MagnifyMoney

Options are one of the most exciting areas of the investing world because of their potential for huge gains. But to get started, you’ll want to know what options strategies are available, when they’re best suited to particular situations and what the risks and rewards are.

Options strategies come in a variety of flavors, but they’re all based on the two fundamental options: calls and puts. From these basics, investors can create a range of strategies that maximize the payout from a stock’s movement and savvy investors pick the strategy that’s best for how they expect the stock to perform.

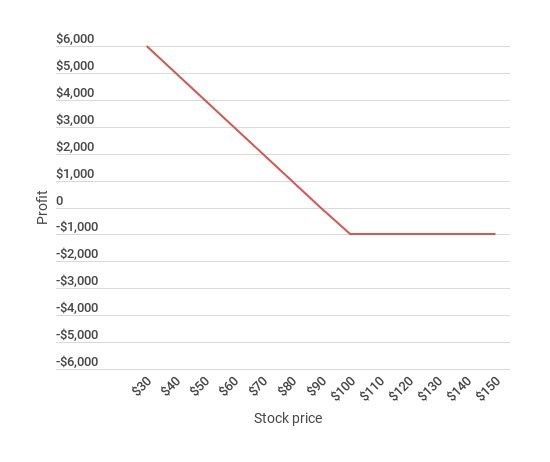

The long put is an options strategy where the trader buys a put expecting the stock to be below the strike price before expiration.

Best to use when: The long put is a useful strategy when you expect the stock to decline and you want to earn a large upside. Traders will earn a significantly better return on their investment than by short selling the stock, so a long put could be a good substitute for shorting the stock directly. The long put also limits the short seller’s loss to the premium, while shorting the stock exposes the trader to uncapped losses.

Example of the long put: STK stock trades at $100 per share, and puts with a $100 strike price are available for $10 with an expiration in six months. One put costs $1,000 (one contract * 100 shares * the $10 premium).

Here’s the return at each stock price, including the cost to set up the position.

| Stock price at expiration | Long put’s profit |

|---|---|

| $130 | -$1,000 |

| $120 | -$1,000 |

| $110 | -$1,000 |

| $100 | -$1,000 |

| $90 | $0 |

| $80 | $1,000 |

| $70 | $2,000 |

Risk/reward: The long put can pay off significantly if the stock moves below the strike price before the option expires. In this example, the maximum return is 10 times the original investment, or $10,000. In general, the maximum value of the long put equals the total value of stock underlying the trade (the number of contracts * 100 * the strike price).

The risk for this potential upside is a complete loss of the premium paid for the put. But if the stock moves higher, making the put less valuable, traders often can salvage some of the value by selling the put, as long as it has substantial time to expiration.

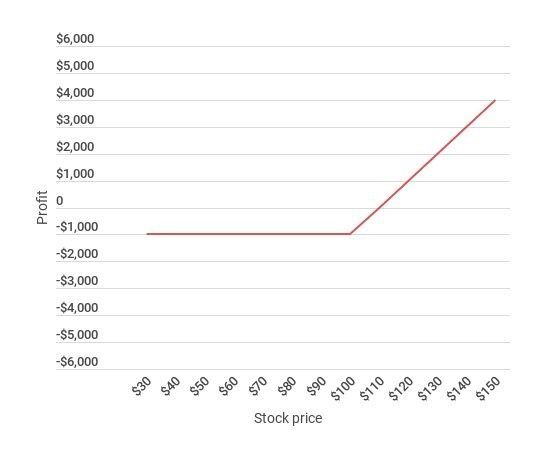

With the long call, the trader buys a call expecting the stock to be above the strike price before expiration.

Best to use when: The long call is much like the long put, but it pays out when the stock rises. So if you’re expecting the stock to move higher, the long call is the way to go. The long call can earn a much higher percentage return than owning the stock directly.

Because the trader’s downside is limited to the option’s premium, the long call also could be a good strategy if the stock has the potential to move much higher but has the potential to move much lower too. If the stock falls, the option’s limited loss could be less than owning the stock directly.

Example of the long call: STK stock trades at $100 per share, and calls with a $100 strike price are available for $10 with an expiration in six months. One call costs $1,000 (one contract * 100 shares * the $10 premium).

Here’s the profit at each stock price, including the cost to set up the position.

| Stock price at expiration | Long call’s profit |

|---|---|

| $130 | $2,000 |

| $120 | $1,000 |

| $110 | $0 |

| $100 | -$1,000 |

| $90 | -$1,000 |

| $80 | -$1,000 |

| $70 | -$1,000 |

Risk/reward: The long call has uncapped upside as the stock moves higher, and that’s why this strategy can be a home run. If a stock rises, you can make many times your investment.

Like the long put, the risk here is that the investor could lose all of the premium paid for the call. However, if the stock moves lower — making the call less valuable — traders often can save some of the value by selling the call, as long as it has substantial time remaining to expiration.

In a short put, the trader sells a put expecting the stock to be higher than the strike price by expiration. This is similar to selling insurance against the stock falling below the strike price.

Best to use when: There are two good situations for the short put.

Example of the short put: STK stock trades at $100 per share, and puts with a $100 strike price are available for $10 with an expiration in six months. One put generates a total premium of $1,000 (one contract * 100 shares * $10 premium).

Here’s the profit at each price, including the cost to set up the position.

| Stock price at expiration | Short put’s profit |

|---|---|

| $130 | $1,000 |

| $120 | $1,000 |

| $110 | $1,000 |

| $100 | $1,000 |

| $90 | $0 |

| $80 | -$1,000 |

| $70 | -$2,000 |

Risk/reward: The short put’s maximum payoff is the premium received by the trader. The stock might fall well below the strike price, but all the short put earns is the premium. The maximum payoff occurs anywhere above the strike price.

The downside for the short put can be substantial, and the trader can be forced to add money in order to close out the trade if there’s not enough to purchase the stock at the strike price. The maximum downside occurs when the stock goes to zero. In this example, the put would lose $10,000 (100 shares * the $100 stock * the one contract), though the investor would still have the $1,000 premium. Short puts can be risky with limited upside.

In order to create a covered call, the trader sells call options for each 100 shares of the underlying stock owned. The investor expects the stock to remain relatively flat, allowing the call to expire worthless. This allows the trader to pocket the premium without having to sell the stock at the strike price.

Best to use when: The covered call can be an effective strategy for generating income when the investor owns the stock and expects it to remain relatively flat over the life of the option.

The covered call also can be an “exit strategy” for a position, with the investor selling calls for a strike price that they would be willing to receive and getting to pocket the extra premium.

Example of the covered call: STK stock trades at $100 per share, and calls with a $100 strike price are available for $10 with an expiration in six months. One call generates $1,000 in premium (one contract * $10 premium * 100 shares), and the investor sells one call for each 100 shares of the stock owned.

Here’s the return at each stock price, including the cost to set up the position.

| Stock price at expiration | Stock’s profit | Call’s profit | Total profit |

|---|---|---|---|

| $130 | $3,000 | -$2,000 | $1,000 |

| $120 | $2,000 | -$1,000 | $1,000 |

| $110 | $1,000 | $0 | $1,000 |

| $100 | $0 | $1,000 | $1,000 |

| $90 | -$1,000 | $1,000 | $0 |

| $80 | -$2,000 | $1,000 | -$1,000 |

| $70 | -$3,000 | $1,000 | -$2,000 |

Risk/reward: The covered call’s maximum payoff is the premium received. This occurs right at the strike price, allowing the option seller to keep the premium without having to sell the underlying stock or losing any money on it.

There are two potential downsides for the covered call.

When using a married put, the trader buys put options on a stock for each 100 shares of the underlying stock owned. The investor suspects the stock may fall in the short term but wants to continue owning it because it may rise significantly. So the married put protects the investor’s downside.

Best to use when: There are two scenarios where the married put works well.

Example of the married put: STK stock trades at $100 per share, and puts with a $100 strike price are available for $10 with an expiration in six months. One put costs $1,000 (one contract * $10 * 100 shares), and the investor buys one put for each 100 shares of the stock owned.

Here’s the return at each stock price, including the cost to set up the position.

| Stock price at expiration | Stock’s profit | Put’s profit | Total profit |

|---|---|---|---|

| $130 | $3,000 | -$1,000 | $2,000 |

| $120 | $2,000 | -$1,000 | $1,000 |

| $110 | $1,000 | -$1,000 | $0 |

| $100 | $0 | -$1,000 | -$1,000 |

| $90 | -$1,000 | $0 | -$1,000 |

| $80 | -$2,000 | $1,000 | -$1,000 |

| $70 | -$3,000 | $2,000 | -$1,000 |

Risk/reward: The married put’s maximum total profit is unlimited if the stock moves higher. The whole point of the married put is to allow the investor to gain the potential upside by paying for “insurance.” If the stock moves lower, then the put increases in value to offset that loss.

The maximum downside is the lost premium. The married put is a hedged position, and the investor expects to lose money on one end of the hedge. The trader pays the option’s premium, and if that’s the maximum loss, then it’s a good thing.

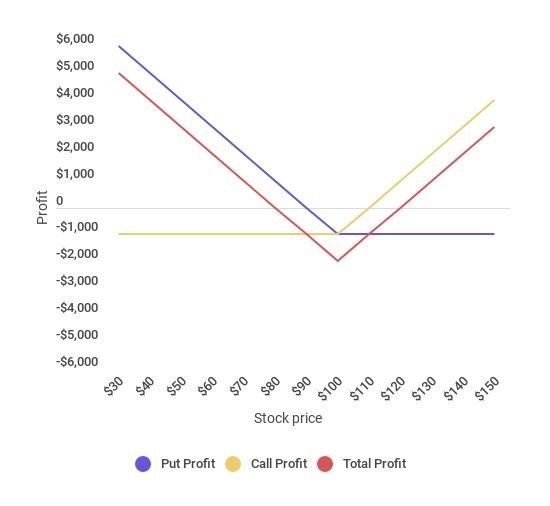

The long straddle is a strategy where the trader buys an at-the-money call and an at-the-money put with the same expiration and the same strike price. The trader suspects the stock may move significantly but is not sure in which direction.

Best to use when: The long straddle is a strategy that’s useful when you expect the stock to be volatile but it’s difficult to determine which direction it’s going. A long straddle costs a lot to set up and requires a big move in order to profit.

Example of the long straddle: STK stock trades at $100 per share. There are puts and calls with a $100 strike price available for $10 with an expiration in six months. The total cost of the trade is $2,000, consisting of the put (one contract * $10 * 100 shares) and the call (one contract * $10 * 100 shares).

Here’s the profit profile, including the cost to set up the position.

| Stock price at expiration | Call’s profit | Put’s profit | Total profit |

|---|---|---|---|

| $130 | $2,000 | -$1,000 | $1,000 |

| $120 | $1,000 | -$1,000 | $0 |

| $110 | $0 | -$1,000 | -$1,000 |

| $100 | -$1,000 | -$1,000 | -$2,000 |

| $90 | -$1,000 | $0 | -$1,000 |

| $80 | -$1,000 | $1,000 | $0 |

| $70 | -$1,000 | $2,000 | $1,000 |

Risk/reward: The long straddle can return a lot, and theoretically the return is uncapped if the stock soars. However, any profit will have to deduct the substantial cost to set up the trade, and this trade requires a stock to move big to make it profitable.

The downside of the long straddle is the complete loss of the premiums paid if the stock doesn’t move. However, if the stock moves even a little bit in either direction, the trader usually can recover some of the premium if there’s enough time until expiration on the options.

The long strangle is like the long straddle, but it’s cheaper to set up because it uses out-of-the-money options instead of at-the-money options. In the long strangle, an investor buys a call and a put option at prices above and below the current stock price, respectively. The trade-off, relative to the straddle, is that the stock must move even more for the strategy to work.

Best to use when: The long strangle is used when you expect the stock to move even more than you would when using a long straddle. So if you expect a big move in the stock, the long strangle can be cheaper to set up and deliver a higher percentage return than the straddle.

Example of the long strangle: STK stock trades at $100 per share, and puts with a $90 strike price are available for $5 with an expiration in six months. Calls with a $110 strike price are available for $5 with an expiration in six months. The total cost of the trade is $1,000, consisting of the put (one contract * $5 * 100 shares) and the call (one contract * $5 * 100 shares).

Here’s what the trade will return at expiration, including the cost to set up the position.

| Stock price at expiration | Call’s profit | Put’s profit | Total profit |

|---|---|---|---|

| $130 | $1,500 | -$500 | $1,000 |

| $120 | $500 | -$500 | $0 |

| $110 | -$500 | -$500 | -$1,000 |

| $100 | -$500 | -$500 | -$1,000 |

| $90 | -$500 | -$500 | -$1,000 |

| $80 | -$500 | $500 | $0 |

| $70 | -$500 | $1,500 | $1,000 |

Risk/reward: Like the long straddle, the long strangle can return a high percentage, theoretically uncapped if the stock rises. Similarly, it’s also a wager that the stock will move significantly in either direction, without the investor having a clear sense of which way. The main advantage of the strangle over the straddle is that it requires less money to set up.

The maximum downside of the long strangle is the complete loss of the premiums paid if the stock fails to move much. Because the options were purchased out of the money, it takes a more significant move to recapture some of the premium, though it is possible if time remains on the options.

There are a plethora of options trading strategies, and common ones that are often recommended for beginners include straddles and strangles, covered calls and selling iron condors. Earlier in this article, you’ll find more in-depth explanations and examples of seven popular options trading strategies.

When you trade options, you have the potential to make money in several different ways. This includes locking in a price for a stock for a specified period of time without actually having to commit to buying the stock, buying stock at some point in the future for a discounted price and generating income for stocks in your current portfolio.

James F. Royal, Ph.D.

James F. Royal, Ph.D.James F. Royal, Ph.D. is an expert in finance and a former stock analyst, and he makes this world easily accessible to readers. His work has appeared in the New York Times, the AP, and the Washington Post.

Read More