MagnifyMoney

MagnifyMoney researchers analyzed the 50 largest U.S. cities to determine where women business owners are seeing the most success. Cities were scored in four categories relating to income, business earnings, rate of incorporation and entrepreneurial parity between men and women.

The results show women on the West Coast are most poised for success, though our top cities represent a range of regions.

Income for self-employed women. We looked at both median and average business income for self-employed women in each city. In an ideal scenario, both numbers are high. However, a wide gap between the two could indicate more opportunity for potential earnings for self-employed women in a certain area.

Business earnings for self-employed women compared with wage earners. We compared income for self-employed women to earnings for women who work for wages. Self-employed women generally make less than those with earned income. A smaller difference between the two amounts could imply that women may benefit from going into business for themselves.

The rate of self-employed and incorporated women. The rankings reflect the percentage of self-employed women, as well as how many of those women have incorporated their businesses. A high rate of self-employment may suggest low barriers to entry for women entrepreneurs. A large amount of incorporated businesses could indicate women are seeing enough success to consider legal and tax implications of business ownership.

Parity of business ownership between women and men. We analyzed the percentage of women among all self-employed people and owners of incorporated businesses in each city. Places with higher percentages could have a more even playing field for women.

Women in our top places earn decent average income from their own businesses and make up nearly half of self-employed workers in their respective locations.

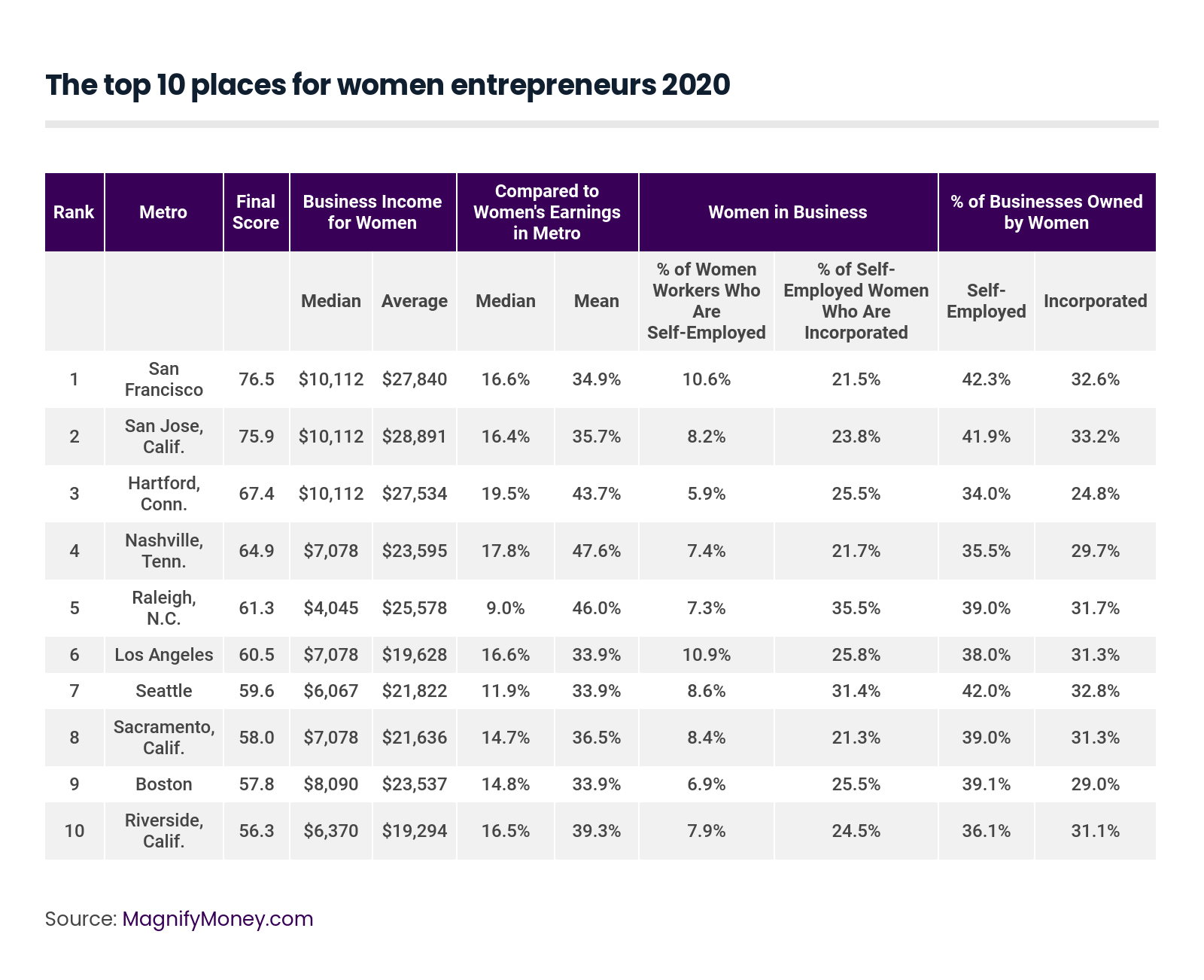

San Francisco took the top spot with a final score of 76.5 — a few points lower than 2018, but still high enough to hold on to first place. Nearly 11% of working women are self-employed, and 21.5% own an incorporated business. Business income for women is $27,840, on average, about 35% of what women earn when working for wages. Of all self-employed people in the city, women make up 42.3%, and they comprise 32.6% of all owners of incorporated companies.

Women’s entrepreneurship groups throughout San Francisco host regular networking events and panel discussions. The local government is also supportive of women-owned businesses. For instance, the San Francisco Office of Economic and Workforce Development provides grants through the San Francisco Women’s Entrepreneurship Fund.

San Jose moved up from its previous No. 3 ranking receiving a final score of 75.9 this year. Women business owners earn an average of $28,891 – more than women in San Francisco – and that income is 35.7% of women’s income from earned wages. Slightly more than 8% of women in the city are self-employed, and 23.8% run an incorporated business. Those women comprise nearly 42% of all self-employed workers in San Jose and 33.2% of owners of incorporated establishments.

Women business owners in San Jose can turn to numerous local groups for support and resources, such as the local eWomenNetwork chapter and the Women’s Networking Alliance. The AnewAmerica Women’s Business Center, which also operates in Oakland, also provides training and counseling to help women grow their businesses.

Hartford jumped from No. 18 to round out our top three best places for women entrepreneurs with a score of 67.4. On average, women business owners earn $27,534, which is 43.7% of women’s earned wages, a higher percentage than the first two cities. Although just 5.9% of women are self employed, 25.5% own an incorporated business. Of all self-employed people in the city, 34% are women. Additionally, women account for 24.8% of incorporated business owners in Hartford.

Hartford saw an improvement in business earnings for women entrepreneurs in this year’s ranking, which contributed to its rise on our list. Women business owners can find support from Greater Hartford’s chapter of eWomenNetwork, Innovation Destination: Hartford and the Women’s Business Center at the University of Hartford.

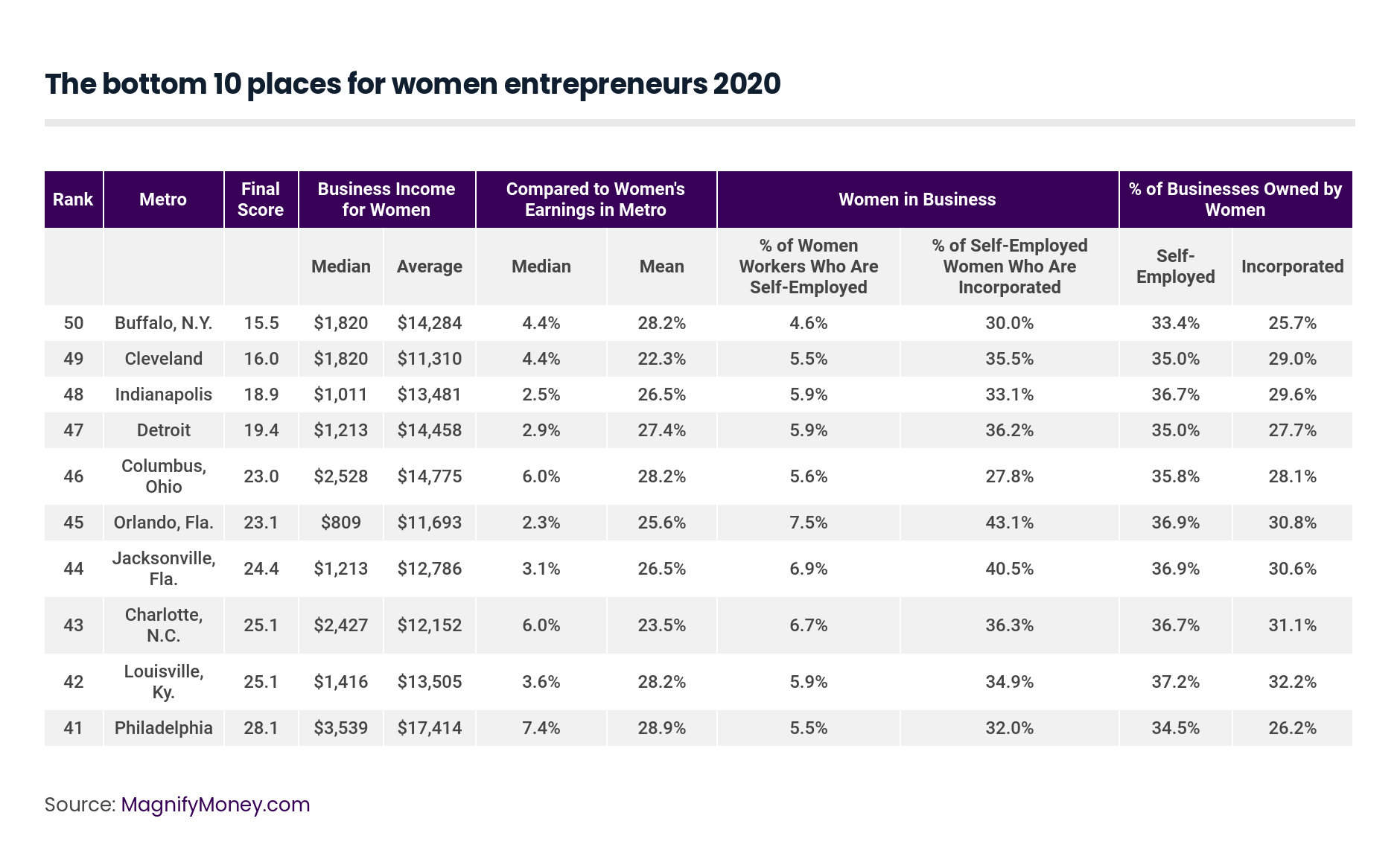

The cities ranking lowest in our study generally have lower business income for women entrepreneurs than the top cities. Orlando, at No. 45, has a median business income of $809, meaning at least half of self-employed women earn that amount or less.

Fewer women in these cities have ventured into business ownership as well. With a smaller number of women entrepreneurs in the area, it may be harder for business owners to establish professional networks or find mentorship among other women — this kind of support is often essential to emerging startups.

However, the data could indicate the entrepreneurial climate is poor for self-employed people in general, not solely women. Although it may be possible to operate a successful company in these cities, women may want to proceed with caution before starting a new venture here.

Living in one of the best cities won’t guarantee success any more than starting in one of the worst cities will ensure failure. Wherever they live, women entrepreneurs must chart their own path to self-employment. If you have a financial advisor they may be able to provide the investment advice necessary for starting a business.

For women ready to take their first steps toward entrepreneurship, these tips could help them get further faster.

Each of the 50 largest metropolitan statistical areas (“MSAs”) was scaled against one another, so that the most positive result for each factor was 100 and the most negative was 0 on the following eight factors from the U.S. Census Bureau’s American Community Survey for 2017 available through FactFinder or calculated from microdata housed in IPUMS USA. The results for each factor were then weighted according to the notation below, and the sum was divided by eight (rounded to one decimal point), for a highest possible score of 100 and a lowest possible score of 0.

Melissa Wylie

Melissa WylieMelissa Wylie is a Senior Writer covering small business financing for LendingTree.com, MagnifyMoney and ValuePenguin. Melissa helps entrepreneurs learn where to find funding and how to apply.

Read More