MagnifyMoney

The 2018 household income growth numbers released by the United States Census Bureau revealed that the median earnings of all workers grew over 3% last year. Sounds like a win, right? But the research also revealed that the 2018 median earnings of men was $55,291. Women, on the other hand, only made a median of $45,097.

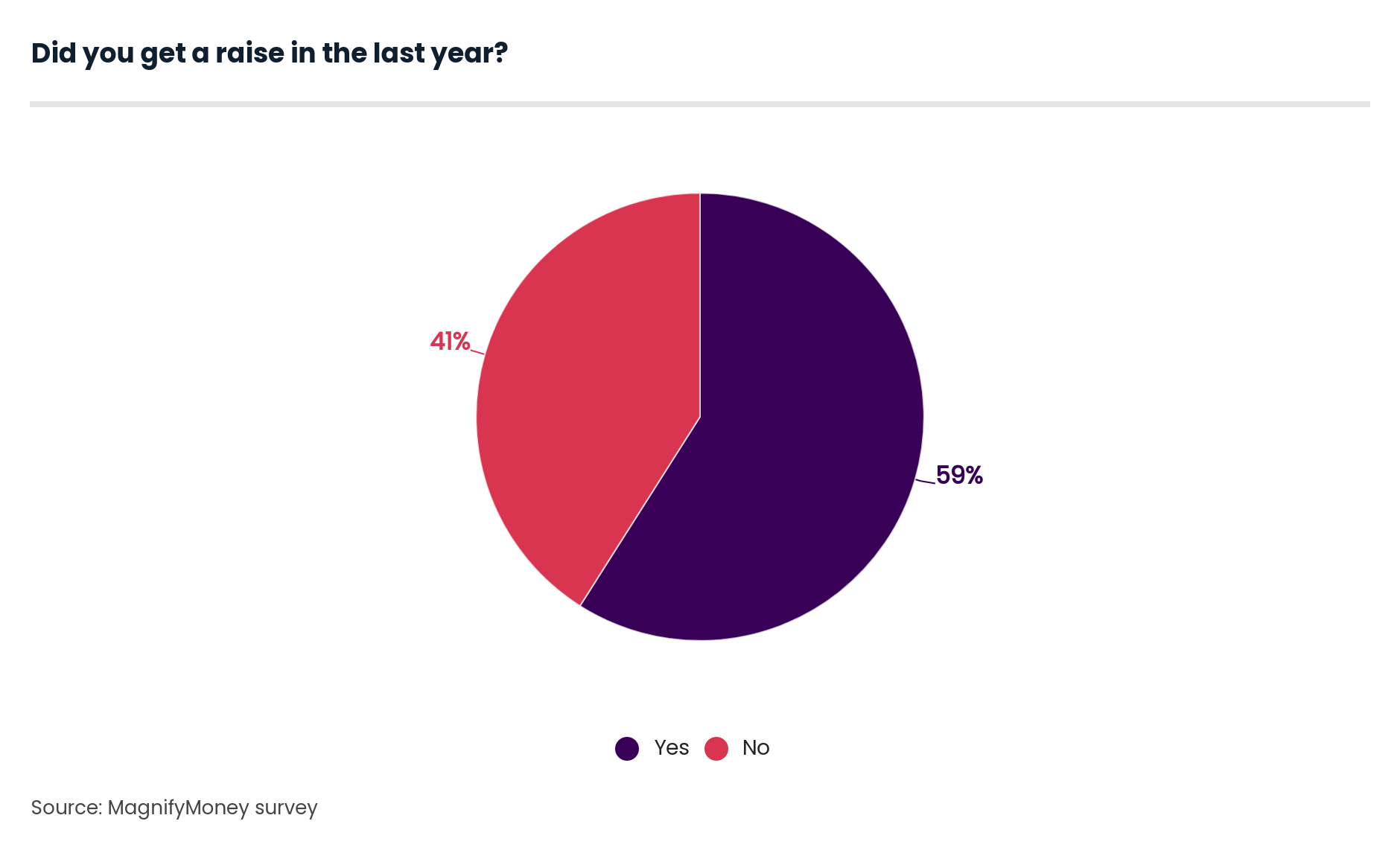

MagnifyMoney by LendingTree wanted to investigate this pay disparity further. They conducted a survey of Americans who work at least 30 hours a week about their pay raises, promotions and career moves.

You know the old saying: Men are from Mars, women are from Venus. We know it’s not true, so why are women and men being paid like they live on different planets? In the past year, 12% more men reported receiving pay increases and promotions than women. Even more disappointing news: 17% more men than women picked up a promotion with their raise.

These figures strongly suggest that women had fewer opportunities for financial and career growth than men in the last year. These occurrences have a ripple effect. Men were 21% more likely than women to increase their retirement savings after they got a pay raise. It makes you wonder whether men are receiving larger pay raises than their female counterparts, considering women have been found to save a higher percentage of their money than men.

This difference in retirement saving contributes to a worrying trend. A 2018 study by Prudential found that on average, women save 43% less for retirement than men. And almost half of the women surveyed admitted to having no retirement savings at all.

Gender may not be the only divide in the workplace. Millennials get a lot of flak, but they’re moving up in the workplace. Millennials reported earning more raises last year than Gen Xers and baby boomers.

While Millennials are more likely to be in the growth stage of their career, it’s also worth noting that in 2016, Millennials became the largest generation in the workforce. Millennials were also the most likely of any generation to report that their raise came with a promotion. Not bad for the generation everyone likes to laugh at for being “lazy.” To top it off, they were also the generation most likely to increase their retirement savings after receiving a raise.

It’s fair to assume that the life and work experiences of each individual surveyed mold their view of the world around them. Because the women surveyed reported receiving fewer raises than men, it’s clear why they would be more pessimistic about their odds of receiving future raises.

While 47% of working Americans believe they’ll receive a raise next year, more of those Americans are men than women. Twenty-one percent of women doubt their pay will increase within the next 12 months, whereas only 8% of men feel that way.

Confidence seems to come easier to those with higher incomes. The more the survey respondents made in wages, the more likely they were to think they would be getting a pay raise in the next year. In their defense, the group with the highest income did in fact receive the most pay raises in the past year.

When it comes time to ask for a raise, prepare yourself by following these steps. Coming to your boss with evidence regarding why you deserve a raise and how you will increase your contributions to the company will help you work toward your professional and financial goals.

Even though you think your boss has a pretty good idea of your accomplishments, they don’t know them as well as you do. A successful request for a raise can take lots of prep work. Keeping track of your accomplishments, tasks and the changes in your role throughout the year will help you remember the triumphs you’re likely to forget a few months later.

Did a thrilled client sing your praises in an email? Flag it. Did the CEO comment on how impressed he was with your presentation? Write down his feedback. If you helped make your team more productive by introducing a new software, saved your department money or increased sales, keep notes of those occurrences somewhere you can easily reference them.

When the time comes to ask for a raise, you’ll have plenty of solid evidence at your fingertips as to why you deserve it. And remember, the more cold hard proof you have of your success (like web analytics or sales growth), the better.

Your boss shouldn’t feel blindsided when you ask for a raise. It’s important to give them notice that you want to speak to them about something important. Ask to schedule a meeting with your manager. Generally, they won’t be able to give you a firm yes or no during this meeting — that’s okay, they also have a boss to report to.

Make sure you set a meeting to follow up on your conversation. This holds your manager responsible for following through and tempers your expectations so you aren’t on pins and needles until you get an answer.

You won’t walk away from every request for a raise successfully, that’s just a fact of life. But it’s important to remember that getting a no now doesn’t mean no forever.

Ask your manager to elaborate on why they said no and how you can work towards a goal of a raise. Maybe there is an area of your performance you really do need to improve upon. Or perhaps your company doesn’t have the money for a raise in their budget. Agree on a time to circle back to this conversation later in the year, and in the meantime, take your manager’s feedback to heart. If they don’t give you a clear path for working toward a raise, it may be time to move on.

MagnifyMoney by LendingTree commissioned Qualtrics to conduct an online survey of 543 Americans who work at least 30 hours per week. The survey was fielded September 5-9, 2019.

Jacqueline DeMarco

Jacqueline DeMarcoJacqueline DeMarco is a freelance writer who is particularly passionate about finance. She began her career in the retirement industry. Today, she works with more than a dozen financial brands to create entertaining and educational money content.

Read More