MagnifyMoney

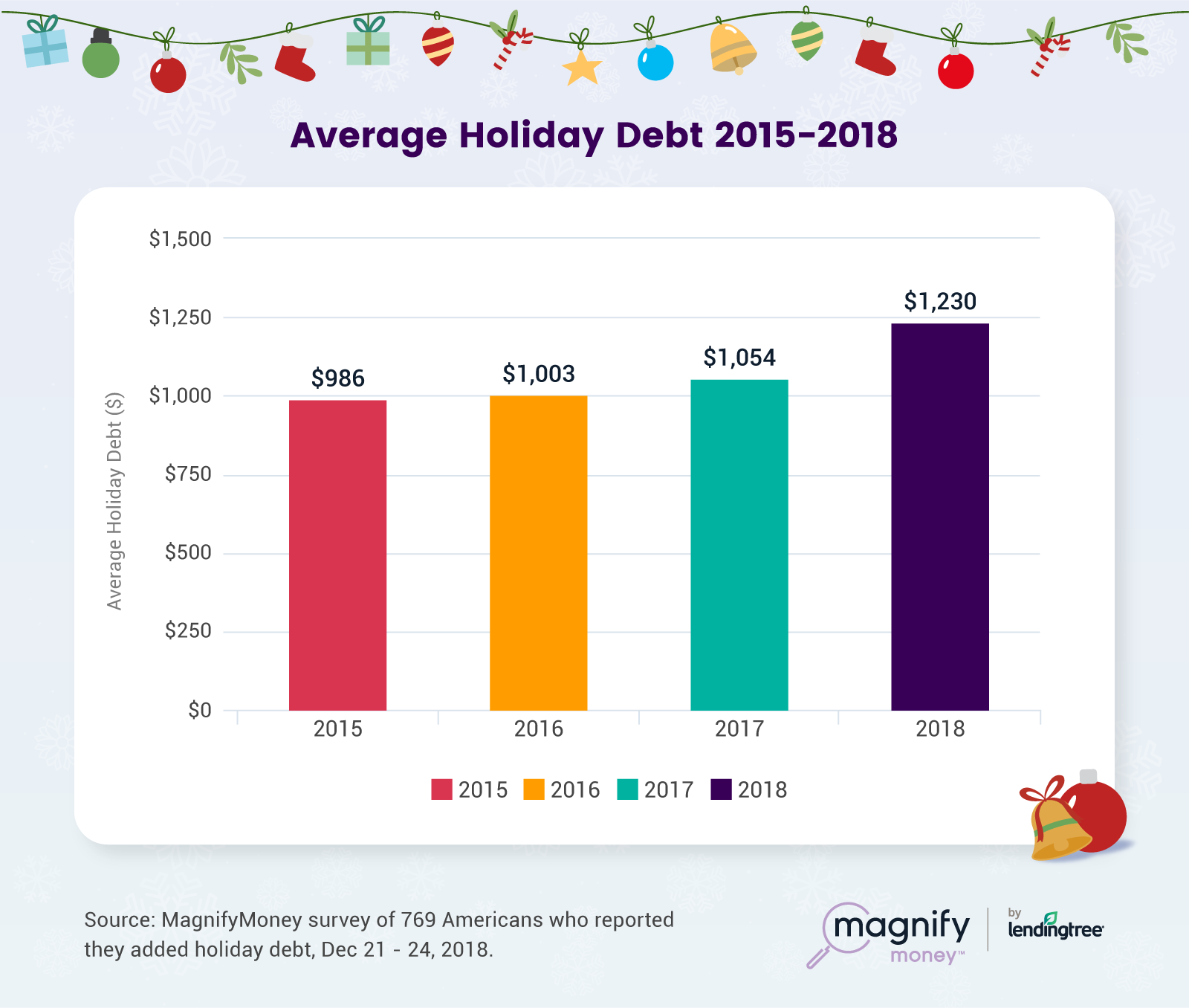

Consumers taking on holiday debt this season used more credit than last year, piling on an average $1,230, according to an annual survey conducted by MagnifyMoney. This marked an increase from $1,054 during the 2017 holiday season, and $1,003 in 2016.

And what’s more, most of those borrowing for the holidays — a full 64% — said they hadn’t expected to resort to debt for their seasonal spending.

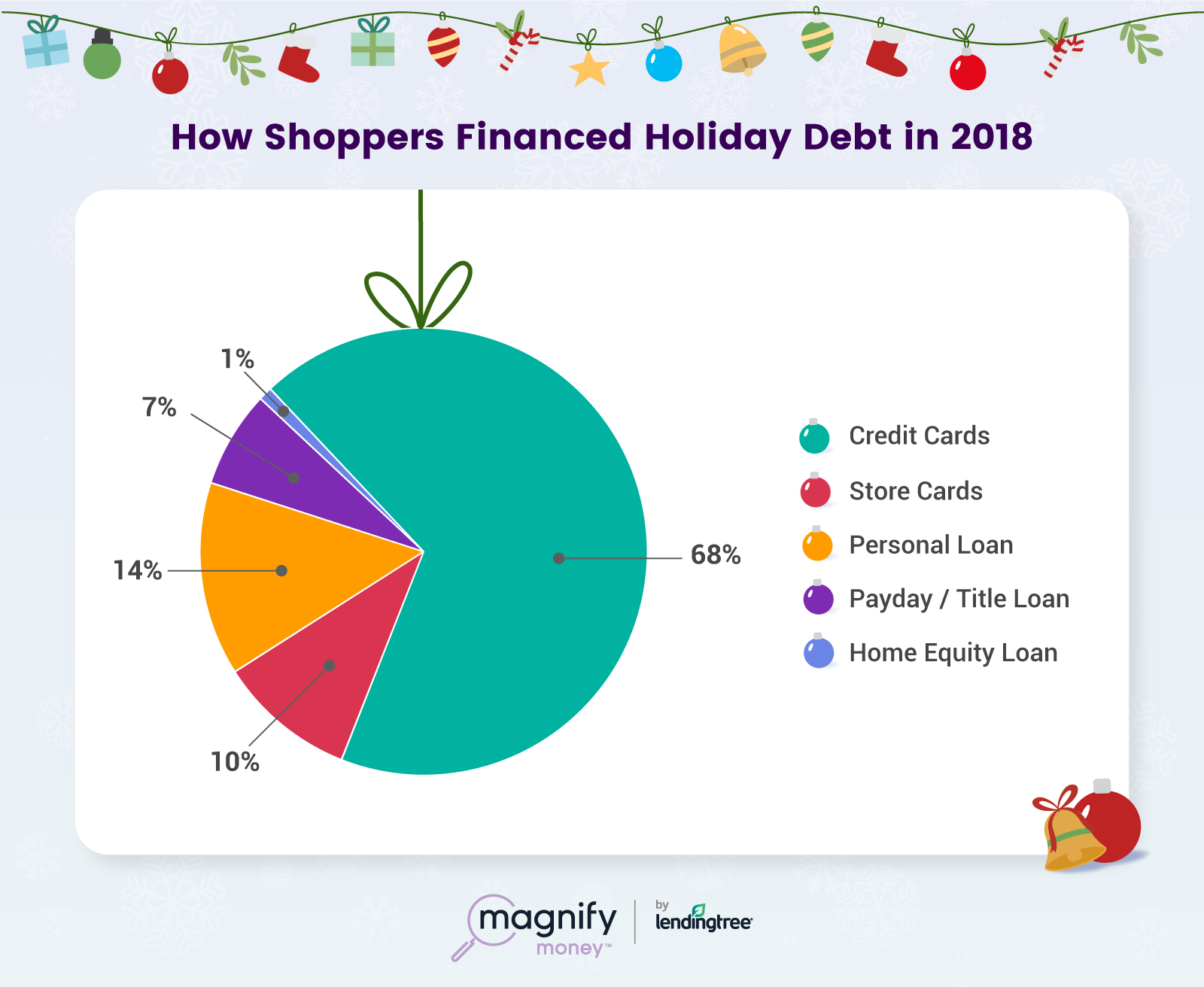

In terms of the funding details, 68% of those with holiday debt put it on credit cards, about the same as last year, the survey found.

Personal loans were the second-most common way to finance the season’s costs, with 14%. Store cards came in third, cited as a primary means of credit by 10% of those taking on holiday debt.

The breakdown comes as online shopping is expected to be “especially strong,” with a 19.1% rise over the last year, according to Mastercard’s SpendingPulse™ forecast released Dec. 26.

This is more than double what was spent in e-commerce five years ago, and compares to a 5% growth for total retail sales, excluding automotives, according to the forecast, which covered Nov. 1-Dec. 24 period.

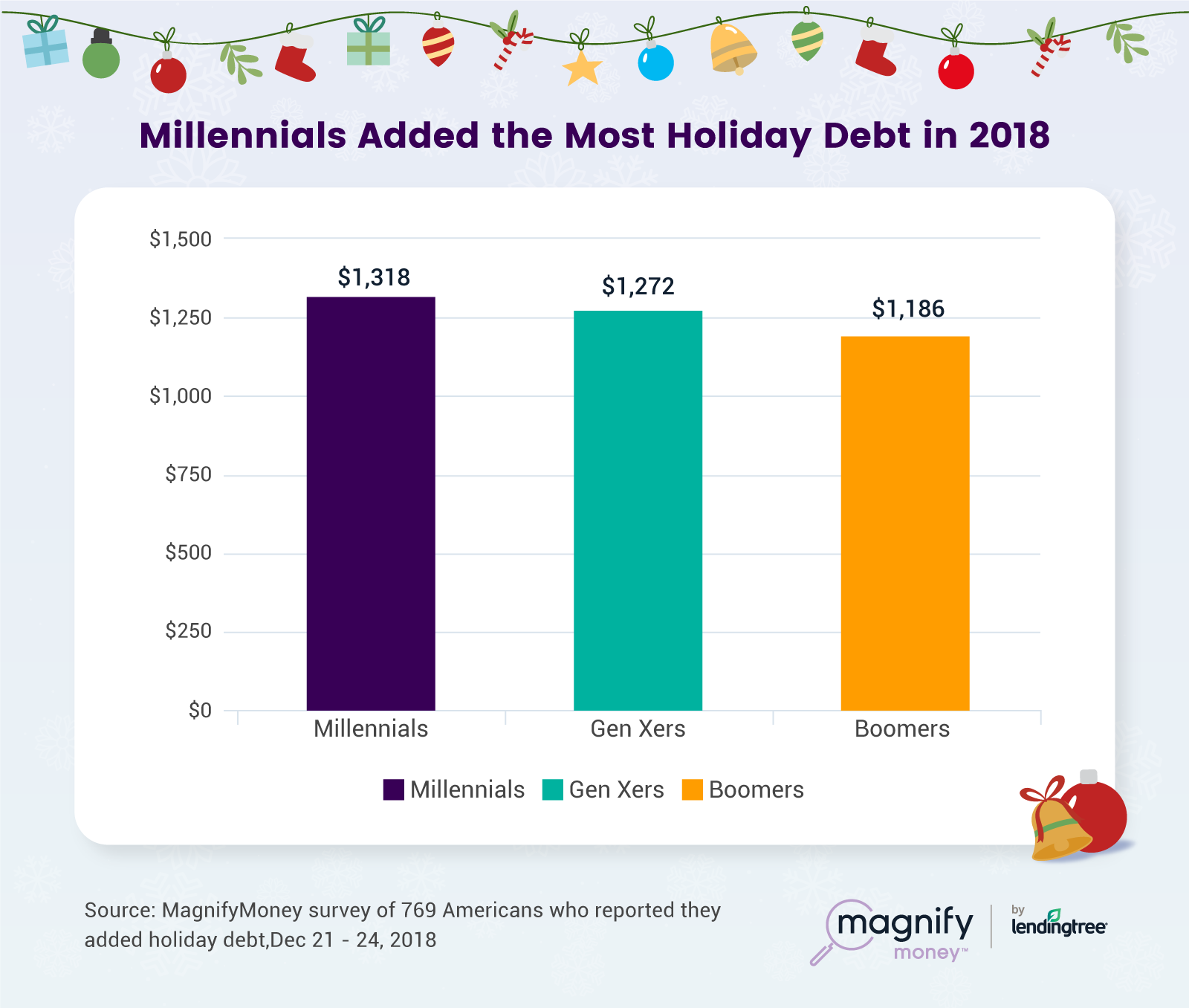

Our survey also showed that the level of holiday debt was heavier on younger consumers.

Millennials with holiday debt spent the most on credit, with an average $1,318. Gen Xers came next, at $1,272, followed by baby boomers, with an average of $1,186.

Among respondents with holiday debt, 62% reported feeling stressed about it. Some of this might be because, as mentioned earlier, a similar percentage said they hadn’t planned to fund their holidays with credit. But the lingering nature of the debt could be a factor as well.

Almost half of the holiday debtors surveyed (49%) said it would take five months or longer to pay off the season’s debt, including 22% who said they only plan to make minimum payments on that debt.

In fact, it would take more than five years to repay $1,230 in holiday debt if you make minimum payments of $30 a month at an annual percentage rate of 16.5%, which is the current national average credit card interest rate, according to recent Federal Reserve data. This would include a hefty $592 worth of interest.

On the other hand, 42% of those surveyed with holiday debt said they expect to have it paid off in three months or less.

With most holiday deficit spending done on credit cards, the potentially heavy interest costs for the 2018 holiday season might not come as much of a surprise. As we’ve reported, Americans are already paying over $100 billion in credit card interest annually, up by more than 35% over the last five years.

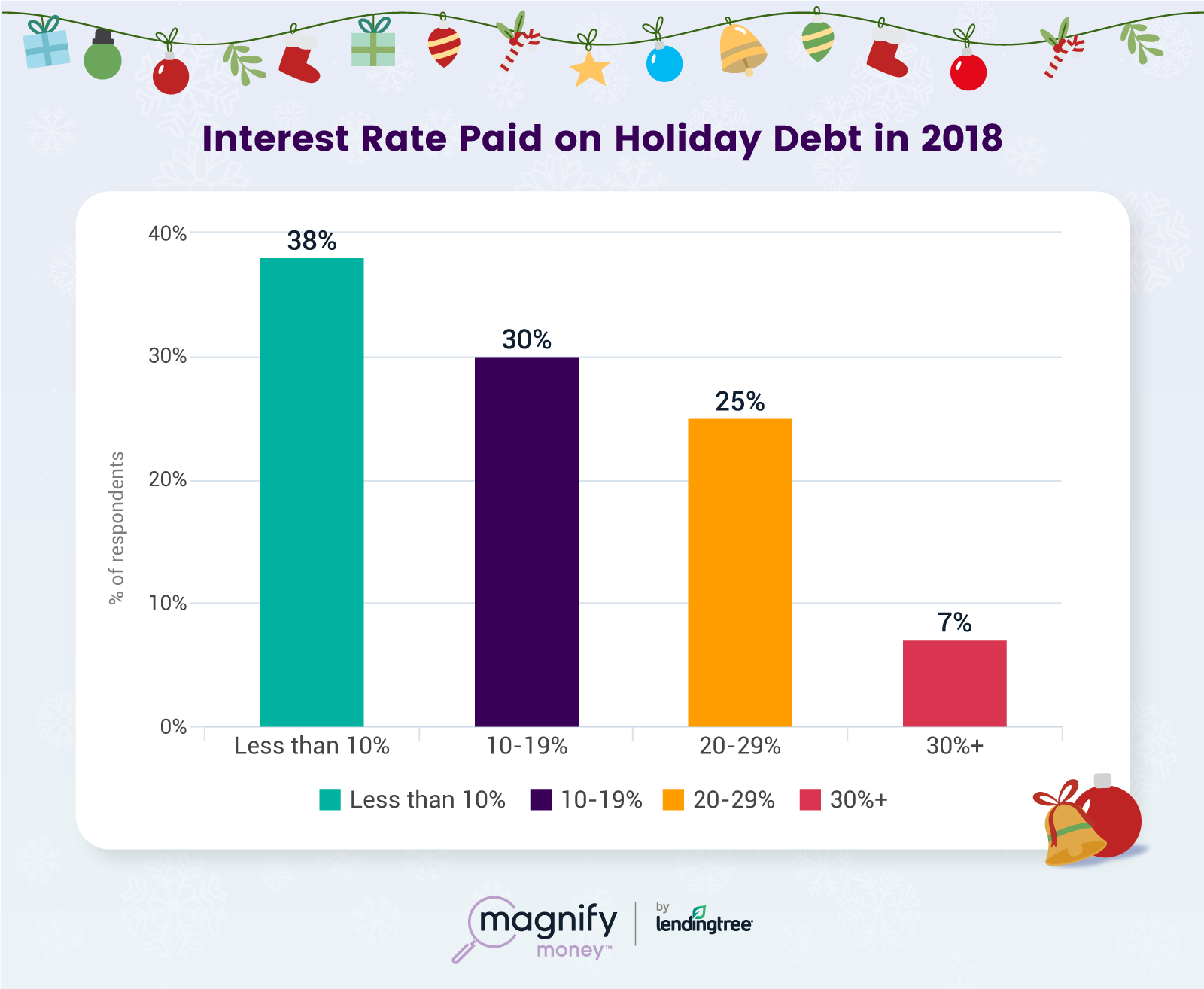

But while 16.5% might be the current average credit card APR, not everyone is paying that much. Among those taking on holiday debt, 38% reported paying 10% or less in interest. This includes those savvy consumers taking advantage of 0% APR offers, although just 27% of respondents with holiday debt said they were considering a balance transfer to lower the rate on their credit cards.

Taking measures to slash the interest on your debt — whether through 0% balance transfer cards or even paying off that debt under a consolidation loan — are generally wise moves. If you find yourself snowed under with credit card bills this holiday season, consider ways to save on interest as your repay them in the new year.

Methodology: MagnifyMoney conducted an online survey via Qualtrics from December 21-24, 2018, with 769 adults who reported they added debt over the holidays this year. Percentages may not add up to 100% due to rounding. The margin of error is +/- 4%, and the incidence rate was 35% from a sample of 2,180 adults.

Average debt among shoppers who said they went into debt over the holidays

2018: $1,230

2017: $1,054

Average debt by generation among shoppers who said they went into debt over the holidays

Millennials (age 22-37): $1,318

Gen X (age 38-53): $1,272

Boomers (age 54-72): $1,186

Did you plan to go into debt this year?

Yes: 36%

No: 64%

How much debt did you take on over the holidays?

Under $1,000: 54%

$1,000-1,999: 22%

$2,000-2,999: 13%

$3,000-3,999: 4%

$4,000-4,999: 1%

$5,000-5,999: 5%

$6,000+: 1%

Where did your holiday debt come from?

Credit cards: 68%

Personal loan: 14%

Store cards: 10%

Payday / title loan: 7%

Home equity loan: 1%

When will you pay the debt off?

1 month: 11%

2 months: 13%

3 months: 18%

4 months: 9%

5 months+: 27%

I’m only making minimum payments: 22%

Will you try to consolidate your debt or shop around for a good balance transfer rate?

Yes: 27%

No – don’t want to deal with another bank: 15%

No – too many traps: 11%

No – Rate is already low: 16%

No – Don’t know enough about it: 18%

No – Wouldn’t qualify: 14%

How stressed are you about your holiday debt?

Stressed: 62%

Not stressed: 38%

What interest rate are you paying on your debt? (percent)

Less than 10%: 38%

10-19%: 30%

20-29%: 25%

30%+: 7%