MagnifyMoney

The coronavirus pandemic has changed almost everyone’s lives, but many parents have had to navigate especially choppy waters. With schools having sporadic periods of virtual learning and day cares sometimes closing due to outbreaks, some parents have needed to work from home without child care.

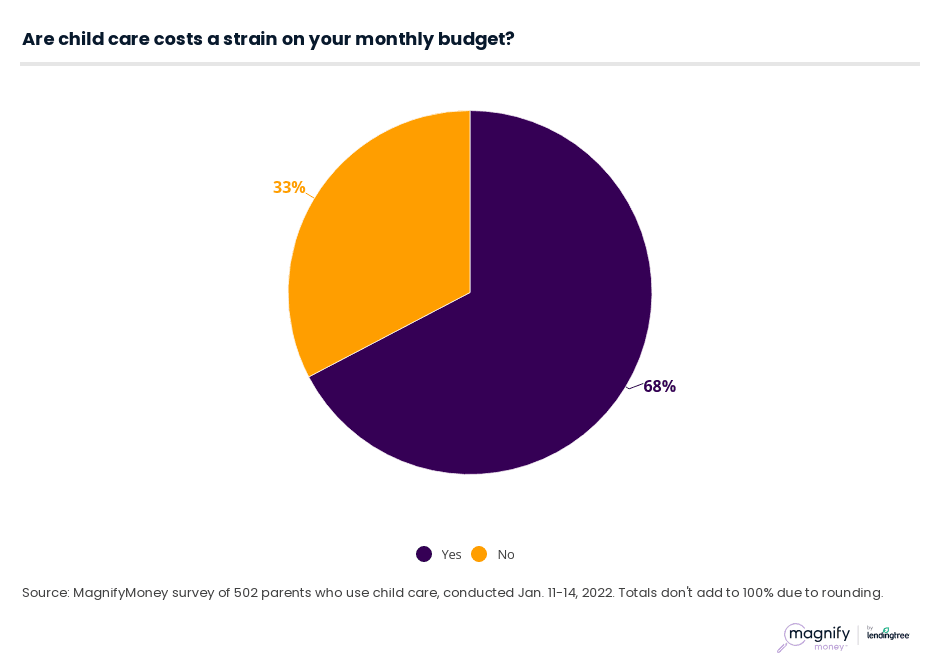

At the same time, those able to secure child care have done so at a steep cost. Nearly 70% of parents with children younger than 18 who use child care say the costs are a strain on their monthly budget (and their savings), according to the newest MagnifyMoney survey of more than 1,000 of these parents.

The MagnifyMoney survey looks deeper at the pandemic’s role in the changing face of child care — keep reading for more insights.

Child care can be a major expense — especially for the 68% of parents who use it and report it causes a strain on their monthly budget. (For this survey, child care options included day care, babysitting, family or friends, before- or after-school programs and other.)

This percentage rises among parents who:

Nearly half of parents with kids younger than 18 (46%) use some form of child care — and according to Matt Schulz, LendingTree chief credit analyst, the only option for many parents is to pay for it. They’re being put in nearly impossible situations, he says, and even parents who have slightly more flexibility have been left with difficult choices.

“Often, one partner’s job may not bring home much more money than it costs to keep their kid in child care,” Schulz says. “Then you have to decide whether that job is ultimately worth it financially. It’s a really tough spot that many parents around this country face every single day.”

To help cover the financial burden of child care, 1 in 3 parents who use child care relied on credit cards to make those payments in the past year. Schulz advises against doing so, but acknowledges there’s sometimes no other choice.

If you have to pay with a credit card, Schulz recommends making sure that you’re paying as much as you can on your card each month. You could also consider calling your credit card issuer and asking for a lower interest rate.

“It works far more often than you’d expect, and it can really save you money,” Schulz says.

Child care expenses stop some parents from making the most of their money. In fact, 38% of parents say that child care costs have prevented them from achieving at least one specific financial goal, with paying off debt at the top of the list. But Schulz is surprised the cost of child care isn’t causing more parents to not reach financial goals.

“Child care costs can really hamstring a family’s budget in a huge way,” Schulz says. “It can keep a parent from going back to work after their kid is born, it can keep them from paying off credit card debt, building an emergency fund, saving for retirement or college and many other things.”

To stay on track to reach these important financial goals, Schulz says that having a budget is key. Knowing how much money is coming in and going out of your household can help you make the best use of your funds. It allows you to prioritize certain expenses and cut back on others, especially when child care is in the mix.

The 44% of working parents who worry that a lack of child care will hurt their career is up from 30% in the summer of 2020, but there are caveats to that. The 2020 question asked specifically whether respondents were worried a lack of child care would cause them to lose their jobs, while this question asked whether they feared it would hurt their careers.

Given the circumstances, that concern is higher among parents who work from home than those who work in-person (49% versus 37%, respectively). And understandably, a lack of child care impacts parents’ abilities to work — more than half of working parents (56%) say it’s affected their ability to work at least once during the pandemic.

Here’s a deeper breakdown of how many times respondents say that lacking child care has impacted their ability to work:

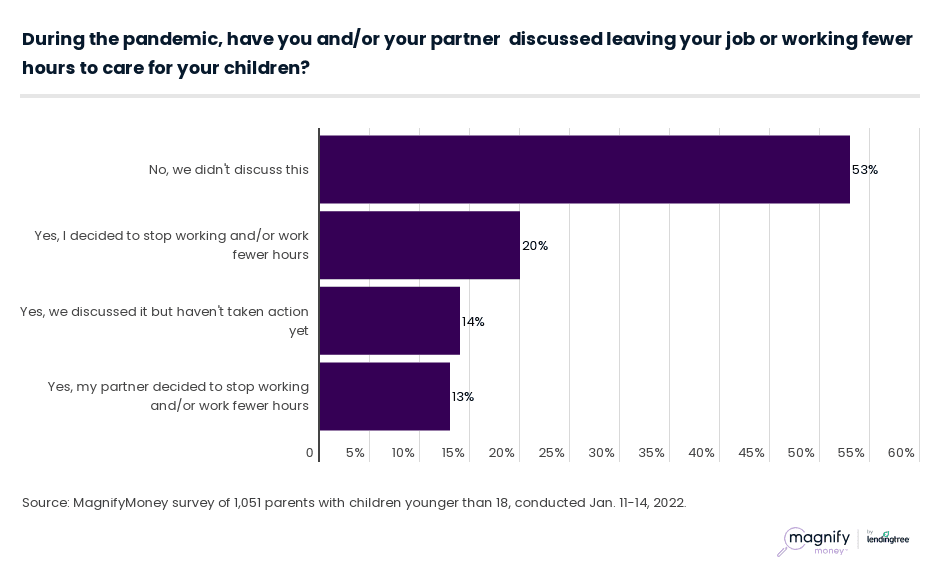

These child care disruptions may even cause some parents to reconsider their working situations. A third (33%) say they or their partner chose to stop working (and become a stay-at-home parent) or work fewer hours to care for their children.

In some cases, parents were able to make things work by switching to remote work or getting a new job that allowed them to do so. More than 4 in 10 (42%) say they or their partner switched to remote work for child care reasons.

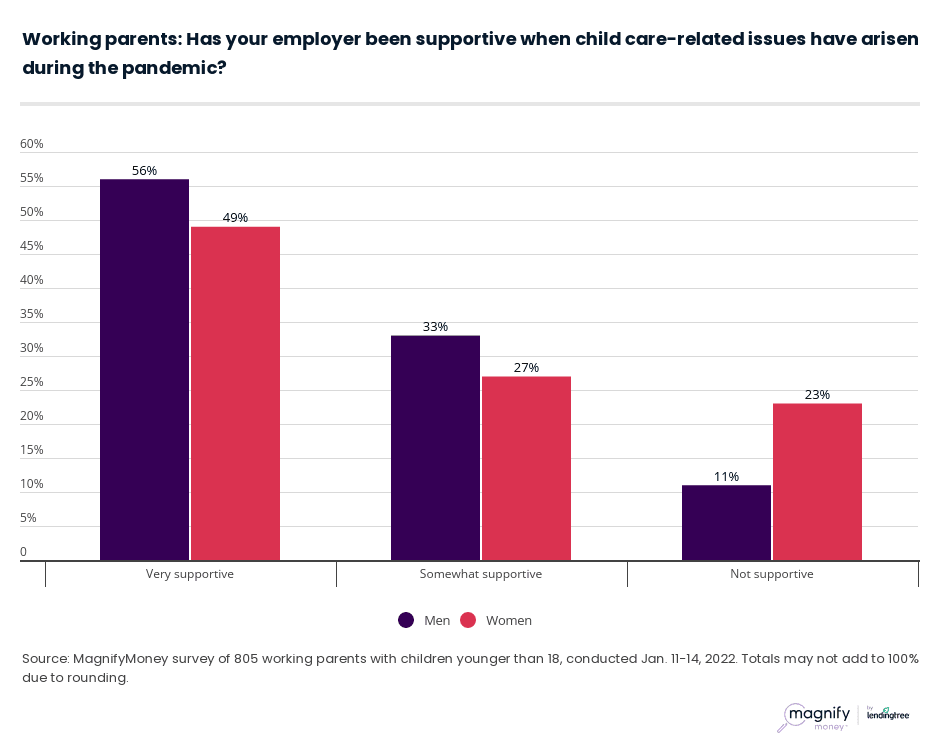

Women, in particular, are struggling with the impact of child care issues on their careers. Almost a quarter of working women report their employer hasn’t been supportive of related problems that have arisen during the pandemic — and it’s double the percentage of men who have experienced the same struggles (23% versus 11%).

On the brighter side, 53% of working parents overall report their employer is generally supportive of any child care-related issues that have arisen during the pandemic.

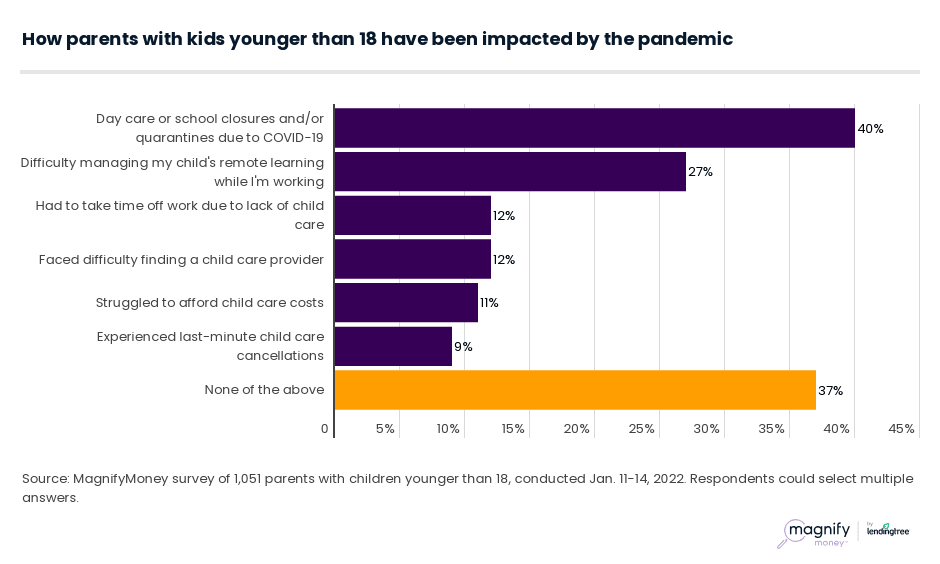

Considering that 63% of parents faced child care-related challenges amid the pandemic, this level of support from employers is necessary — especially for working mothers. Mothers working full time are more likely than full-time working fathers to cite difficulty managing their child’s remote learning during the workday (39% versus 28%).

For parents that hit financial speed bumps in the past year or two, it’s important to remember that they can bounce back. Schulz shares some tips for getting back to a good place.

MagnifyMoney commissioned Qualtrics to conduct an online survey of 1,051 parents with children younger than 18, fielded Jan. 11-14, 2022. The survey was administered using a nonprobability-based sample, and quotas were used to ensure the sample base represented the overall population. All responses were reviewed by researchers for quality control.

Jacqueline DeMarco

Jacqueline DeMarcoJacqueline DeMarco is a freelance writer who is particularly passionate about finance. She began her career in the retirement industry. Today, she works with more than a dozen financial brands to create entertaining and educational money content.

Read More