MagnifyMoney

Do you find certificates of deposit (CDs) confusing? You’re not alone. MagnifyMoney found that many Americans find CDs confusing, too. Certificates of deposit do not have to be mystifying — in fact, CDs are a top savings strategy for high earners that are easy to use and provide a competitive rate of growth. Let’s look at what our respondents said about CDs, and show you how to break this cycle of CD skepticism and become a smarter saver.

A certificate of deposit is a time deposit that carries a fixed term and a set rate of interest. Financial institutions offer CDs in terms ranging from a few months to ten years or more. When you open a CD, you agree to keep your money in the account for the term of the deposit, in exchange for an interest rate that remains fixed over the term. Generally speaking, longer terms earn higher interest rates, with some CD offering rates that rival even the best online savings accounts listed on our site.

You can open a CD for a variety of reasons and savings goals. For short-term goals, you could open a three-month CD as a temporary parking spot for extra savings. For longer-term goals, you could choose a five-year CD as part of a plan to build a down payment for a home or a college education fund for your kids.

You immediately fund a CD when you open it at a bank or credit union, and once you’ve deposited your funds, you cannot withdraw money without penalty until the end of the term, also known as maturity.

Survey respondents said they most commonly used CDs for general long-term savings (49%). Opening a long-term CD at a high rate allows you to lock in the rate for years. Since the fixed rate won’t change, it protects against any potential rate drops in the future. Of course, this could also prevent you from taking advantage of potential rate increases, too.

A nearly equal number of respondents indicate they use their CDs for retirement savings (31%) or homebuying savings (30%). Nearly 22% said they use their CDs for college savings.

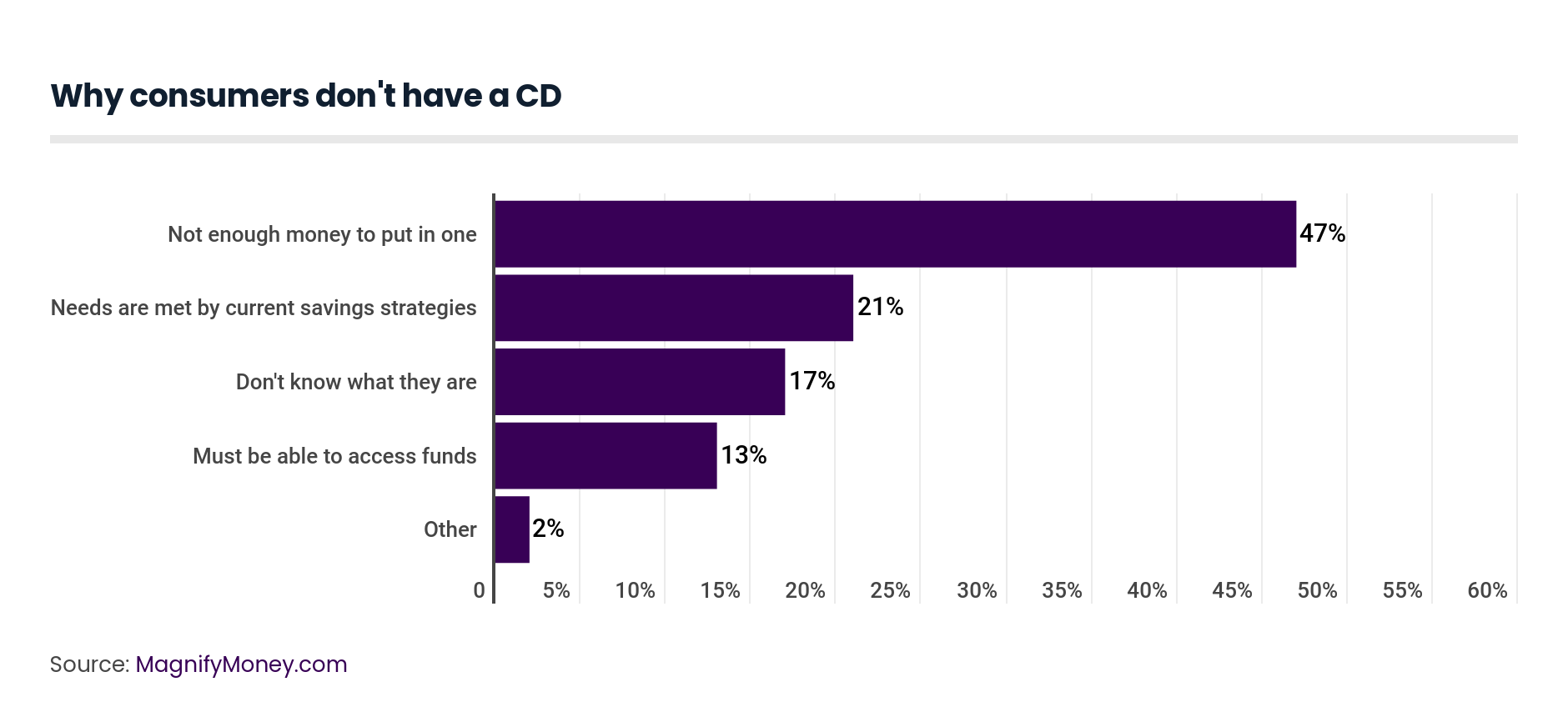

Nearly 47% of those without a CD said they don’t have enough money to put in one. Traditionally, CDs require minimum deposits of between $500 and $25,000 to open. Financial institutions use the money deposited in CDs to help fund their lending businesses — that’s part of the reason longer terms yield higher interest rates, as they help ensure access to longer-term funding.

However, some online bank CDs are turning this practice on its head, offering CDs with no minimum deposit requirement. That means you can deposit as little as $5 or $50 or even $0.01 to get your savings started. Of course, the larger the deposit, the more interest you earn over time and the larger the end payout will be.

Understandably, 13% of respondents said they need access to their funds. This can rule out CDs as a savings option, as you typically face heavy early withdrawal penalties for dipping into a CD before maturity — often losing all the interest you’ve earned. This is why CDs are more often used for excess savings, rather than savings intended to help with day-to-day needs or emergencies.

No-minimum deposit CDs are an affordable way to create a CD ladder, which gives you both the earning power of certificates of deposit and regular access to cash saved in CDs. Depending on the maturities you choose, a CD ladder provides predictable payouts. They do require a bit of extra planning and upkeep, which is perhaps part of why only 3% of our respondents said they use CDs ladders.

MagnifyMoney commissioned Qualtrics to conduct an online survey of 1,025 Americans, with the sample base proportioned to represent the overall population. The survey was fielded November 8-12, 2019.

Lauren Perez

Lauren PerezLauren Perez is a former writer at MagnifyMoney who covered deposit accounts and Federal Reserve meetings. Prior to joining LendingTree, she was a personal finance writer for SmartAsset. She has a B.A. in English from the University of Rochester.

Read More