MagnifyMoney

As the coronavirus (COVID-19) pandemic brings the world to a screeching halt, one of its many detrimental effects is its impact on the stock market. With businesses shuttering, unemployment spiking and economic fears rising, the stock market has been hit hard, with multiple indexes plunging to new, multi-year lows in March.

Such a significant decline has taken a toll on individual investors, too. According to a new survey of over 1,000 respondents by MagnifyMoney, 38% of investors fear they’ll lose all of their retirement savings due to the economic turmoil caused by the pandemic. Already, the coronavirus outbreak has caused investors to lose money and alter their investing behavior, our survey found.

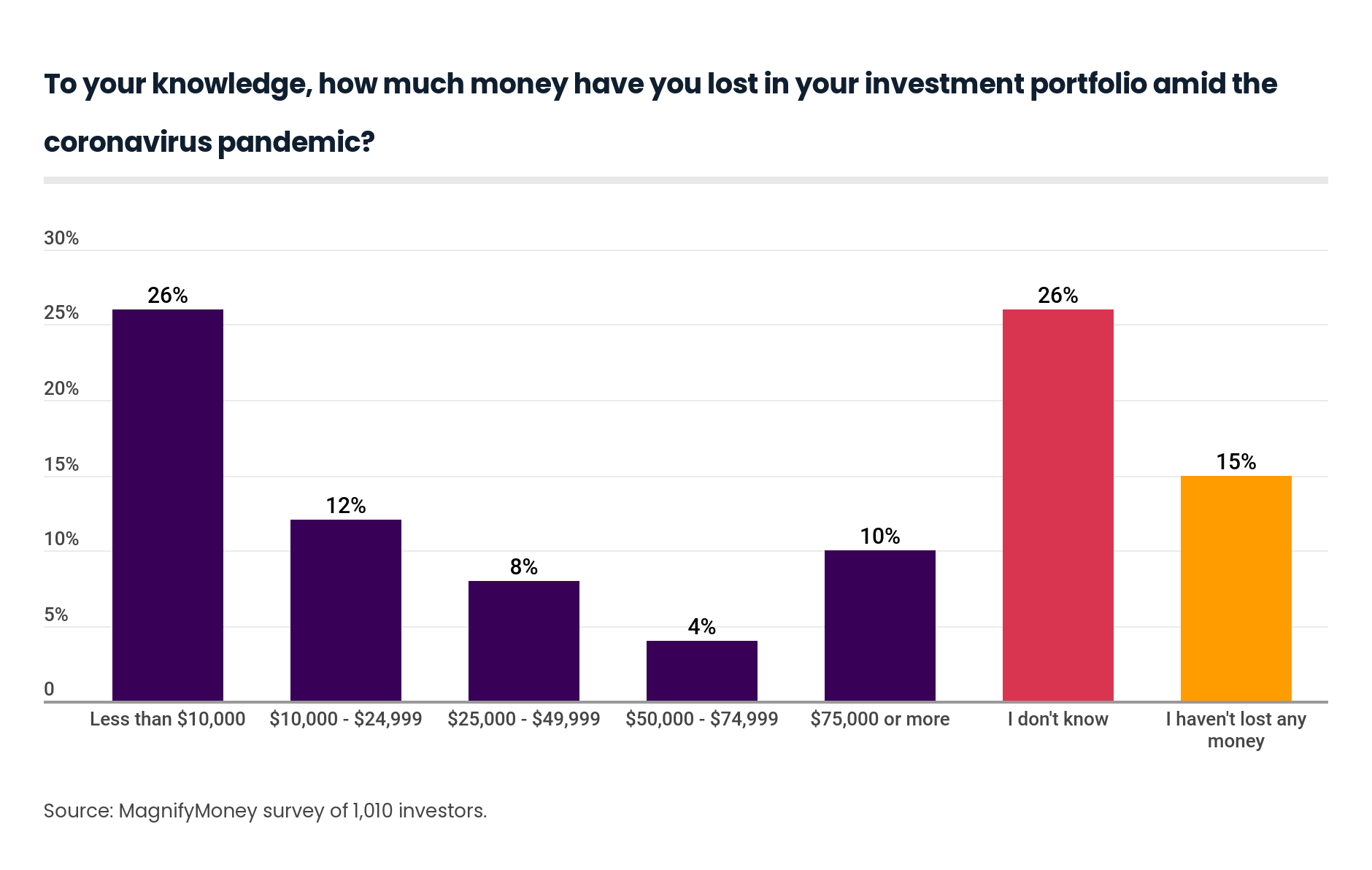

With markets swinging wildly and diving to new lows, investors have understandably lost money in the wake of the coronavirus pandemic. In fact, our survey reveals that the majority of investors (59%) have lost money — a figure that did not include the 26% of investors who were not sure if they had.

The bulk of investors who have lost money during the coronavirus outbreak, though, have lost less than $50,000, with 26% saying they lost less than $10,000, 12% saying they lost between $10,000 and $24,999 and 8% saying they lost between $25,000 and $49,999. However, some investors are reporting hefty losses, with 4% losing between $50,000 and $74,999 and 10% losing a staggering $75,000 or more. Meanwhile, our survey found that 15% of investors haven’t lost any money and 26% don’t know how much they have lost.

What’s arguably more alarming, though, is the sheer amount of investors (38%) who said they fear they have lost all of their retirement savings as fallout from the coronavirus pandemic continues to ravage the markets. While that percentage was fairly consistent across generations, it was highest among those in Generation Z. Nearly half (47%) of Gen Z worried their retirement savings would be completely wiped out, compared to 40% of millennials, 45% of Gen Xers and 30% of baby boomers.

One potential reason for the gap in concern between Gen Zers and baby boomers is that younger generations likely have far smaller nest eggs than their boomer counterparts, meaning it wouldn’t take as much market volatility to wipe out their retirement savings.

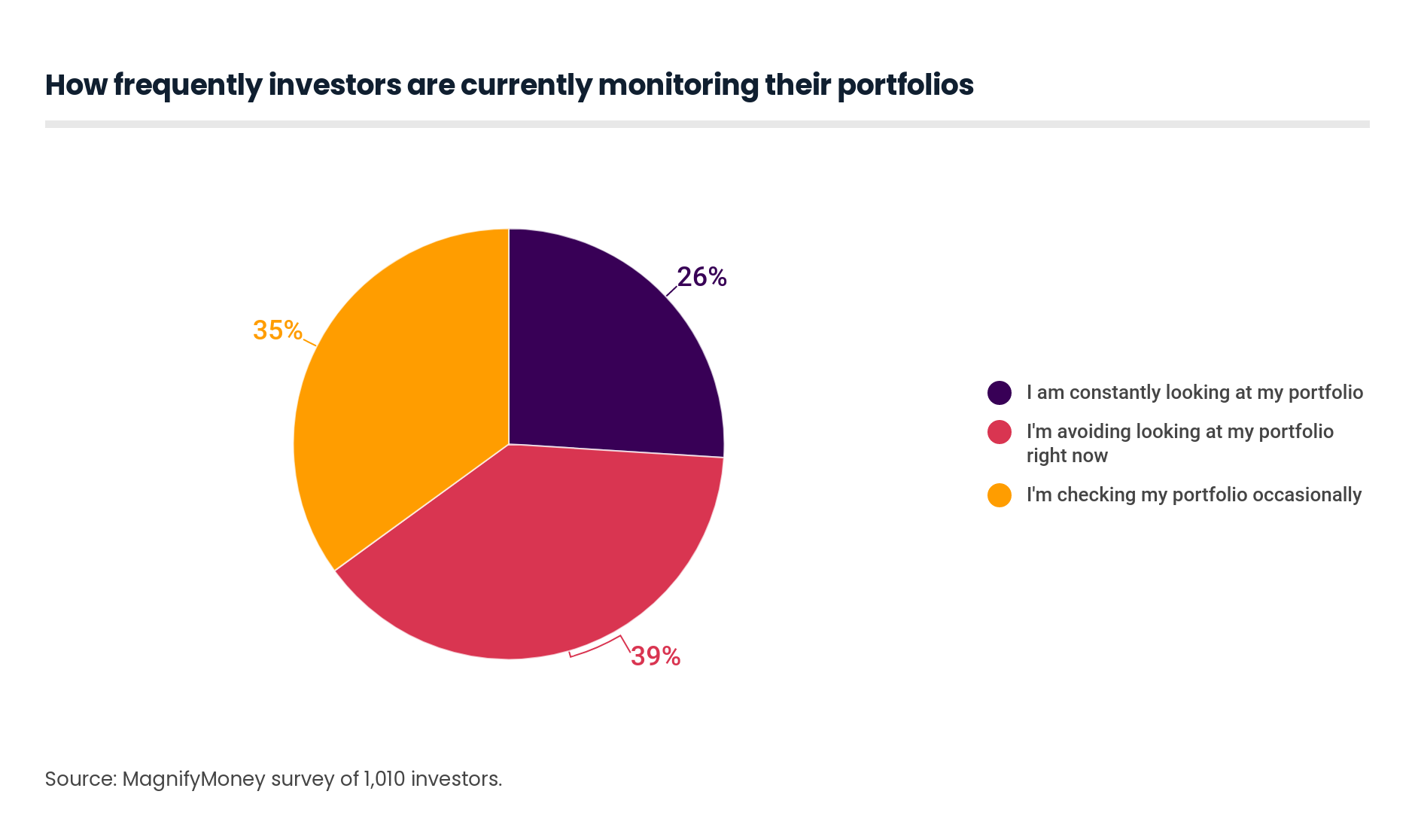

As the coronavirus pandemic continues to batter the economy, our survey found that many investors (39%) are choosing to avoid checking their portfolios altogether. Meanwhile, 35% of respondents said they are looking at their portfolios occasionally, while 26% said they are checking in constantly.

Of those who are shielding themselves from watching their portfolios plummet, many are baby boomers. Our survey revealed that almost half of baby boomers (48%) are steering clear of checking their portfolio right now, compared to 37% of Gen Xers, 35% of millennials and 27% of Gen Z.

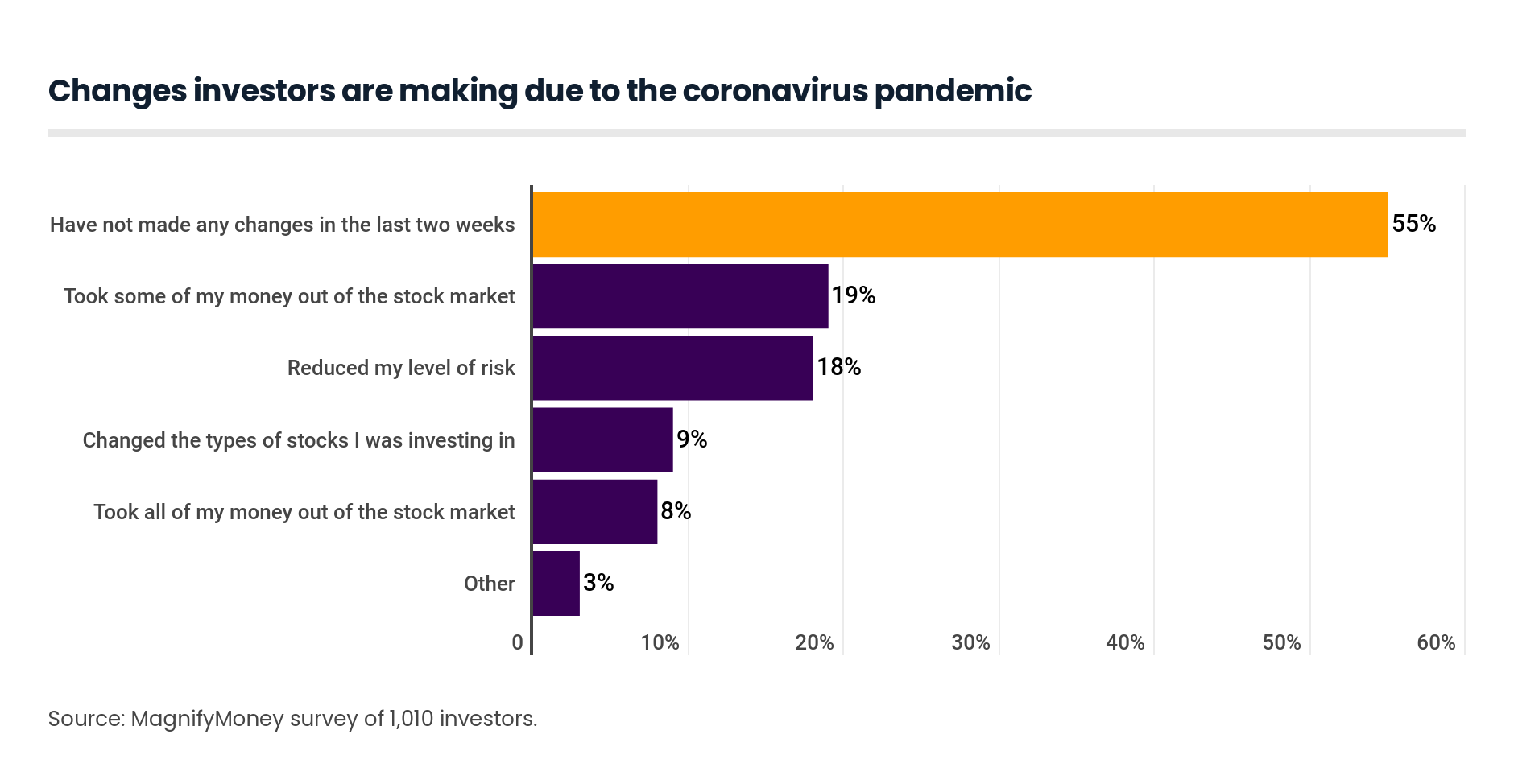

Despite the fact that many investors are opting against looking at their portfolios during this turbulent time, some are still making changes to their investing behavior in response to the coronavirus outbreak. Our survey found that while the majority of investors (55%) have not made any changes in the last two weeks, 19% have taken some money out of the stock market, 18% have reduced their level of risk, 9% have changed the type of stocks they’re investing in and a surprising 8% have taken all of their money out of the stock market.

Stock market ups and downs are par for the course when it comes to investing, and our survey suggests that even the coronavirus pandemic’s impact on the stock market isn’t enough to have a lasting effect on the confidence of many investors. In fact, we found that the majority of investors (78%) think that the stock market will recover from the drop associated with the coronavirus pandemic.

Still, 8% of investors said they don’t think the stock market will ever recover in their lifetime, while 15% investors said they didn’t know if it would. It’s worth highlighting, too, that Gen Zers were far more likely (18%) than any other generation to not have faith that the stock market will make a recovery in their lifetime.

While we did find that most investors are confident that the market will recover from the drop associated with the pandemic, that confidence doesn’t necessarily translate to comfort. In fact, our survey found that 11% of respondents said they will never again feel comfortable with the stock market, which could impact how — and whether — they invest again in the future.

Meanwhile, 29% of investors said they still feel comfortable with the stock market during these turbulent times, though most investors said they’d need to see the following major changes to feel comfortable again:

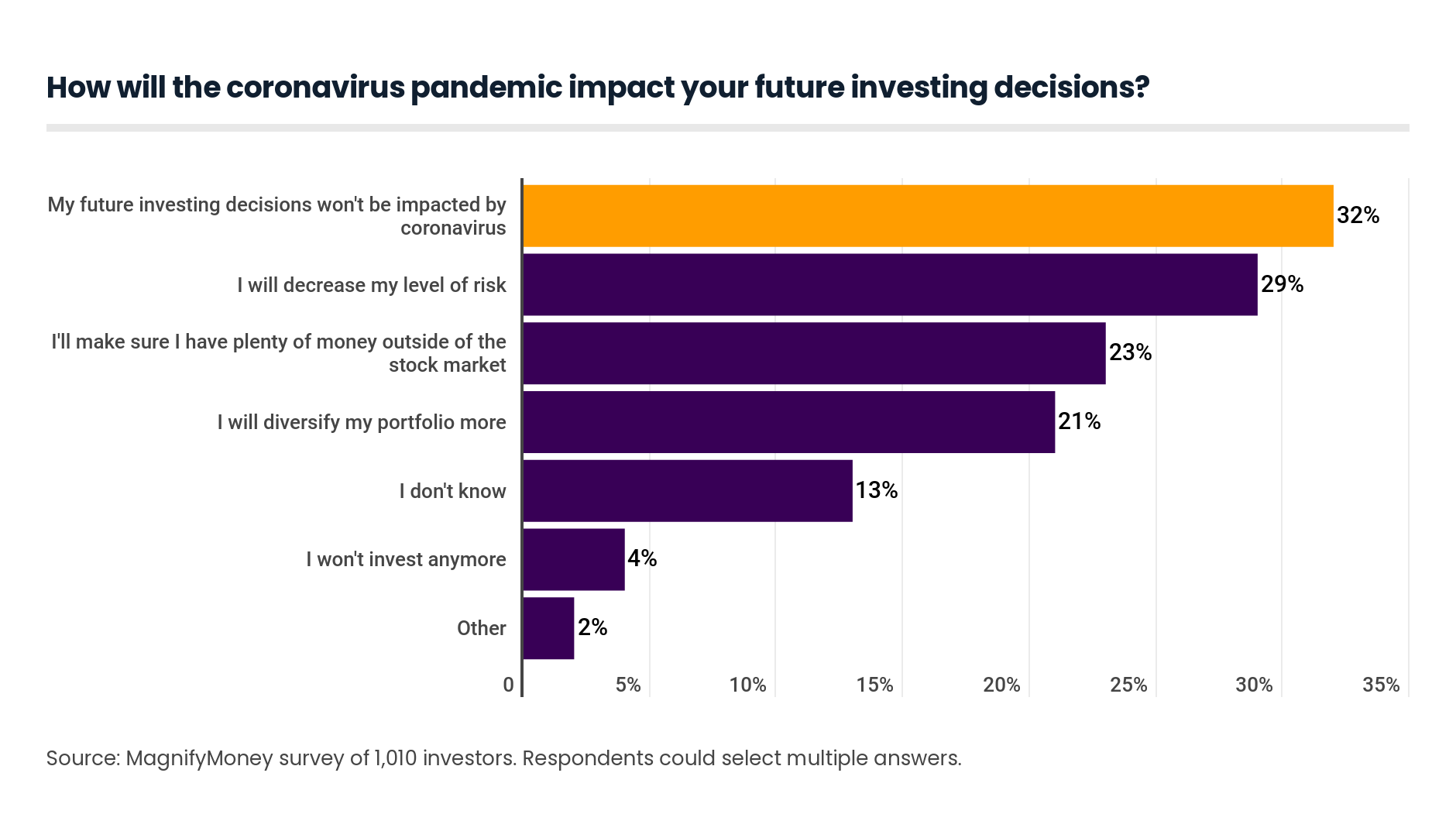

Aside from rattling investor confidence, our survey reveals the coronavirus outbreak could have lingering effects on investor behavior in the future. Only 32% of investors said their future investing decisions won’t be impacted by the coronavirus pandemic. Meanwhile, 29% said it will cause them to decrease their level of risk, 23% said that it would cause them to make sure they have enough money outside of the stock market and 21% said it will cause them to diversify their portfolio more. A striking 4% said they may not invest anymore.

When the stock market is taking multiple nose-dives as it has been recently, it’s understandable to feel uneasy. It’s important to remember, though, that investing is a critical component of building a healthy financial life, and stock market declines are par for the course.

In fact, market corrections — which is when the stock market drops 10% or more from its most recent high — happen every few years. Factoring in all corrections, the S&P 500 still has an average annual rate of return of around 10% over the longer term.

During times of turbulence, money moves you can make include:

MagnifyMoney conducted an online survey of 1,010 investors, with the sample base proportioned to represent the overall population. We defined generations as the following ages in 2020:

The survey was fielded through Qualtrics from March 18-19, 2020.

Sarah Berger

Sarah BergerSarah Berger is a former writer at LendingTree, where she covered personal finance, specifically focusing on challenges and opportunities facing millennials. Before joining LendingTree, she was a writer for CNBC and Bankrate.

Read More