saying they regretted not investing earlier, including 69% of Gen Zers and 77% of millennials. For millennials, that’s even more than the 76% of baby boomers who said they regretted not investing earlier.

Other common investing regrets among Americans include not purchasing a certain stock earlier (21%), selling a stock too early (16%), holding on to a stock for too long (14%), taking money out of a retirement account (14%), not diversifying their portfolio (10%), not monitoring a portfolio enough (9%), putting too much money in an individual stock (9%), not using an investment advisor (7%), trading too frequently (7%) and basing investment decisions on the news (7%).

Another plot twist revealed by the survey: While 7% of Americans say they regret not using an investment advisor, people with paid financial advisors reported having more investment regrets than those without one (59% versus 41%). Apparently, money can’t buy satisfaction.

Rest assured, even if you’re in the camp of having investing regrets, don’t beat yourself up — 65% of Americans say that investing will “inevitably” lead to some regrets, according to the survey. Seasoned investors know this to be true: Investing is a long game, characterized by ups and downs that even out over the long term.

With so many Americans wishing they had invested earlier themselves, it makes sense that the most popular piece of advice baby boomers have for younger Americans is to start investing as soon as possible (61%).

Other nuggets of wisdom baby boomers say they would pass down to younger generations include to prioritize retirement savings (20%), followed by diversifying your portfolio (7%) and trying not to base your investment decisions on emotions (5%).

Only 3% of baby boomers wound advise young people to hire a financial advisor, 2% would say don’t fear the stock market, and just 1% would say learn the power of inflation.

The urgency to invest sooner rather than later is due to a core investing concept: compounding returns. Time is of the essence when investing, because the longer you let your investments compound, the more money you’ll generate over time. Your returns build on existing returns. Compounding is like a snowball rolling downhill: The longer it rolls, the bigger it gets.

Thanks to the power of compounding, for example, you could turn $50 a week into nearly $40,000 after 10 years, assuming an average return of 8% — giving the term FOMO (fear of missing out) an entirely new meaning.

If you’re a newbie investor and decide it’s time to finally pull the trigger, the first step to take is to research. Learn about the different types of investments and asset classes that are available to you, determine how much risk you’re able to stomach and take a look at your budget to determine how much you can comfortably put toward an investment fund.

There are also platforms that are best for first-time investors, which incorpare built-in tools that teach you to invest. Micro-investing apps, for example, allow you to invest your spare change in exchange-traded funds (ETFs). While investing on a small scale won’t make you rich, it’ll help you get into the habit of funneling your money into investments instead of personal spending.

One of the easiest ways you can start investing is by enrolling in your workplace-sponsored retirement plan, if you have one. Typically, the money you invest in this fund will be deducted from your paycheck pretax, so you won’t be tempted to spend that cash on something else. An added bonus: Many employers will match your contributions up to a certain amount.

MagnifyMoney by LendingTree commissioned Qualtrics to conduct an online survey of 836 consumers with an investment account. The survey was fielded Sept. 11-13 and Dec. 3-4, 2019, with the sample base proportioned to represent the general population. Generations are defined as: Generation Z ages 18-22, millennials ages 23-38, Generation Xers ages 39-53 and baby boomers ages 54-73.

Sarah Berger

Sarah BergerSarah Berger is a former writer at LendingTree, where she covered personal finance, specifically focusing on challenges and opportunities facing millennials. Before joining LendingTree, she was a writer for CNBC and Bankrate.

Read More