MagnifyMoney

The presidential election will dominate headlines throughout 2020, with voters and pundits alike obsessively following polls, reading coverage and watching debates to get a feel for who’s leading in the race for the White House. In addition, they’ll be closely watching another key indicator for the race: the performance of the U.S. economy.

MagnifyMoney commissioned a survey of 1,000 Americans to gauge how people think about the relationship between the economy and the 2020 presidential election. Our survey found that nearly four in ten respondents said monitoring the economy helps them decide which candidate to support, and believe the results of an election can be at least somewhat predicted by the performance of the economy.

Our survey found that about 4 in 10 respondents think you can at least somewhat predict the outcome of the presidential election based on U.S. economic performance in the year leading up to the election. Meanwhile, 37% say that they do not think that economic performance could predict the election’s outcome, while nearly 22% were not sure.

Republicans were more likely than Democrats to say that economic performance could at least somewhat predict the 2020 election, 53% versus 43%. Meanwhile, 50% of millennials think that the state of the economy could at least somewhat predict the 2020 election, compared to 40% of Gen Xers and 32% of baby boomers.

Our survey asked whether people monitor the stock market and economic performance when deciding which presidential candidate to support. We found that the majority of people (64%) do not track such metrics when deciding who to support, while approximately 21% do somewhat and 15% do a great deal. The results didn’t differ greatly when considering party affiliation: 40% of Democrats and 42% of Republicans follow these metrics at least somewhat when determining who to vote for.

While our survey revealed that many people think that economic conditions can help predict the outcome of the 2020 election, we also asked respondents how they think the election will impact the economy once the polls close and the next president is selected.

Overall, people feel very differently about how the 2020 election results will impact the economy, with 31% of respondents saying it will positively affect it, 18% saying it will negatively affect it, 42% saying they are unsure how it will affect it and 9% saying it will not affect it at all.

Those results look somewhat different when party affiliation is taken into account: 41% of Republicans said the outcome of the election will positively impact the economy, compared to just 32% of Democrats. Meanwhile, Democrats were more likely to say that the election would have a negative impact on the economy, 19% compared to 14% of Republicans.

Different generations also had different thoughts on how the election’s results might affect the economy, with millennials (39%) most likely to say they think it will have a positive impact, followed by Gen Xers (28%) and baby boomers (24%). In contrast, Gen Xers were the generation most likely to say the election will have a negative economic impact (20%), followed by millennials (18%) and baby boomers (15%).

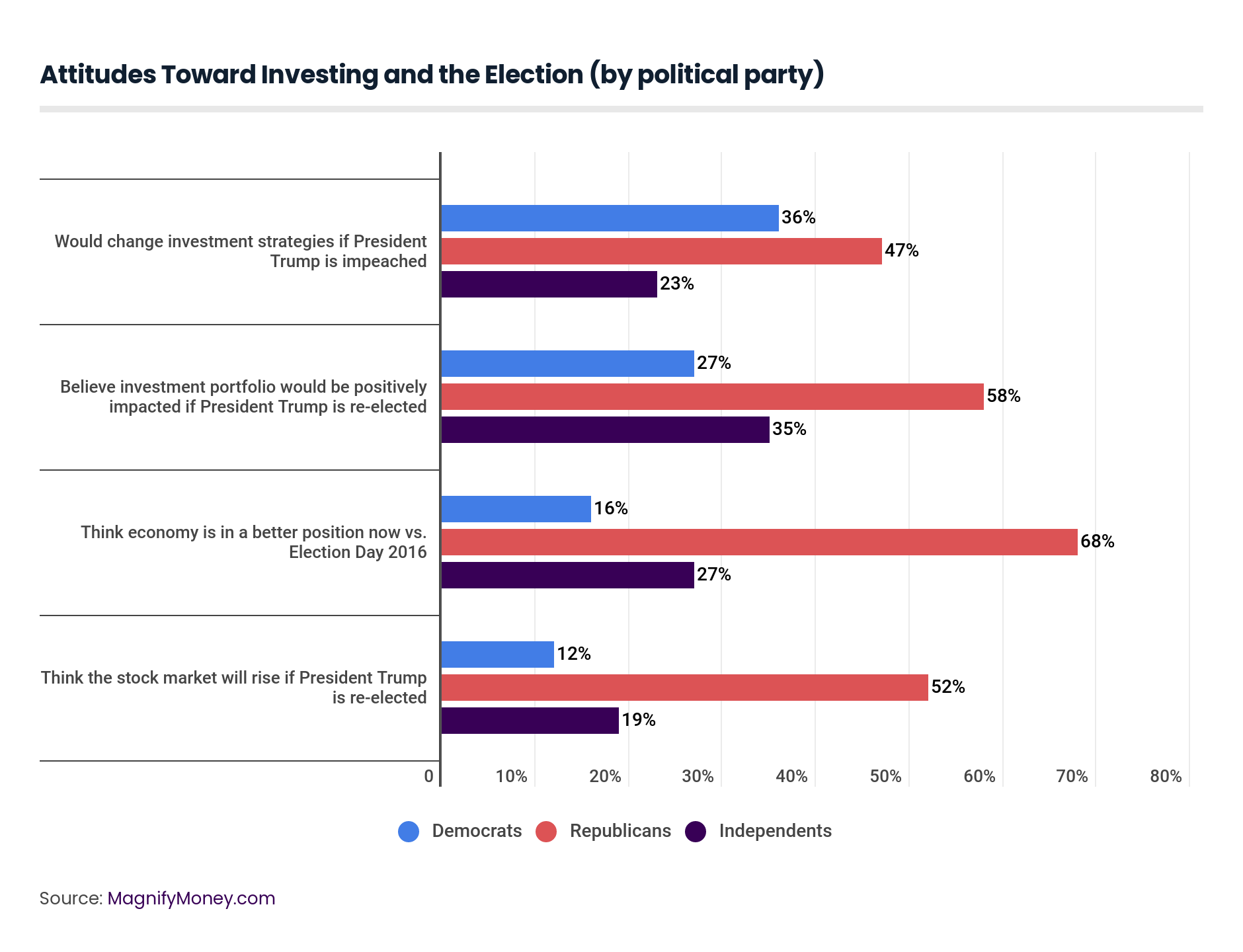

Our survey also revealed how people think the stock market will react to a President Trump re-election. Overall, 31% of respondents think that the stock market will fall if Trump is re-elected, 26% think the market would rise, 28% are unsure of how the market would react and 16% think it won’t change. Not surprisingly, 50% of Democrats think the stock market will fall with a Trump re-election, while 52% of Republicans think it will rise.

Everything from a CEO’s tweets to global trade deals has the potential to rattle an investor’s confidence — and our survey found that the 2020 election is no exception.

Interestingly, we found that overall, 37% of people avoid investing their money during election years. That includes 41% of Democrats and 39% of Republicans, as well as a whopping 56% of millennials, 29% of Gen Xers and 13% of baby boomers.

One reason for the lack of investment during election years could be chalked up to overall uneasiness about the state of the economy in general. When looking at the 2020 election in particular, many respondents aren’t too confident in many metrics that measure the health of the economy.

Overall, 28% of those surveyed are at least somewhat unconfident that the stock market will continue to rise, 30% are at least somewhat unconfident that the U.S. will continue adding jobs in the next 12 months and 29% are at least somewhat unconfident that the overall U.S. economy will continue to grow over the next 12 months.

When looking at confidence levels regarding the overall future of the economy, our survey found that Democrats are much more pessimistic than their Republican counterparts: 38% of Democrats were at least somewhat unconfident that the overall U.S. economy will continue to grow over the next 12 months, compared to just 19% of Republicans who feel the same way.

When looking at how the economy is now versus how it was on the night of the election in 2016, different political parties have very different viewpoints. Only 16% of Democrats think that the economy is in a better position now, compared to a whopping 68% of Republicans.

When asked which presidential candidate made them the most optimistic about the future U.S. economy and which one made them the most pessimistic, the most popular candidate was the same for both: Donald Trump. Overall, 33% of respondents said that Trump was the candidate that made them the most optimistic about the economic future, followed by Joe Biden (17%), Bernie Sanders (14%) and Elizabeth Warren (12%).

Meanwhile, 35% of respondents said that Trump was the candidate that made them the most pessimistic about the future of the U.S. economy, followed by Sanders and Biden (both at 14%) and then Warren (11%).

MagnifyMoney commissioned Qualtrics to conduct an online survey of 1,048 Americans, with the sample base proportioned to represent the general population. The survey was fielded October 1-3, 2019.

In the survey, generations are defined as:

Members of Generation Z (ages 18 to 22) and the Silent Generation (ages 74 and older) were also surveyed, and their responses are included within the total percentages among all respondents. However, their responses are excluded from the charts and age breakdowns due to the smaller population size among our survey sample.

Sarah Berger

Sarah BergerSarah Berger is a former writer at LendingTree, where she covered personal finance, specifically focusing on challenges and opportunities facing millennials. Before joining LendingTree, she was a writer for CNBC and Bankrate.

Read More