MagnifyMoney

Most Americans believe the nation’s economy will be in a recession in the next six months, according to the newest survey from MagnifyMoney — just over two-thirds of consumers say they’re not financially ready for it.

That last part is particularly troubling — especially considering that Americans are not too far removed from a period in which credit card debt fell significantly, savings rates soared to never-before-seen heights and delinquency rates stayed at or near historic lows.

The truth, however, is that resurgent spending, rising interest rates and rampant inflation have begun to take a toll on millions of Americans, leaving them concerned about their preparedness for the next economic downturn — which may already be underway.

This survey of more than 2,000 consumers wasn’t all doom and gloom, though. A large majority of Americans say they’ve taken at least one step to prepare for a potential recession.

Most people have heard the term “recession” regarding the economy, and most understand — at least to some degree — that it’s a bad thing, a significant rough patch for the nation’s economy. However, much like all squares are rectangles but not all rectangles are squares, all recessions are economic downturns but not all economic downturns are recessions.

That may make its start and stop dates a little harder to judge. A mild, short period of decline may not qualify, while a brief but incredibly intense period of decline — such as what we saw in early 2020 — may make the cut.

It’s important to understand when reviewing this survey data, however, that many — maybe even most — of those surveyed don’t know the textbook definition of a recession, nor have they ever heard of the NBER. We simply asked them “Do you think a recession is coming?” Seven in 10 (70%) say yes, while just 6% say no. (Another 24% say they aren’t sure.)

The most likely to say a recession is on the way:

Meanwhile, just 46% of Gen Zers (ages 18 to 25) say they think a recession is coming. However, that doesn’t mean they’re super-optimistic — 42% of Gen Zers say they aren’t sure, far higher than any other age group.

Of the 70% who think a recession is coming, 59% expect it to happen in the next six months. Among the various demographics, six-figure earners are the most likely to predict this at 68%, followed by Gen Xers at 67%.

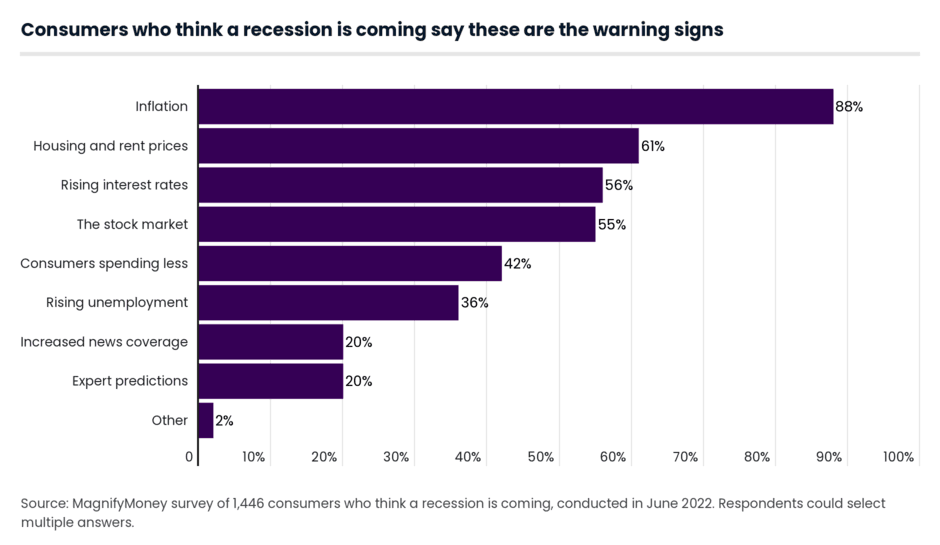

Not surprisingly, inflation is the runaway top choice. Nearly 9 in 10 (88%) of those who think a recession is coming pointed to rising inflation as one of the biggest warning signs.

The other top warning signs include:

Across demographics, baby boomers in particular are most worried about inflation (93%), rising interest rates (67%) and the stock market (60%). Of interest, parents whose children are all 18 or older and six-figure earners are the next most worried about rising interest rates.

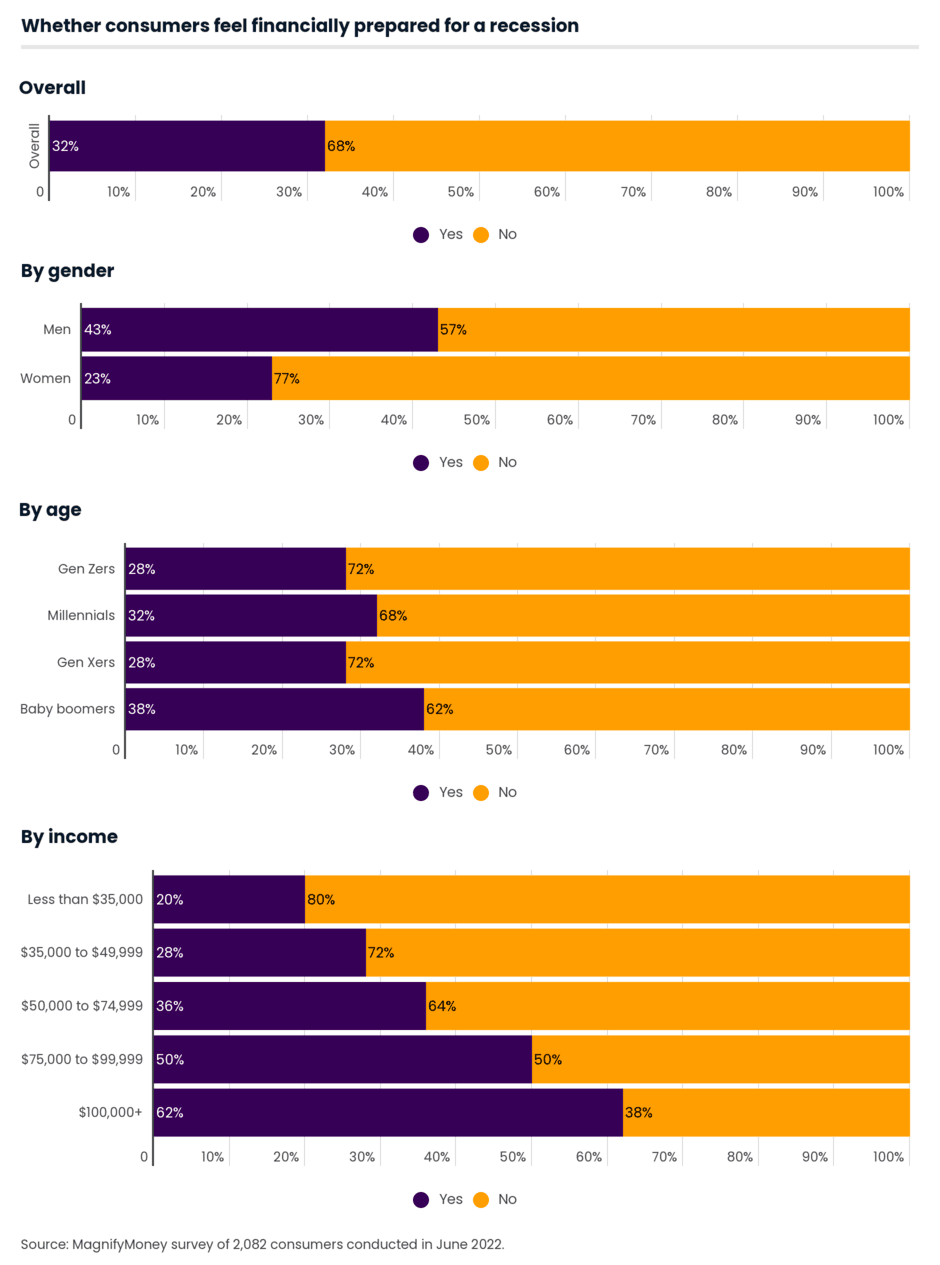

The most troubling fact of this survey: More than two-thirds of Americans (68%) say they don’t feel financially prepared for a recession.

As the high percentage indicates, that feeling is shared among Americans of all different types, though a deeper look shows some folks are far more likely than others to feel this way.

Women are 20 percentage points more likely than men (77% to 57%) to say they’re unprepared. Gen Xers and Gen Zers (both at 72%) are more likely than millennials (ages 26 to 41) (68%) and baby boomers (62%) to say so.

And perhaps not surprisingly, the lower your income, the more likely you are to say you’re not prepared. Eight in 10 (80%) of those making less than $35,000 a year said so, versus 38% of those making $100,000 or more a year.

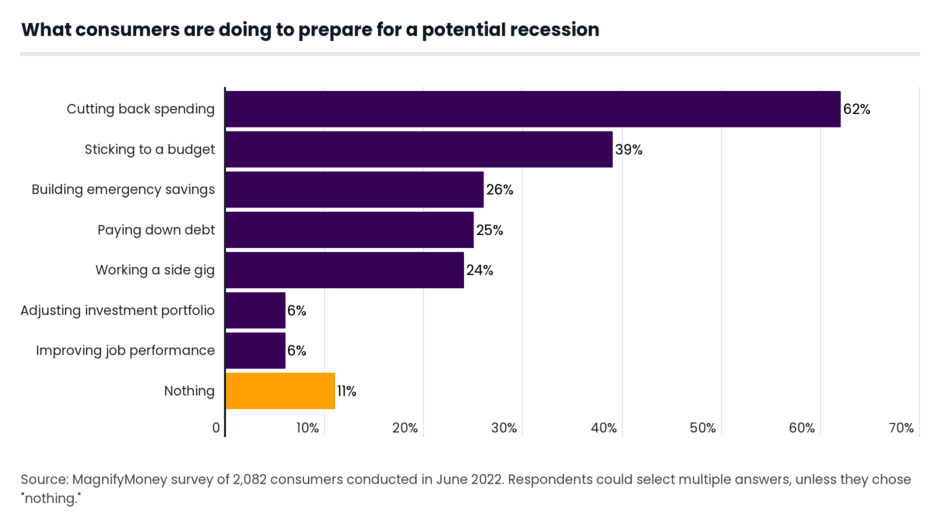

The best news of this survey, however, is that people aren’t just sitting idly by and waiting for a potential recession to hit — they’re acting. Nearly 9 in 10 respondents (89%) say they’ve taken at least one step to prepare for a possible recession.

The most popular response, by far, was that people were cutting back on spending (62%). Others say they’re sticking to a budget (39%), building emergency savings (26%) and paying down debt (25%). About 1 in 4 said they’re getting a side gig to raise extra money.

Across every demographic, including gender, age, income level and parental status, cutting back on spending topped the list. Similarly, sticking to a budget came in second across the board.

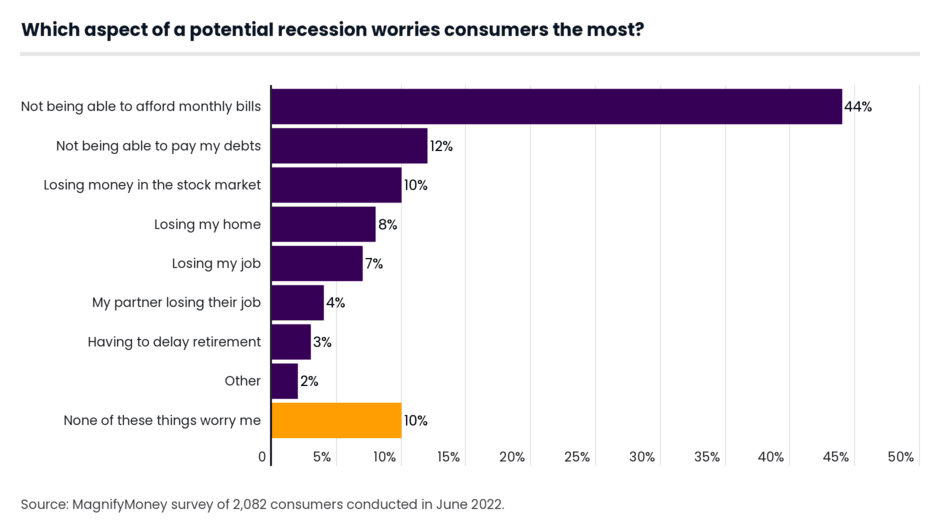

The biggest fear that Americans have of a possible recession is simple: not being able to pay their monthly bills.

More than 4 in 10 Americans (44%) chose that from a list of options of what worried them most if a recession were to come. And this is nearly double as common among those who earn less than $35,000 (54%) versus those who earn six figures (28%).

The overall response — 44% — is three to four times more common than the next most popular options, including not being able to pay their debts (12%) and losing money in the stock market (10%). It makes all the sense in the world because if you’re struggling to pay your bills, little in life is more important than figuring out how to make those ends meet.

Again, it is heartening that Americans are already taking at least some important steps to protect themselves from a possible recession. Here are a few more things you can do to protect yourself in a recession.

Difficult times require difficult choices. Whether you’re prioritizing building your savings, reducing your debt or doing some of both, you may need to make some sacrifices to get there.

That might mean dining out less often or canceling a streaming service or two — or it could mean more dramatic steps. A budget can help you make those choices. (Just don’t forget to update some of those old spending assumptions in your budget. Chances are that inflation might mean they’re not accurate anymore.)

Yes, the Federal Reserve is raising rates like mad, but there are things you can do to reduce the amount of interest you pay on your balances.

A 0% balance transfer credit might just be the best tool to tackle credit card debt, giving you a year or more without accruing any interest on transferred balances. (Just make sure you know about any other rates, fees and deadlines with the card.)

A low-interest personal loan can be helpful, too, especially if your credit isn’t quite good enough for a balance transfer card. Plus, you can also try asking your credit card issuer for a lower interest rate on your cards. A LendingTree survey showed that 70% of those who did so got one, but far too few people ask. (The average reduction was 7 percentage points, which is a big deal.)

Regardless of whether you think a recession is coming, it’s a good idea to have a meaningful emergency fund. While it might not be realistic for many Americans to have three to six months’ worth of income saved in case of an unexpected job loss or medical emergency, the truth is that you probably need more money in savings than what you have.

Having that cushion can make a huge difference to your financial — and mental — health if a recession comes. And the good news is that savings accounts are offering better returns now than they have in a few years — every little bit helps.

Sure, this one can be easier said than done, too. However, it’s never been easier to start a side hustle or find part-time gigs that can help bring in a few extra dollars a month. With inflation running rampant, every extra dollar matters.

Money problems can take a huge toll on virtually all aspects of one’s health and can lead to bigger issues that can make those financial woes even worse. This makes it crucial that you tend to your mental and physical health while you work on your financial health.

And you don’t have to spend a fortune to do so. Devoting regular time to exercising, meditating, reading, watching movies, playing your favorite games or doing whatever healthy activities help you decompress and escape the struggles of daily life (even if only for a few minutes) can make a huge difference to you and your family.

MagnifyMoney commissioned Qualtrics to conduct an online survey of 2,082 U.S. consumers, fielded June 10-14, 2022. The survey was administered using a nonprobability-based sample, and quotas were used to ensure the sample base represented the overall population. All responses were reviewed by researchers for quality control.

We defined generations as the following ages in 2022:

While the survey also included consumers from the silent generation (those 77 and older), the sample size was too small to include findings related to that group in the generational breakdowns.

Matt Schulz

Matt SchulzMatt Schulz is a personal finance expert who has been quoted in or appeared on Good Morning America, NBC Nightly News, the Wall Street Journal, the New York Times and other reputable outlets.

Read More