MagnifyMoney

The coronavirus (COVID-19) outbreak, and its lack of predictability, has thrown us into uncharted territory economically, politically and personally. Many Americans have started stockpiling cash in response to the pandemic, a new survey by MagnifyMoney found.

From buying toilet paper in bulk to stashing cash, we’re all trying to take steps toward preparedness and to feel some measure of control in the face of uncertainty. But should you really stockpile cash?

In the survey, MagnifyMoney asked over 1,500 Americans about their money habits in this time of crisis. Here’s what we found about why Americans are withdrawing their funds, and whether it’s necessary.

Those who have stockpiled cash said they were primarily motivated by three factors:

Interestingly, 21% of those who took out cash weren’t exactly sure why they were doing it, indicating that “it just felt like the right thing to do.” Additionally, 1 in 10 respondents seemed to be following the crowd, saying they withdrew cash at the advice of someone else.

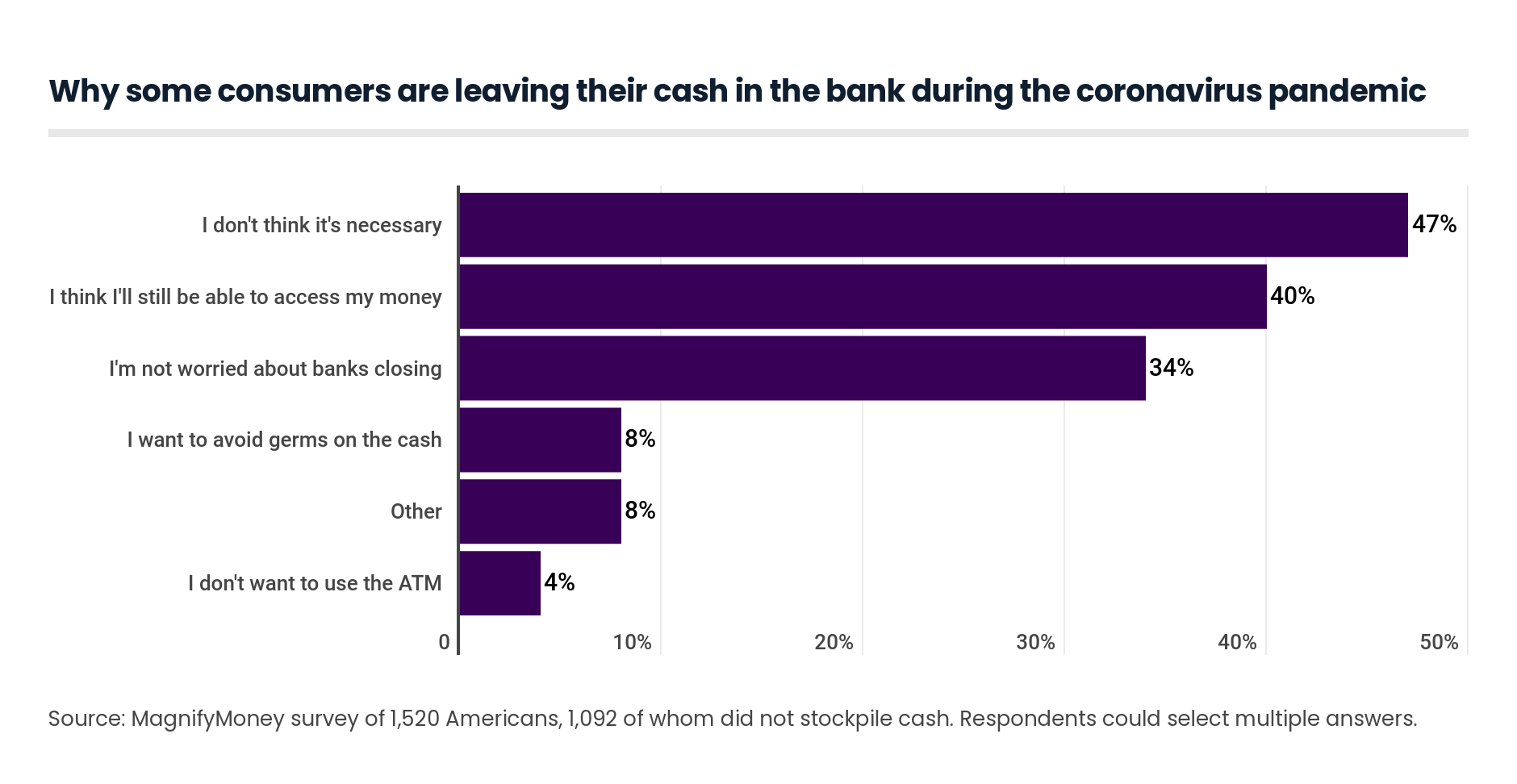

While 1 in 3 Americans have chosen to stockpile cash, 72% of respondents had not done so at the time of our survey. When asked about their decision to leave their money in the bank, 47% said they just didn’t think it was necessary to withdraw cash. This was the most common reason cited.

Another 40% believe they’ll still have access to their money despite the coronavirus pandemic, while 34% aren’t concerned about banks closing. Meanwhile, 8% of respondents said they wanted to avoid the germs found on cash.

Luckily, there’s no indication that banks are about to shut down. While some banks have chosen to temporarily cut hours, close select branches or move to drive-thru services only, the Federal Reserve’s expansive emergency measures ensure there’s little risk of your bank shutting down completely either tomorrow or even in the next few months. Banks staying in business also ensure that you’ll continue to have online and in-person access to your funds through branches that remain open and bank ATMs. Check your institution’s official social media accounts for the most up-to-date alerts on their services and policies.

While the desire to have cash during emergencies is entirely understandable, we shouldn’t expect society to devolve into an entirely off-the-grid operation during this time. Still, withdrawing one large sum of cash at the start of the crisis does mean fewer trips to the bank during this time of social distancing. Additionally, having a stash of cash makes payments easier when you need to make a quick run to the corner store.

Before stockpiling cash, also remember that your money is protected at all times — whether in a crisis or not — by the Federal Deposit Insurance Corporation (FDIC) for bank deposits or the National Credit Union Administration (NCUA) for credit union deposits. These institutions insure your deposits up to legal limits in case of bank failure, which means you’ll never truly lose your money if your institution fails. You’ll either receive a check for the amount that was in your account, or get set up with a new account at another insured institution for the same amount.

Typically, the legal limit on a single deposit account maxes out at $250,000 for an individual. But the new CARES Act has given both the FDIC and NCUA authority to temporarily provide unlimited insurance through Dec. 31, 2020, to support Americans and their finances through this time of crisis.

Of course, if you’re handling cash — or any other form of payment, really — you should make sure you’re washing your hands frequently as per guidelines from the Centers for Disease Control and Prevention (CDC).

MagnifyMoney conducted an online survey of 1,520 Americans, with the sample base proportioned to represent the overall population. We defined generations as the following ages in 2020:

The survey was fielded through Qualtrics from March 18-19, 2020.

For more information on the rest of the stimulus package, refer to our hub page.

Lauren Perez

Lauren PerezLauren Perez is a former writer at MagnifyMoney who covered deposit accounts and Federal Reserve meetings. Prior to joining LendingTree, she was a personal finance writer for SmartAsset. She has a B.A. in English from the University of Rochester.

Read More