MagnifyMoney

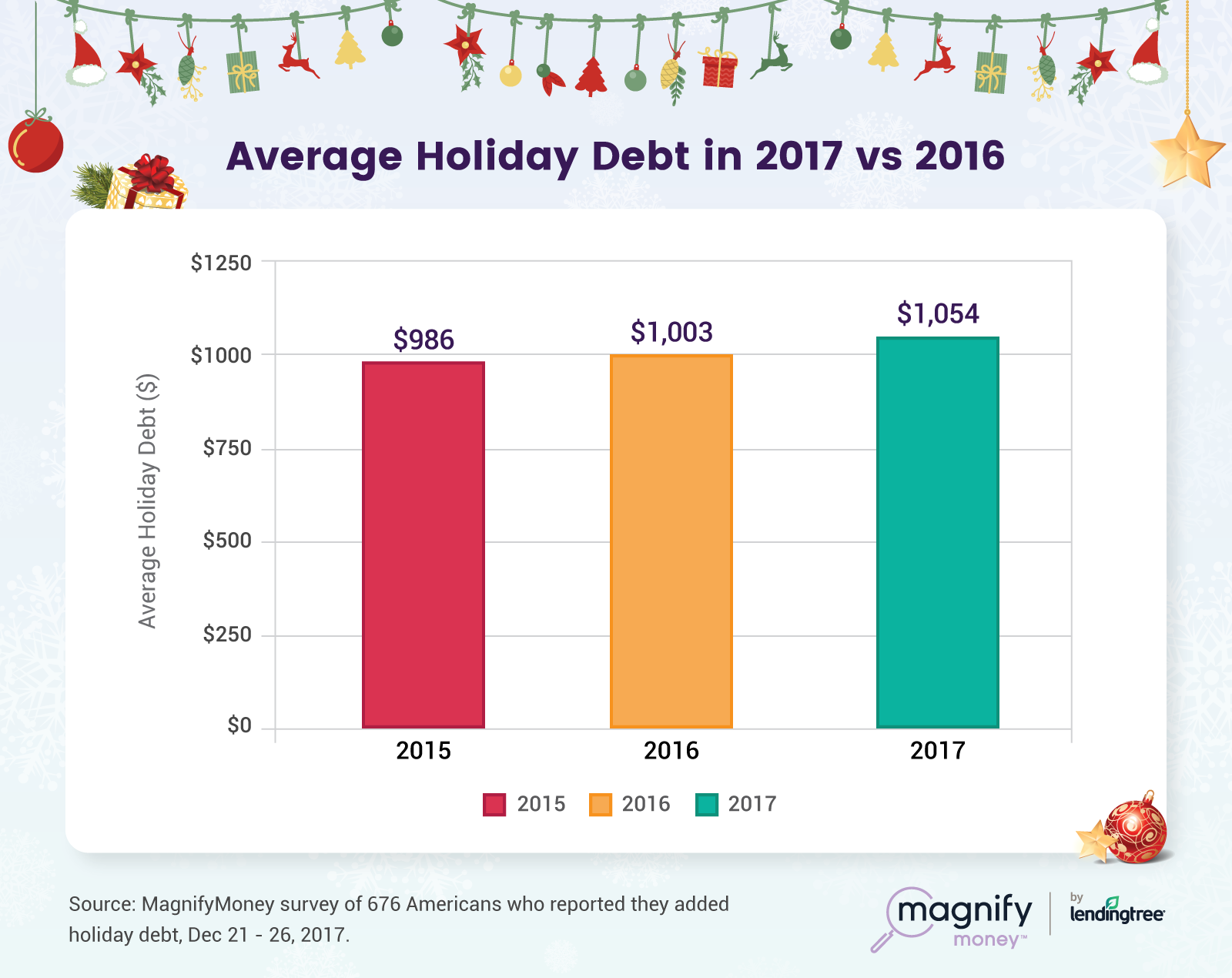

Consumers who said they went into debt over the holiday season racked up an average of $1,054 of debt, according to an annual survey conducted by MagnifyMoney. That’s not only an increase of 5% over last year, but we also found more shoppers put that debt on high-interest plastic.

As in previous years, most shoppers who took on holiday debt put their purchases on credit cards. But the percentage of consumers who pulled out the plastic for holiday gifts and other seasonal spending was significantly higher in 2017. When asked where the holiday debt came from, 68% of shoppers said that credit cards were responsible, up 8 percentage points from 2016. Store cards were the reason for 17% of shoppers, and 9% used a personal loan.

Nor were the amounts of debt accumulated trivial. Many consumers accumulated significant amounts of debt this season: 44% of shoppers racked up more than $1,000 in holiday debt, and 5% accumulated more than $5,000 in balances. Meanwhile, half of consumers admit it will take more than three months to pay off that spending.

Early indications from industry sources show that retail sales rose nearly 5% versus last year, according to a sales report by Mastercard. The MagnifyMoney survey appears to validate that finding: among shoppers surveyed who said they went into debt, the average amount spent this season exceeded 2016 spending by $51, or roughly 5%.

For most shoppers, going into debt wasn’t the plan. According to the survey, 64% of those who have holiday-related debt didn’t plan to incur it. And lack of planning, whether it’s for holiday spending or other types of debt, can lead to financial problems down the road.

Only half of those surveyed said that they expected to pay off their spending in three months or less. Of the remaining half, 29% said they’ll need five months or longer to pay off holiday debt, in most cases accruing additional interest.

An additional 10 percent of people who took on holiday debt said they would only make minimum payments. Assuming that shopper spent the average of $1,054, and paid a minimum payment of $25 each month, he or she would be paying down that balance until 2023. That is nearly as painful as the $500 in interest fees they would pay over that time, assuming an annual percentage rate (APR) of 15.9%.

Interestingly, nearly half of respondents indicated they’re paying less than a 10% APR on their balances. Although the survey didn’t ask the source of those low rates, some of these “rates” could be special financing offers from store cards from retailers – a source of financing for 17% of holiday shoppers surveyed who said they took on debt this year.

The holiday season is prime time for special in-store financing offers, but once you read the fine print, they may cost much more than they help shoppers save. Many of store cards come with deferred interest clauses, where the consumer pays no interest for a fixed period – often 6 months. If the consumer pays off those types of purchases within the period, he or she does indeed pay no interest. But after that period ends, any balance that hasn’t yet been paid in full will be charged interest retroactively, often at rates much higher than most bank-issued credit cards (APRs of 25% or greater are typical).

Although more shoppers resorted to credit cards for holiday shopping this year, fewer used loans like payday or title loans – usually the most costly form of borrowing for consumers. Only 4% of shoppers said they used payday or title loans to finance holiday shopping, down from 6% in 2016. Similarly, only 2% said they used home equity for financing. Although home equity may provide more favorable borrowing terms, there may be additional fees you’ll incur, and in the worst case, your home is the ultimate collateral on these loans.

By understanding where your finances are now, you’ll likely do a better job with managing your debt and spending in the future. For instance, just tracking your spending, whether or not it’s holiday-related spending, will help clarify which expenses might be able to be reduced or eliminated.

Finding out your what’s in your credit reports (available for free at AnnualCreditReport.com) will confirm there aren’t any unexpected surprises waiting for you should you consider refinancing with a lower-rate personal loan or zero percent balance transfer offer from a new or existing credit card offer. Other tactics, like automated payment plans and budgeting, can be found in The MagnifyMoney Debt Guide e-book.

Methodology: MagnifyMoney surveyed 676 U.S. adults who reported they added debt over the holidays via Google Consumer Surveys from December 21 – 26, 2017. Percentages may not add up to 100% due to rounding.

Average debt among shoppers who said they went into debt over the holidays

2017: $1,054

2016: $1,003

If you went into debt, did you plan to go into debt this holiday season?

Yes: 36%

No: 64%

How much debt did you take on over the holidays?

$0-999: 56%

$1,000-1,999: 26%

$2,000-2,999: 9%

$3,000-3,999: 3%

$4,000-4,999: 1%

$5,000-5,999: 4%

$6,000+: 1%

Where did your holiday debt come from?

Credit cards: 68%

Store cards: 17%

Personal loan: 9%

Payday / title loan: 4%

Home equity loan: 2%

When will you pay the debt off?

1 month: 19%

2 months: 16%

3 months: 14%

4 months: 11%

5 months+: 30%

I’m only making minimum payments: 10%

Will you try to consolidate your debt or shop around for a good balance transfer rate?

Yes: 12%

No – Don’t want to deal with another bank: 27%

No – Too many traps: 20%

No – Rate is already low: 23%

No: – Don’t know enough about it: 10%

No – Wouldn’t qualify: 8%

How stressed are you about your holiday debt?

Stressed: 29%

Not Stressed: 71%

What interest rate are you paying on your debt?

Less than 10%: 49%

10-19%: 33%

20-29%: 16%