MagnifyMoney

A warming planet can really burn consumers…financially, at least. Climate change has cost U.S. taxpayers $350 billion over the past decade, according to one report from the Government Accountability Office, and that number is expected to swell to $35 billion per year by 2050.

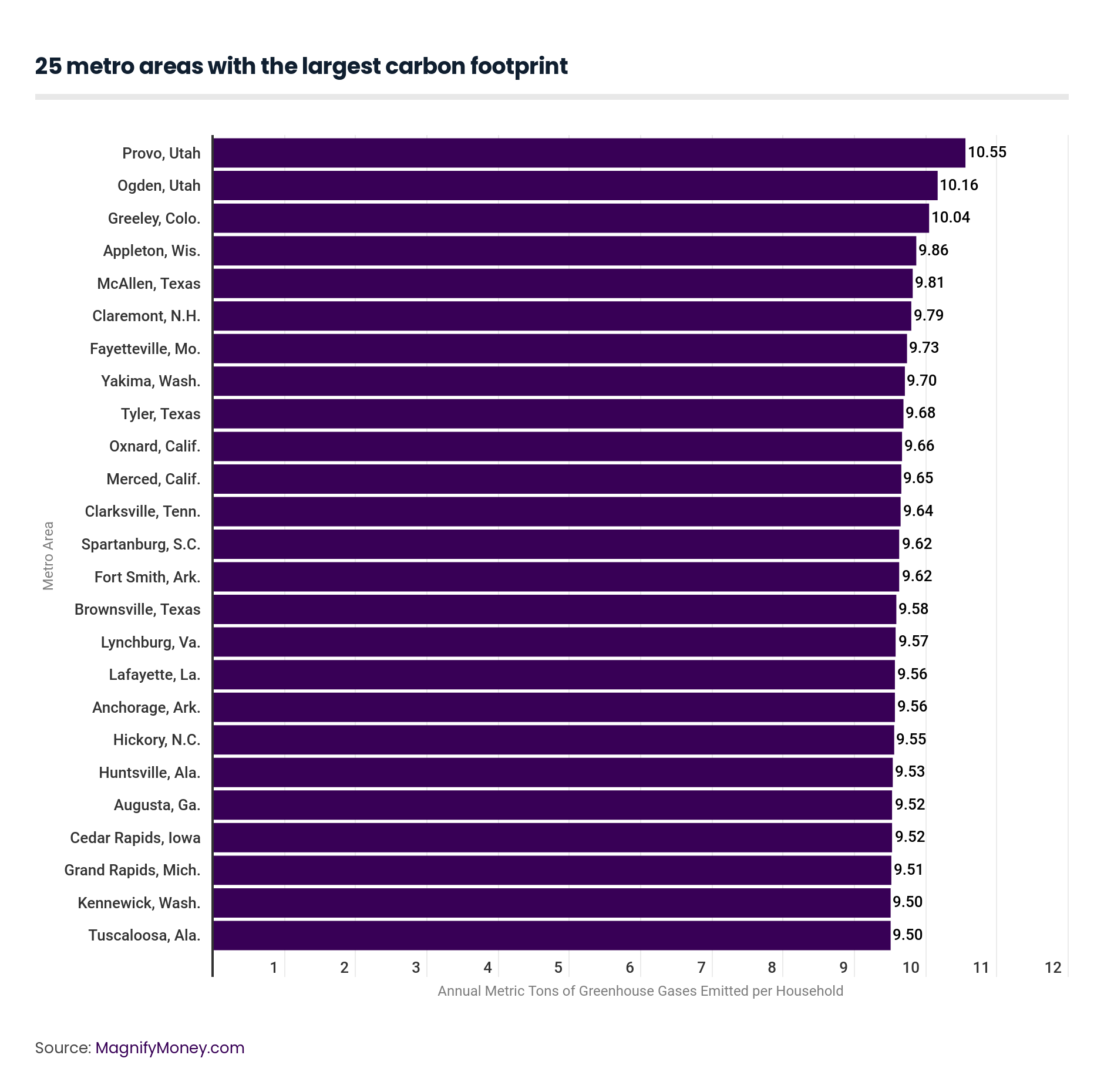

So which households are to blame? We have found that the carbon footprints of households in different cities varies widely, with households in the West spewing more carbon emissions than ones in urban, denser areas.

For this study, we’ve defined carbon footprint as the combined total annual amount of carbon dioxide produced to support the lives of each member of a household. In other words, every time you drive your car, buy groceries or heat your home, you’re adding to your household’s carbon footprint.

The study analyzes the largest 200 metros in the U.S. by population, and measures the annual average annual metric tons of CO2 emitted, per household.

Take New York City, with a population of nearly 14 million. It’s consistently ranked as one of the biggest emitters of greenhouse gases among U.S. cities, but this study found it has the smallest carbon footprint on an emissions per household basis.

Our study revealed that cities in the West have the largest carbon footprints. The top five cities with the highest average CO2 emissions per household are:

Not surprisingly, we found that cities with larger carbon footprints tended to have more cars per household. Transportation is a major factor when calculating a household’s carbon footprint—one study even found that housing and transportation are responsible for more than half of all U.S. household carbon emissions.

Households in Provo which have the biggest average household carbon footprint in our study, own an average of 2.1 cars and travel approximately 25,000 miles annually by car, while only 2% of commuters take public transit. Ogden, with the second-largest carbon footprint, touted similar statistics: Households own an average 2.04 cars and travel approximately 24,000 miles in them annually, while only 2% of commuters use public transit.

In general, dense, urban cities have the smallest average carbon footprints. We found that the top five cities with the lowest average CO2 footprints per household are:

One factor that is likely responsible for cities with relatively small carbon footprints is the widespread use of public transit. Our study found that households in New York City have 1.27 cars and travel 13,000 miles annually (compared to Provo’s household average of 2.1 cars and 25,000 miles of travel). Meanwhile, an impressive 31% of New York City commuters take public transit (compared to Provo’s 2%). The average San Francisco household has 1.66 cars and travels 17,000 miles annually, while only 15% of commuters take public transit.

Another reason for the smaller carbon footprint in big cities can be chalked up to urban density. New York City has the highest residential density score, likely due to the low number of single-family, detached homes in the city. We found that 37% of New York City households were single-family, detached homes, while that number was 67% in Provo and 75% in Ogden. Buildings with multiple apartment units have been known to use significantly less energy than single-family homes.

Going green isn’t just good for Mother Earth. It can actually save you some green, too. Residents in the cities with the largest carbon footprints spent significantly more money on annual transportation costs than those in cities with the smallest carbon footprints. Residents in Provo, for example, spend nearly $16,000 annually on transportation costs, according to our study. In contrast, New Yorkers spend around $10,000 annually on transportation.

Indeed, making the switch from commuting by car to public transit can result in substantial savings. A household can save $10,000 by taking public transit and living with one less car, according to the American Public Transportation Association. It’s also beneficial for the planet; the organization claims that if communities invest in public transit systems, they can cut the country’s carbon emissions by 37 million metric tons annually.

An environmentally cleaner commute isn’t the only way going green can save you money. Cutting down on the energy you use in your home can help, too. Assess how your home is using (and wasting) energy. Sealing uncontrolled air leaks, for example, can save you 10% to 20% annually on your heating and cooling bills, according to the Department of Energy, while replacing your five most-used light fixtures with bulbs that have earned ENERGY STAR status can save you 9% annually on your electric bill.

| Action | Potential savings (as a percentage of utility bills) | Average annual savings in $ (based on EIA average end-use expenditures*; actual savings will vary) |

|---|---|---|

| Sealing uncontrolled air leaks | 10%-20% on annual heating and cooling bills | $100-$274 |

| Replacing your lightbulbs with ENERGY star ones | 9% on electricity bill annually | 75 |

| Lowering your water heating temp | Save 4%-22% annually on your water heating bill | $12-$60 |

| Use sleep mode | Up to 4% of annual electric bill | 30 |

| Fix leaky faucets | N/A | 35 |

Source: energy.gov

Other simple steps you can take to reel in your energy bill include regularly examining your HVAC system air filter, reducing the temperature of your water heater to 120 degrees and shutting off lights when you are not using them.

There are easy ways you can cut back on the amount of money you spend on energy, while also shrinking your carbon footprint. For transportation, you can:

At home, you can:

Another way you can have a positive impact on the earth — while also doing yourself a favor financially — is taking a close look at socially-responsible investing.

MagnifyMoney analyzed 2017 data from the Center for Neighborhood Technology Housing and Transportation Index.

Sarah Berger

Sarah BergerSarah Berger is a former writer at LendingTree, where she covered personal finance, specifically focusing on challenges and opportunities facing millennials. Before joining LendingTree, she was a writer for CNBC and Bankrate.

Read More