MagnifyMoney

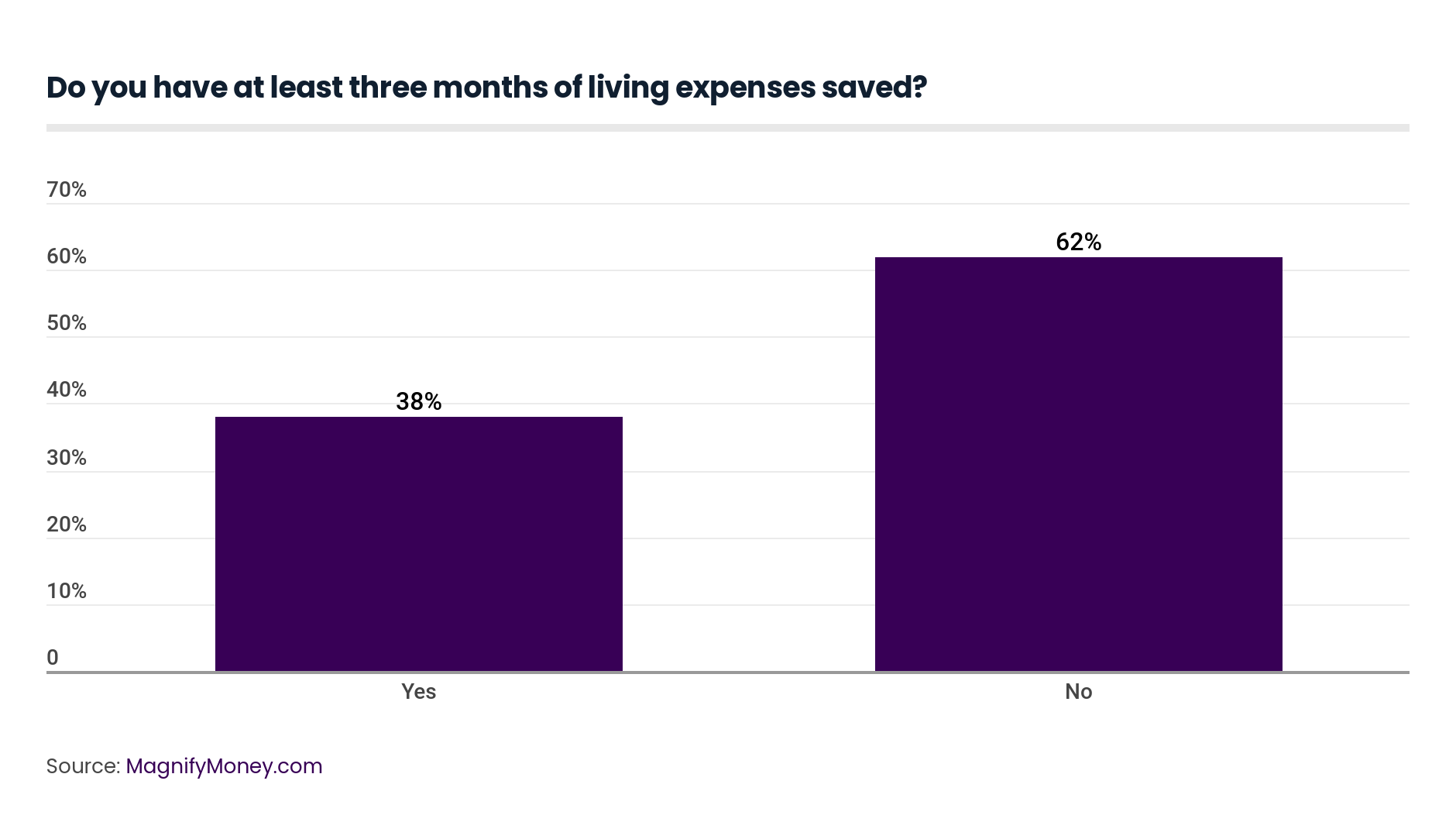

Many Americans are living life on the edge — financially, at least. A new survey from MagnifyMoney revealed that a staggering number of people live paycheck to paycheck — and that just one missed paycheck would cause bills to pile up. According to our survey of over 1,000 Americans, 62% don’t have the recommended three months of living expenses saved up.

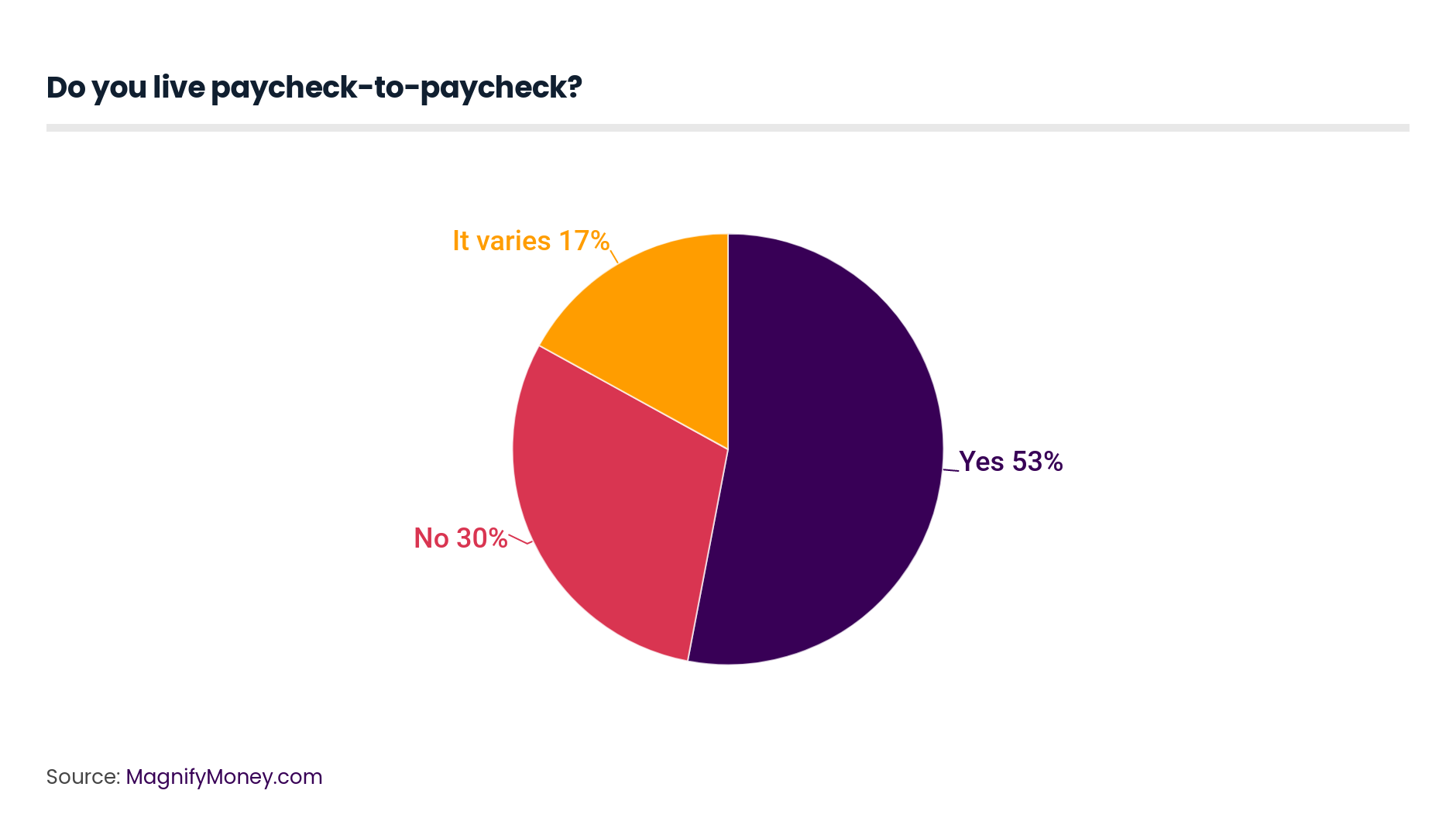

Overall, our survey found that a whopping 53% of respondents are living paycheck-to-paycheck, meaning they don’t have money left over after all their expenses are paid for. Interestingly, there were people in every generation and across every income level that said they live paycheck-to-paycheck, proving that even older and wealthier respondents skate on thin ice, financially.

In fact, there weren’t any significant differences in how many people live paycheck-to paycheck per generation: 58% of millennial respondents live paycheck-to-paycheck, as do 59% of Gen Xers and 47% of baby boomers. Nearly 55% of female respondents saying they live paycheck-to-paycheck and 51% of male respondents.

Understandably, though, the number of people living paycheck-to-paycheck varied among different income levels, with poorer households more likely to cut it close financially. Still, a surprisingly significant number of wealthy households have little financial wiggle room, too. Our survey found 28% of people who make at least six-figures have no money left over after paying for their expenses. That’s compared to 41% of households who make between $75,000 to $100,000; 47% who make between $50,000 to $75,000; 55% who make between $35,000 to $50,000; 66% who make between $25,000 and $35,000; and 67% of households who make less than $25,000.

Experts often recommend that you have enough in your savings to survive for three to six months without income, which equates to 12 to 24 weeks of living expenses. However, our survey found that most respondents only have enough saved to survive much, much less than that.

Our survey found that on average, respondents could live for 10 weeks (a little over two months) without getting paid again after receiving their last paycheck. That number varied vastly among male and female respondents, though, with the men surveyed saying on average they could get by for 11 weeks without getting paid again, compared to women’s average of just 8 weeks. One potential reason for this discrepancy could be the gender wage gap, in which women make only 82 cents for every dollar made by a man — less money earned means less money to save.

| Overall Average | Men | Women | Millennials | Gen Xers | Baby Boomers |

|---|---|---|---|---|---|

| 10 weeks | 11 weeks | 8 weeks | 7 weeks | 8 weeks | 14 weeks |

Source: MagnifyMoney.com

By generation, there was a big difference in the number of weeks people said they’d be able to go without receiving a paycheck. On average, millennials said they could survive only 7 weeks without a paycheck and Gen Xers only 8 weeks. That’s much less than baby boomers, who said they could live for 14 weeks without pay.

Not surprisingly, there were also big differences among income levels when looking at how long a person could go without pay. Households making over $100,000 said they could survive 23 weeks, those making between $75,000 and $100,000 said 11 weeks and households earning between $50,000 and $75,000 also said 11 weeks. Meanwhile, households making between $35,000 and $50,000 said only 6 weeks, $25,000 to $35,000 households said just 4 weeks and those making less than $25,000 said 6 weeks.

Another jarring discovery from our survey was that most people don’t have enough money in savings to cover three months of living expenses — which is often the bare minimum recommended as an emergency fund.

Overall, a whopping 62% of people said they do not have at least three months of living expenses saved up. The demographics that were most likely to say that they do not have at least three months stashed away include female respondents (67%), millennials (69%) and households making less than $25,000 (79%).

Additionally, overall, our survey found that 70% of people would not be able to pay all of their bills if they missed a paycheck. Even more bleak is that nearly half (48%) of millennials wouldn’t be able to pay rent or their mortgage if they missed a paycheck.

While our survey found that most respondents are struggling with saving, most financial experts recommend saving between three to six months of living expenses in a liquid emergency fund, such as a high-yield savings account. This should be enough to allow you to pay your bills and live comfortably if you lose your job or get hit with a big, unexpected expense, like a medical bill.

However, three to six months is just a guideline, and shouldn’t be viewed as one-size-fits-all. If you’re single with a steady job, three months of savings should be sufficient, while people with a spouse and children to support should aim for six months. Those that are self-employed, though, should play it safe and shoot to save at least nine months of living expenses in their emergency fund.

For our survey, MagnifyMoney commissioned Qualtrics to conduct an online survey of 1,007 Americans, with the sample base proportioned to represent the overall population. The survey was fielded October 25-29, 2019.

For our survey, we defined generations as: millennials are ages 23-38, Gen Xers are ages 39-53, and baby boomers are ages 54-73. Members of Generation Z (ages 18-22) and the Silent Generation (ages 74 and older) were also surveyed, and their responses are included within the total percentages among all respondents. However, their responses are excluded from the charts and age breakdowns due to the smaller population size among our survey sample.

Sarah Berger

Sarah BergerSarah Berger is a former writer at LendingTree, where she covered personal finance, specifically focusing on challenges and opportunities facing millennials. Before joining LendingTree, she was a writer for CNBC and Bankrate.

Read More