MagnifyMoney

It’s been more than a year since the U.S. had its first confirmed coronavirus case, but the latest MagnifyMoney survey is showing signs of financial optimism — especially among the youngest generations.

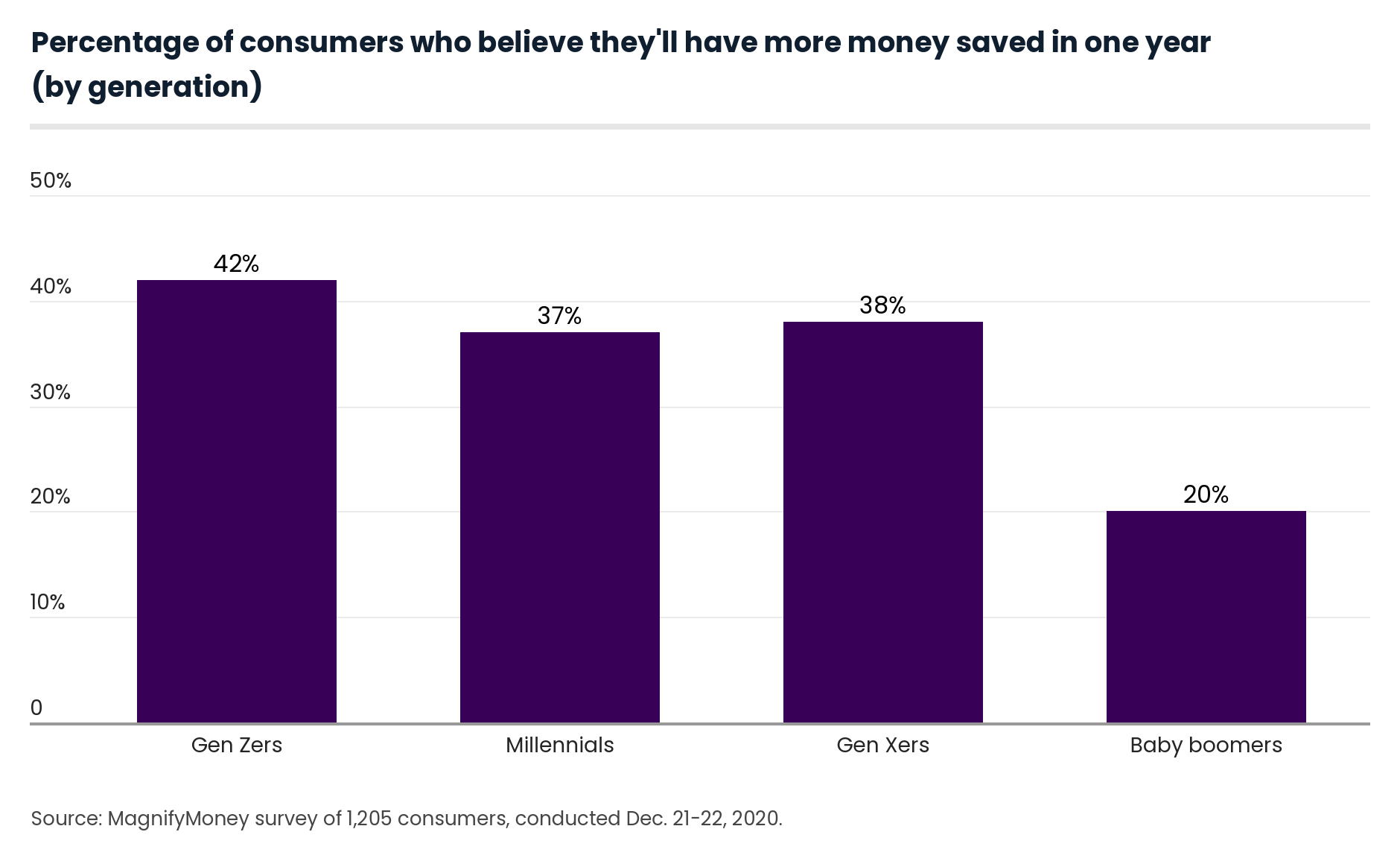

In fact, 42% of Generation Zers believe they’ll have a lot more money saved a year from now, while 41% of millennials think they’ll have less debt in a year.

Our survey asked more than 1,200 Americans about their finances — and where they think those finances will be a year from now. Here’s what we learned.

A third of Americans (33%) believe they’ll have significantly more money saved a year from now. Generation Zers (ages 18 to 23) are particularly optimistic, at 42%.

“COVID-19 has caused the world to come to a grinding halt, including expenses that Gen Z may have previously spent a significant amount of money on, like travel, concerts and dining out,” says Sarah Berger, MagnifyMoney’s millennial finance columnist.

These forced spending cutbacks give this younger generation more opportunity to save. Berger believes Gen Zers may be anticipating another round of economic impact payments that could boost their savings.

However, gender seemed to create an optimism gap: Nearly a quarter of women (24%) expect to have less money saved a year from now, compared with 16% of men.

The wage gap plays a role in men being more optimistic about their money, Berger says. If you make more money, you have more money to put toward saving and investing — which leads to financial security, which in turn leads to optimism.

Those in higher income brackets did express more financial optimism. In fact, 46% of those earning $100,000 or more think they’ll have a lot more money in savings this time next year, versus 28% of those who make less than $35,000. Meanwhile, a quarter of those in the lowest income bracket predict they’ll have a lot less saved, perhaps due to drawing from savings to cover expenses, versus 13% of six-figure earners.

Not everyone surveyed had such a positive outlook. A year from now, nearly half (48%) of respondents don’t think their savings will have changed much, while 20% think they’ll have a lot less saved.

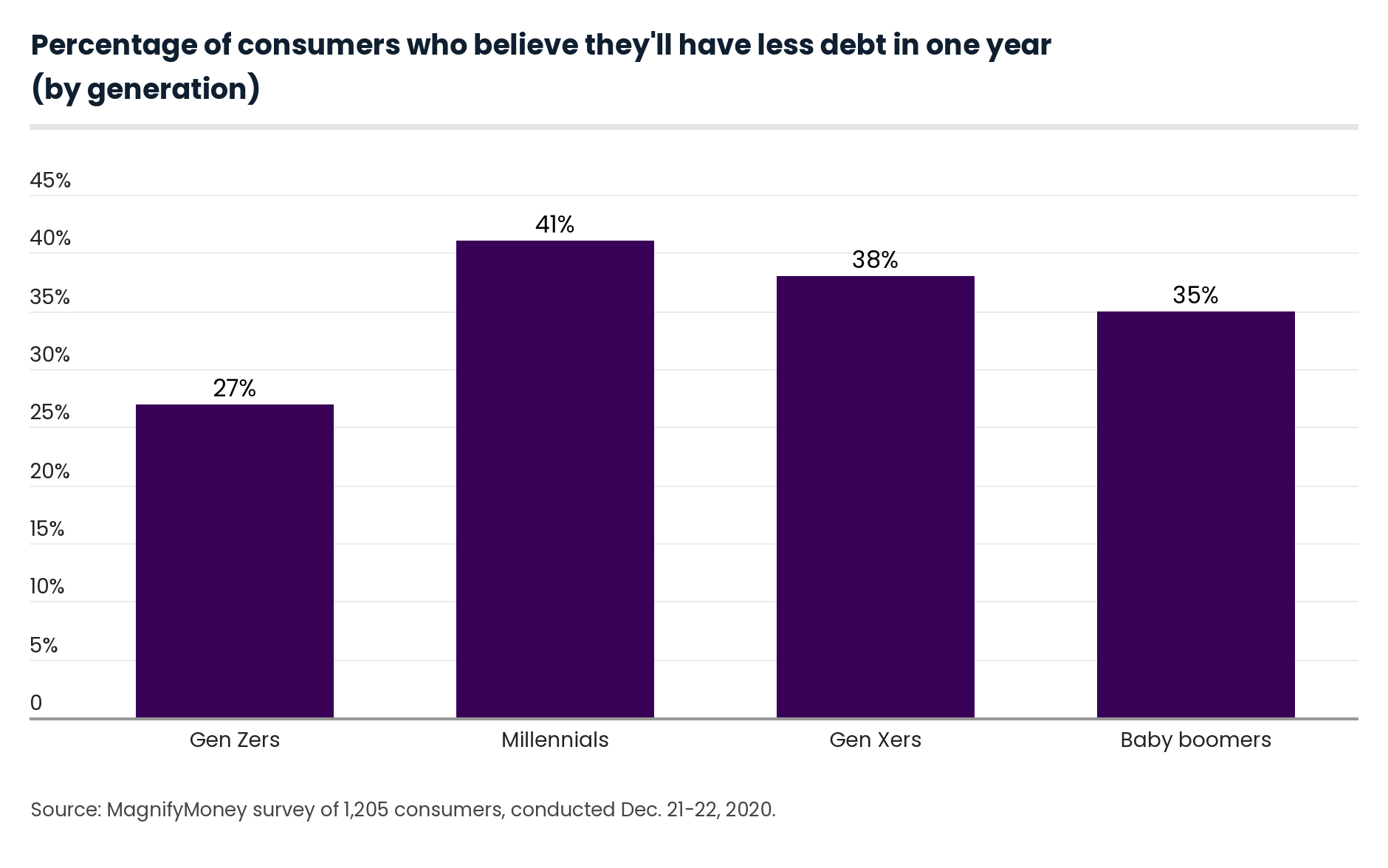

Overall, 37% of Americans believe they’ll have less debt a year from now, with 41% of millennials (ages 24 to 39) reporting they think they’ll have less debt then.

The reason that millennials may be so optimistic about having less debt a year from now could stem to where they are in their working lives.

At this point, says Berger, millennials — especially older millennials — are entering their prime working years. Millennials may be anticipating making more income and having more money to put toward paying off debt.

Separately, only 13% think they’ll have more debt, including 16% of Gen Xers (ages 40 to 54).

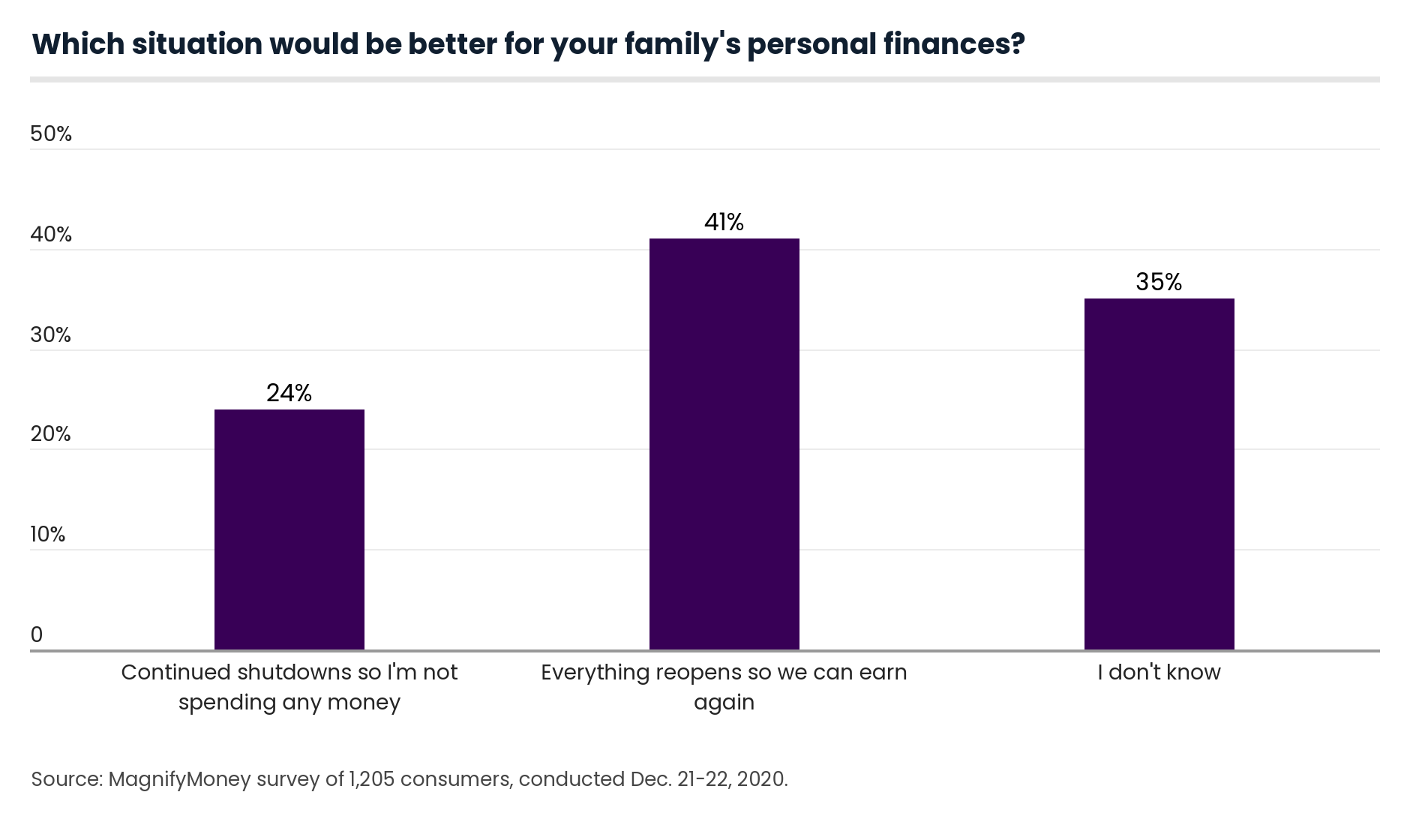

One surprising discovery from MagnifyMoney’s survey was that almost a quarter (24%) of consumers reported that continued shutdowns are better for their wallets. Why? They’re not spending as much money as they used to due to these shutdowns.

A third of Gen Z respondents said a continued shutdown is better for their wallet, because it makes them spend less money, while 27% of millennials agreed.

Another 41% said a completely reopened economy would be better for their finances, while 35% don’t know which path forward is better for them financially.

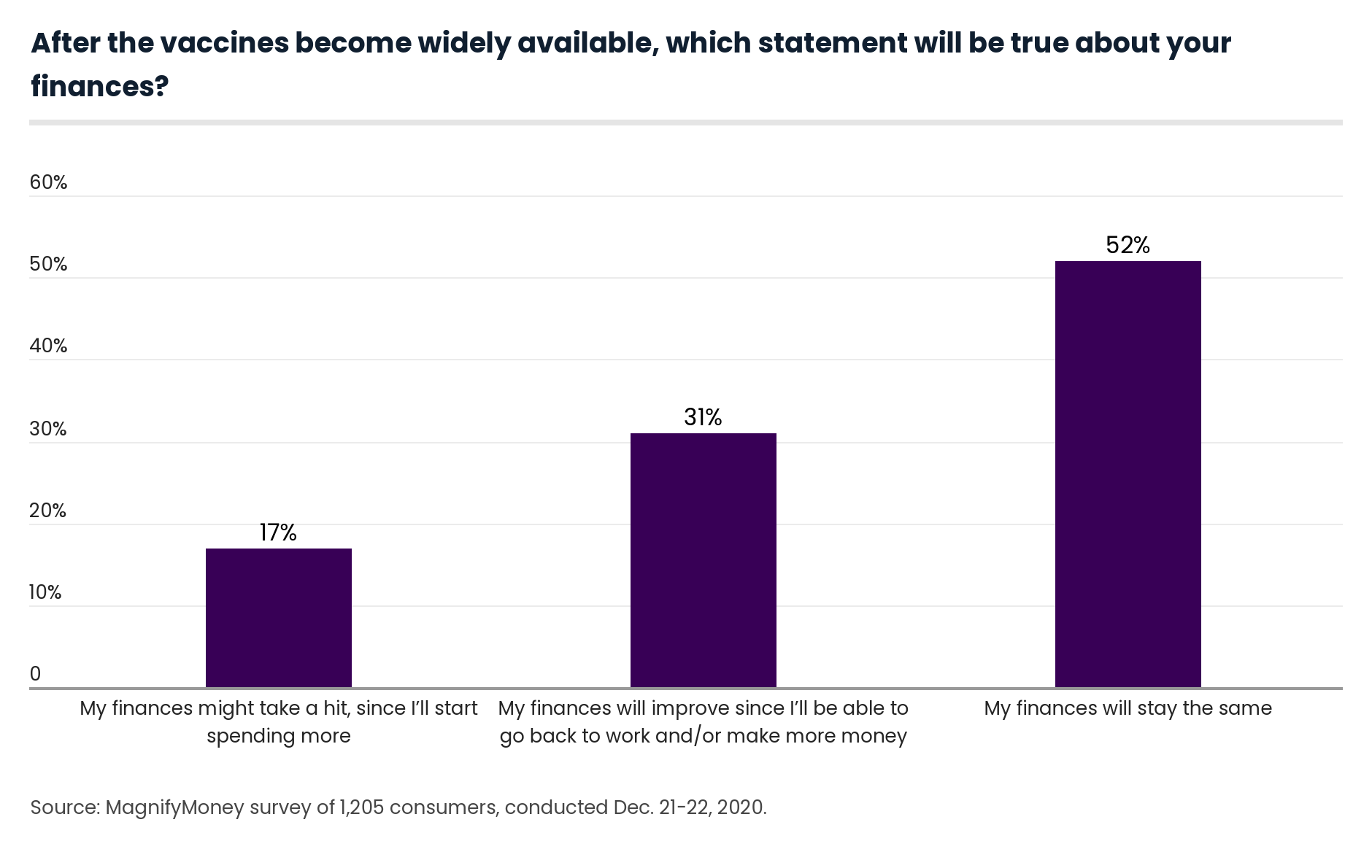

Even though nearly a quarter of respondents said continued shutdowns are better for their finances, 3 in 10 (31%) said their finances will improve after vaccines are widely available, believing that the end of shutdowns will allow them to return to work and/or make more money.

Optimism surrounding how the vaccine will affect finances is especially strong among those who lost their jobs or were furloughed (49%) and those who had their salaries or hours cut (47%). For them, a vaccine may signal a return to work and their pre-pandemic income levels.

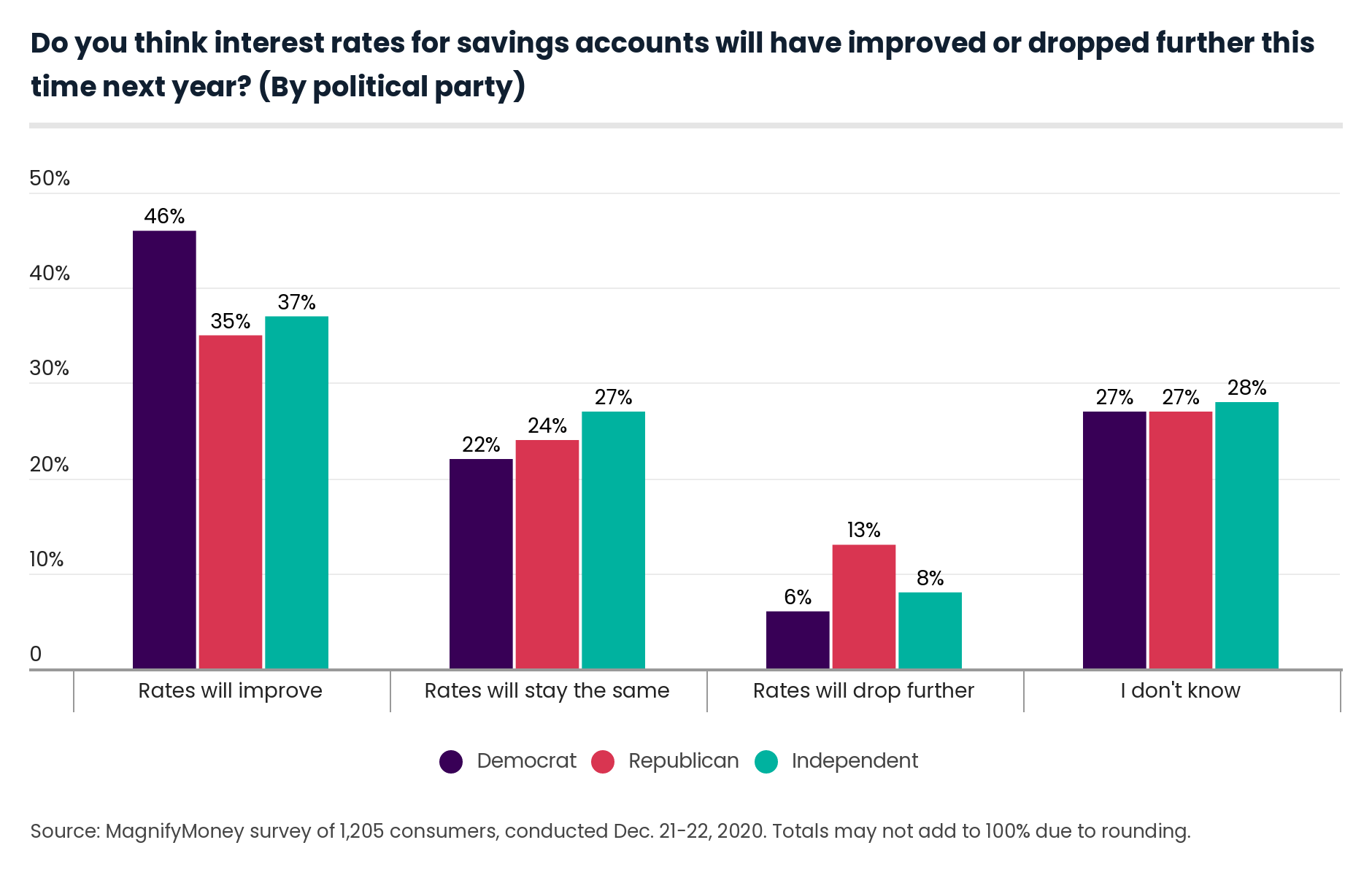

Some consumers are hopeful the new year will bring increased rates for savings accounts. In all, 39% predict rates will improve at least somewhat. Political party affiliation comes into play here, with Democrats feeling more optimistic about savings rate increases than Republicans.

As DepositAccounts founder Ken Tumin says, the health of the economy influences deposit rates. Not only does the economy drive the Federal Reserve’s interest rate policy, but it also impacts deposit levels and loan activity in the banking industry.

The stronger the economy, the higher the odds that there will be rising deposit rates.

“Democrats generally believe their policies are best for the economy, while Republicans generally believe the opposite,” Tumin says. “Thus, it makes sense Democrats are more optimistic about future deposit rates based on the changes that are taking place.”

Looking forward to next year, Tumin predicts that deposit rates will likely be close to where they are now. “In 2020, deposit rates have fallen to all-time lows at many banks and credit unions, but the interest rate declines are slowing,” Tumin says. “There are indications that deposit rates may be near a bottom in early 2021.”

Tumin believes that significant deposit rate increases are unlikely to occur within the next year. “Even if the COVID-19 vaccine program is extremely successful and the economy has a very strong recovery through 2021, the Fed will almost certainly keep its benchmark rate near zero in 2021,” Tumin says.

And even if the Fed holds rates steady, Tumin says a very strong economic recovery may have a small positive impact on deposit rates, especially on CD rates.

Our survey also asked how people feel about their current financial life.

While 39% of respondents said their finances have stayed the same throughout the pandemic, an equal amount (39%) reported that their finances took a hit due to income either they or another member of their household lost during the pandemic.

Those affected the most earn less than $35,000 a year.

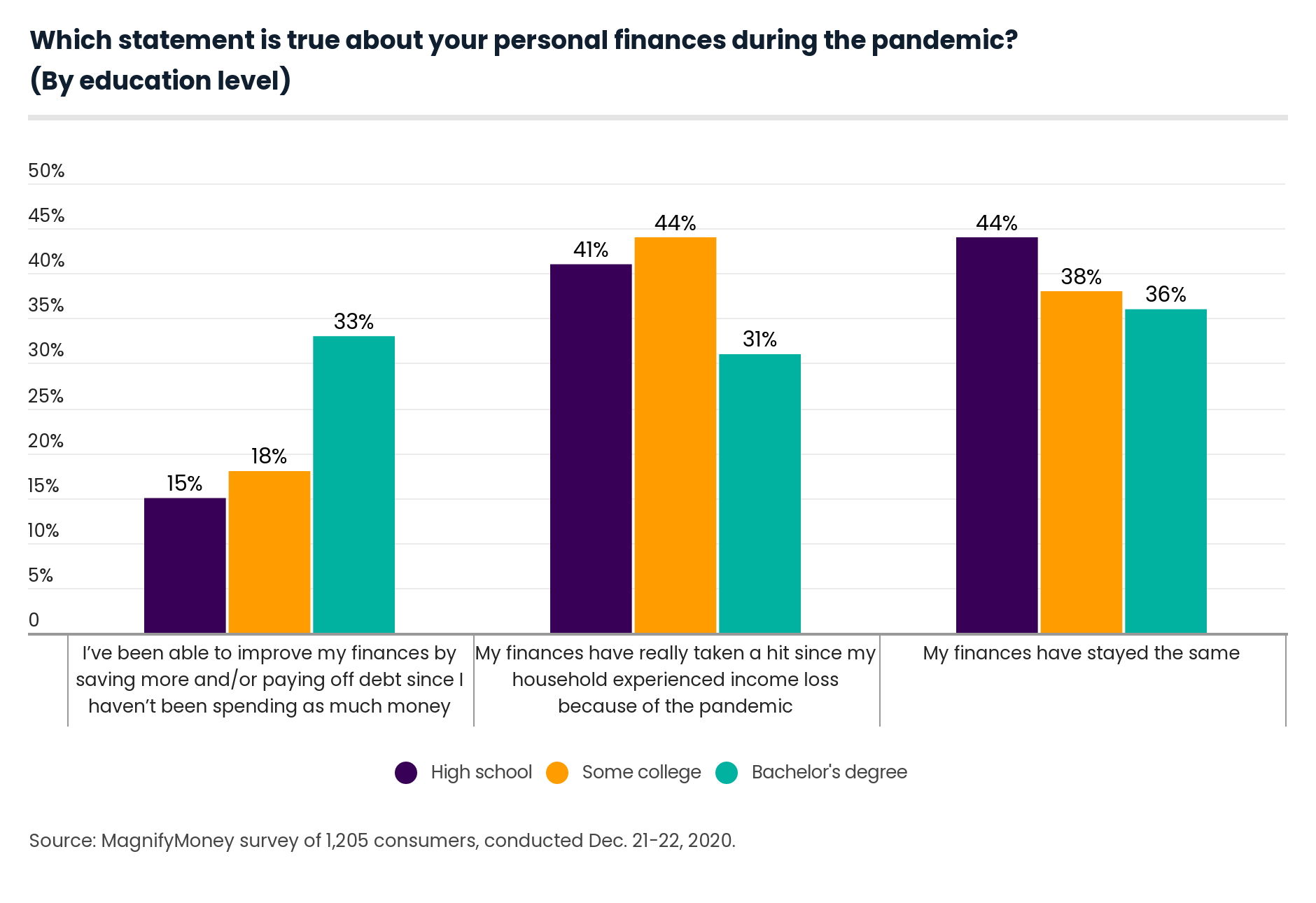

There was also an education gap: A third of bachelor’s degree holders said their finances have improved during the coronavirus crisis, versus 18% of those with some college education but no degree and 15% of high school graduates.

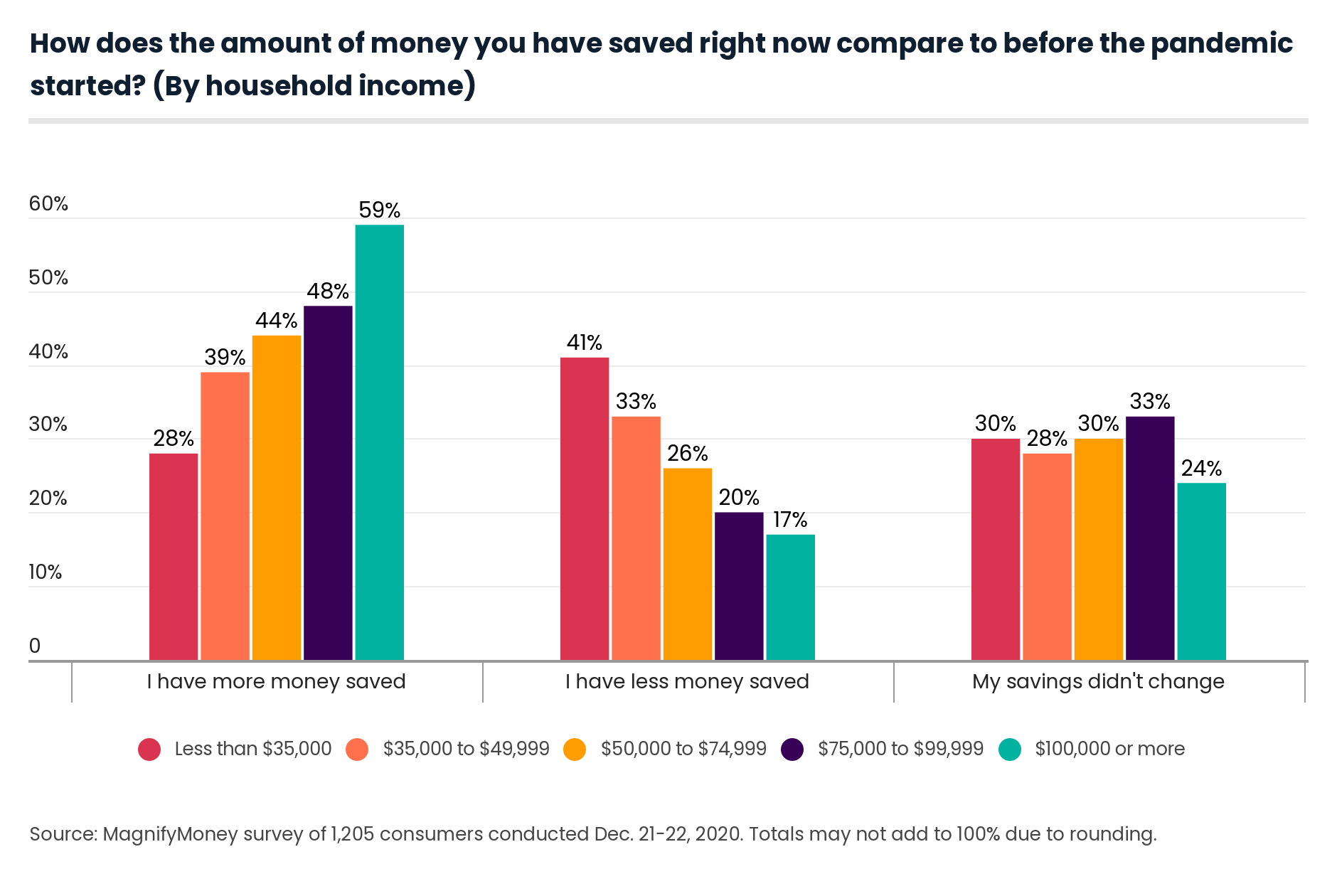

In general, 38% of consumers said they have more saved now than they did before the pandemic, while 33% said they have less money saved now.

Again, income levels and education levels continued to affect respondents. In fact, 59% of those with a household income of $100,000 or more increased their savings during the pandemic, compared with 28% of those earning less than $35,000. Meanwhile, only 17% of six-figure earners have decreased their savings, compared with 41% of those earning less than $35,000.

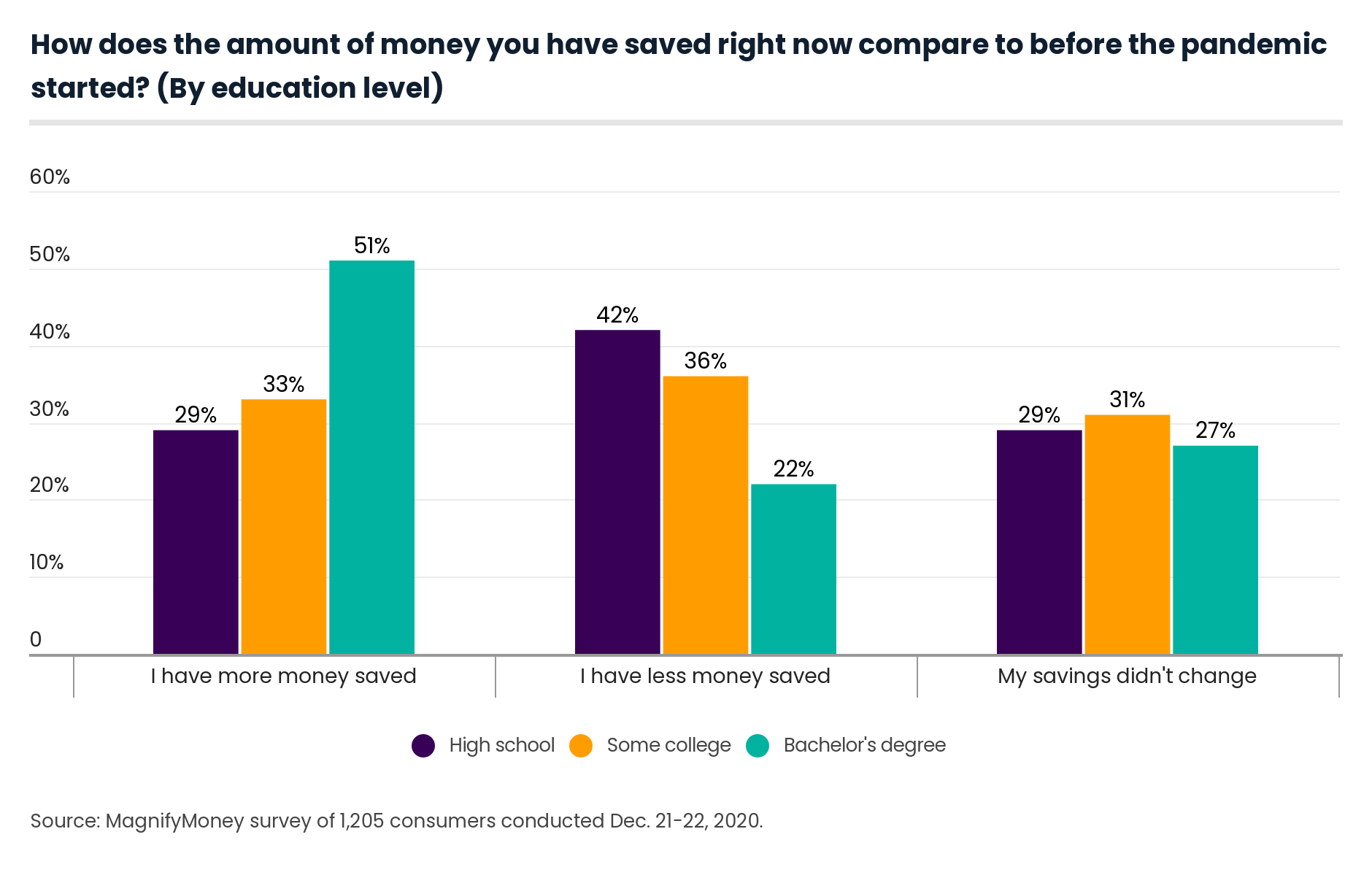

When it comes to education, 51% of college graduates increased their savings during the pandemic, versus 33% of those with some college and 29% with a high school education.

If you’re looking to boost your savings during the pandemic, Tumin recommends trying to automate your savings so that you regularly make contributions to your emergency fund and short-term goal funds. Creating good spending habits that will hopefully extend past the pandemic helps too.

“The pandemic has encouraged people to spend less,” Tumin says. “Many people have saved money by eating out less and cutting back on travel and other entertainment activities. I can see that contributing to these positive results.”

MagnifyMoney commissioned Qualtrics to field an online survey of 1,205 Americans, conducted Dec. 21-22, 2020. The survey was administered using a non-probability-based sample, and quotas were used to ensure the sample base represented the overall population. All responses were reviewed by researchers for quality control.

We defined generations as the following ages in 2020:

While the survey also included consumers from the silent generation (defined as those 75 and older), the sample size was too small to include findings related to that group in the generational breakdowns.

Jacqueline DeMarco

Jacqueline DeMarcoJacqueline DeMarco is a freelance writer who is particularly passionate about finance. She began her career in the retirement industry. Today, she works with more than a dozen financial brands to create entertaining and educational money content.

Read More