MagnifyMoney

Despite the growing prevalence of women in the workforce, the median earnings of women over the age of 25 was $32,679 in 2017, with men’s median earnings for that same age group at $46,152, per U.S. Census Bureau data, who estimated that women only earn nearly 71% of their male counterparts.

The reasons for this discrepancy are stridently debated, with theories ranging from personal preferences to mismatched family responsibilities, cultural pressure, institutional compensation or advancement bias. Whatever combination of factors are keeping women’s pay low, the fact remains that female workers make less than their male counterparts — both at work and at home.

Our new analysis takes a closer look at pay differences between men and women to see how it affects couples. To find out whether some places are more likely to have a balance between male and female breadwinners, we analyzed microdata from the American Community Survey conducted by the U.S. Census for the 50 largest metros in the country.

In an ideal world, men and women would be equally likely to be the breadwinner of a couple. But our analysis found that in the 50 largest metros, women were the main breadwinner in less than 31% of couples’ households.

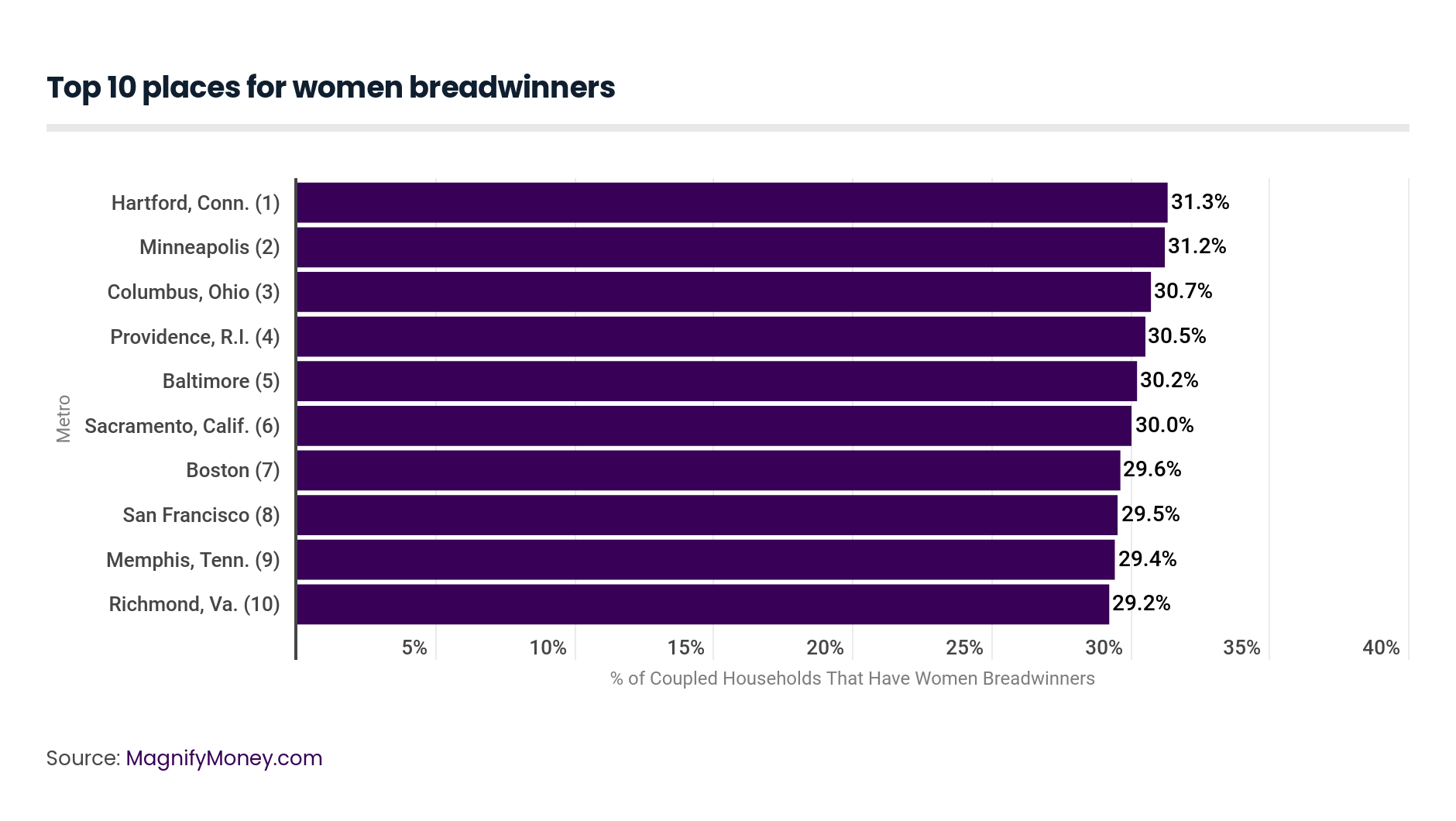

In the 10 major U.S. cities with the highest rates of couples with female breadwinners, roughly three in 10 couples have a woman earning more than her partner.

This is a contrast to other surveys that have found higher rates of female breadwinners, such as 49% of women who said they were the primary breadwinner in an NBC News-Wall Street Journal poll. The difference in these findings could be attributed to single women or single mothers who are the household’s sole income earners. Women may be more likely to be breadwinners in these surveys that include those who report they’re not competing with a partner for that title.

When they are paired up, however, our analysis shows that women are less likely to be the higher earner. Here’s a closer look at the 10 major U.S. cities that had the highest rates of female breadwinners.

Women who are partnered up are the most likely to be the breadwinner if they live in Hartford. Here, 31.3% of coupled women outearn their partner. This could be thanks to the higher parity of pay in this city, where the gap between men and women’s earnings shrinks to just 17.8%.

Next is Minneapolis, which has almost the same rate of female breadwinners, with 31.2% of coupled women earning more than their partners.

Minneapolis also took the No. 2 spot in our ranking of the best cities for working women. Its high ranking is due to a number of factors, but it’s a true standout for low unemployment among women and decent workplace protections for pregnant women and mothers.

In Columbus, 30.7% of partnered women are the breadwinners. Overall, women here make about $0.19 less per dollar than their male counterparts, well in line with the average among all 50 cities included in this analysis.

Providence, R.I. has a female breadwinning rate of 30.5%. This is no surprise, given that it was the eighth-best city for working women in our 2018 study.

While the gender pay gap is above average here, at 19.9%, Providence has above-average rates of women in management positions along with better policies for maternity and parental leave.

Among women in Baltimore who are part of a couple, 30.2% outearn their partners. Here, women earn just 18.8% less than men, giving them a better chance of landing pay that beats their significant other’s salary.

The third-best city for working women, Sacramento, also has one of the highest rates of female breadwinners: 30.0%.

It offers a lower pay gap between genders, with women earning just 14.6% less than men. Sacramento also gets a boost from California’s robust policies and benefits for pregnancy, maternity and family leave.

Boston is the next city with the highest rate of coupled households for which women are the breadwinners, at 29.6%. The gender pay gap here is 18.9%, which is just below average.

Next is another top city for working women, San Francisco. Here, the gap in median pay by gender is 18.7% and women outearn their partners 29.5% percent of the time. As another Californian city, women workers in San Francisco are also likely to benefit from strong parental and family work policies.

In Memphis, women are the breadwinners in 29.4% of couples’ households — that’s despite its ranking as the second-worst city for women. It has just a few redeeming factors, however, such as the above-average number of female managers and the below-average childcare costs in Memphis.

Couples in Richmond are among those most likely to be led by a female breadwinner, with 29.2% of women out-earning their partners. Women here earn $0.19 less for every $1 male workers earn, only slightly above the average. Still, working women in Richmond are more likely to receive employer-provided health care and more affordable child care costs, which can offset this pay gap.

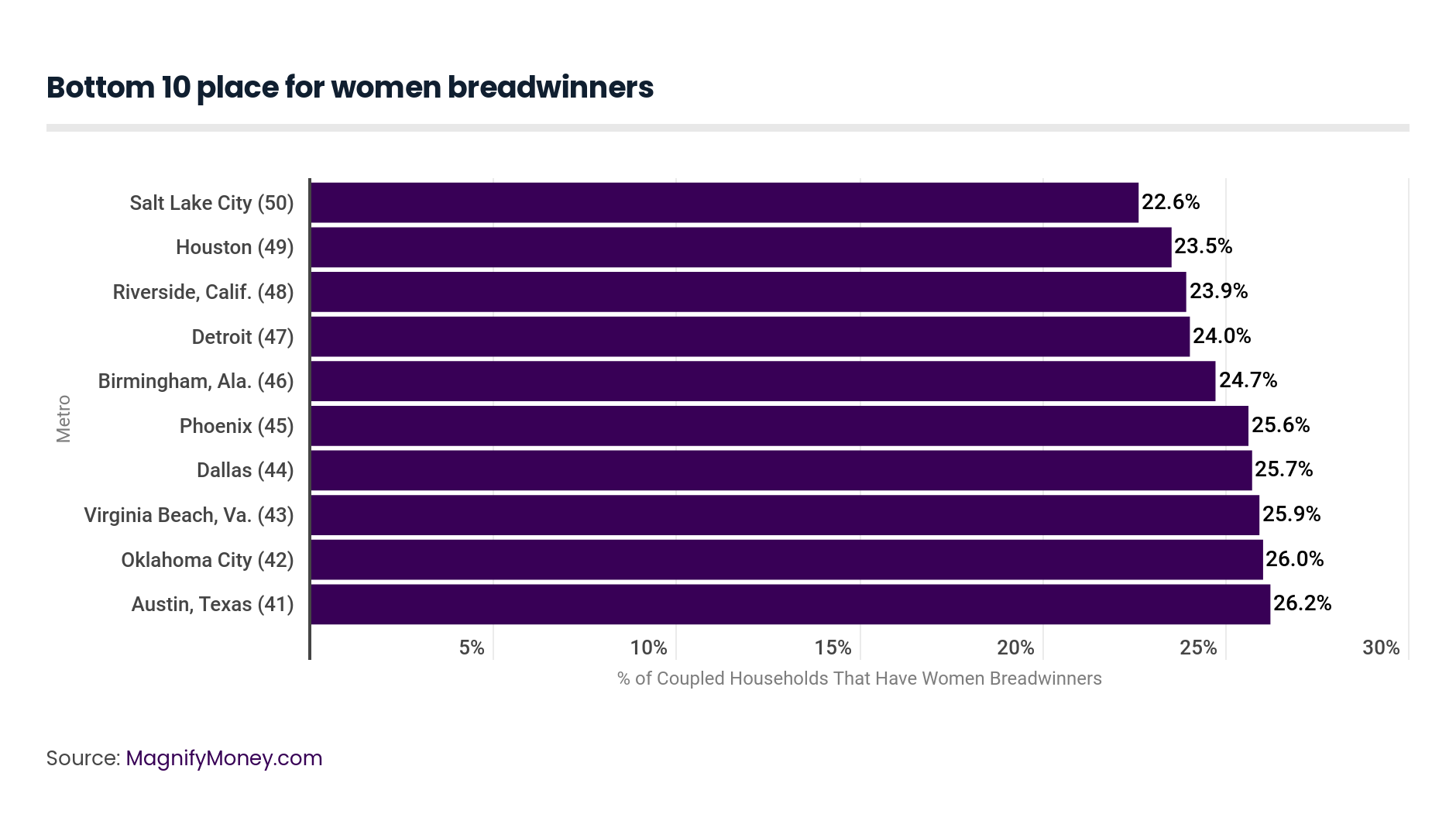

Along with the 10 cities that had the highest rates of women out-earning their partners, we also found the 10 major U.S. cities where women were the least likely to be breadwinners. In these cities, around a quarter (or fewer) of women with partners bring home higher pay than their significant other.

Most of these cities were also among the worst places for women to work, including Detroit and Oklahoma City. Still, low rates of female breadwinners isn’t always a sign of a city that disadvantages women, as three of these cities were among the 15 best places for working women: Austin, Texas; Phoenix; and Virginia Beach, Va.

Overall, this study is another sign of how women are often behind when it comes to pay. The gender pay gap is a big contributor to the low rate of female breadwinners, but it affects more than just women.

When a woman is paid less, this impacts her partner too. The entire household comes up short, setting back financial goals such as paying down debt, building security and savings, and managing money day-to-day.

Some women will also feel the pain of the wage gap more than others, too. Same-sex couples comprised of two female earners, for example, will be doubly hit by the setbacks of the gender pay gap. Women who are the sole breadwinners might also find that they’re having to support their family on less pay than many men in the same position. And for women who earn less than their partner, a separation or divorce can be particularly problematic for their finances.

Many of these factors are outside of U.S. women’s immediate control — but that makes it all the more important to focus on improving their finances where they can.

Here are some ways women can work to close, offset, or compensate for the gender pay gap.

Work on increasing your income. The top cities are proof that the gender pay gap doesn’t have to be universal, and many women are finding ways to close or even overcome it. Take a look at your current pay and do some research through sites such as PayScale or Glassdoor to figure out if it’s fair. If it’s not, it might be time to ask to be paid what you’re worth, either with your current employer or a new one.

You can also look out for career training and opportunities that could act as stepping stones to higher-paying positions. You can even create your own opportunities to boost your income and grow your skills with a side hustle.

Share costs fairly. There are a lot of ways for couples to manage their money together, so look into different methods and decide together on one that’s equitable. If your partner earns twice as much as you, for example, does it really make sense to split expenses 50-50? Discuss how you can work with differences in pay to ensure that both assets and expenses are equally and fairly shared.

Make savings a priority. Women in a couple must save for their own future, regardless of what they earn. It can be wise to have your own checking or savings accounts that are held in your name alone, where you can build financial security independent of your partner. It’s also wise to set up your own retirement accounts and contribute to those regularly, as well.

Manage debt wisely. Debt can be a huge source of stress for couples. On top of that, debt accrued in marriage can be considered jointly shared, making you equally responsible for its repayment even if your spouse took it out. So it’s smart to practice good budgeting habits, live within your means and avoid getting into debt. Even if you’re not married, your or your partner’s debt will still affect shared money goals and lower the debtor’s ability to contribute as equally. Work on paying debt off faster, and look into ways to lower costs such as credit card consolidation.

As of 17-May-19, LendingTree Personal Loan consumers were seeing match rates as low as 2.49% (2.49% APR) on a $20,000 loan amount for a term of three (3) years. Rates and APRs were based on a self-identified credit score of 700 or higher, zero down payment, origination fees of $0 to $100 (depending on loan amount and term selected). Terms Apply. NMLS #1136

While women with a partner are still less likely to be the breadwinners than partnered men, it doesn’t have to hold back their finances. Choose a significant other who values and equal partnership and practices sound financial management. Aim for higher-paying positions at work to try to close the gender gap. Then improve your own money skills and knowledge so you can make the most of your income.

Analysts used the U.S. Census’ American Community Survey 2017 microdata hosted on IPUMS to determine the percentage of coupled households with a female partner, where a female partner had the higher income. The analysis was limited to the 50 largest metropolitan statistical areas in the U.S.

Elyssa Kirkham

Elyssa KirkhamElyssa Kirkham is a personal finance writer whose work has been featured in TIME, CBS News, MSN Money, Business Insider, Daily Finance and more.

Read More