MagnifyMoney

As the coronavirus pandemic took a hold of the global economy in early 2020, investors everywhere panicked and sent the stock market plummeting to some of its worst days in recent history. Now that some of the immediate panic has subsided, many American investors are reflecting on recent investment moves that they now regret.

In a new MagnifyMoney survey, we found that many Americans regret their previous investing decisions in light of the COVID-19 crisis. However, many investors are also hopeful for the market’s future, which could make this a perfect time to plan your own future investing moves.

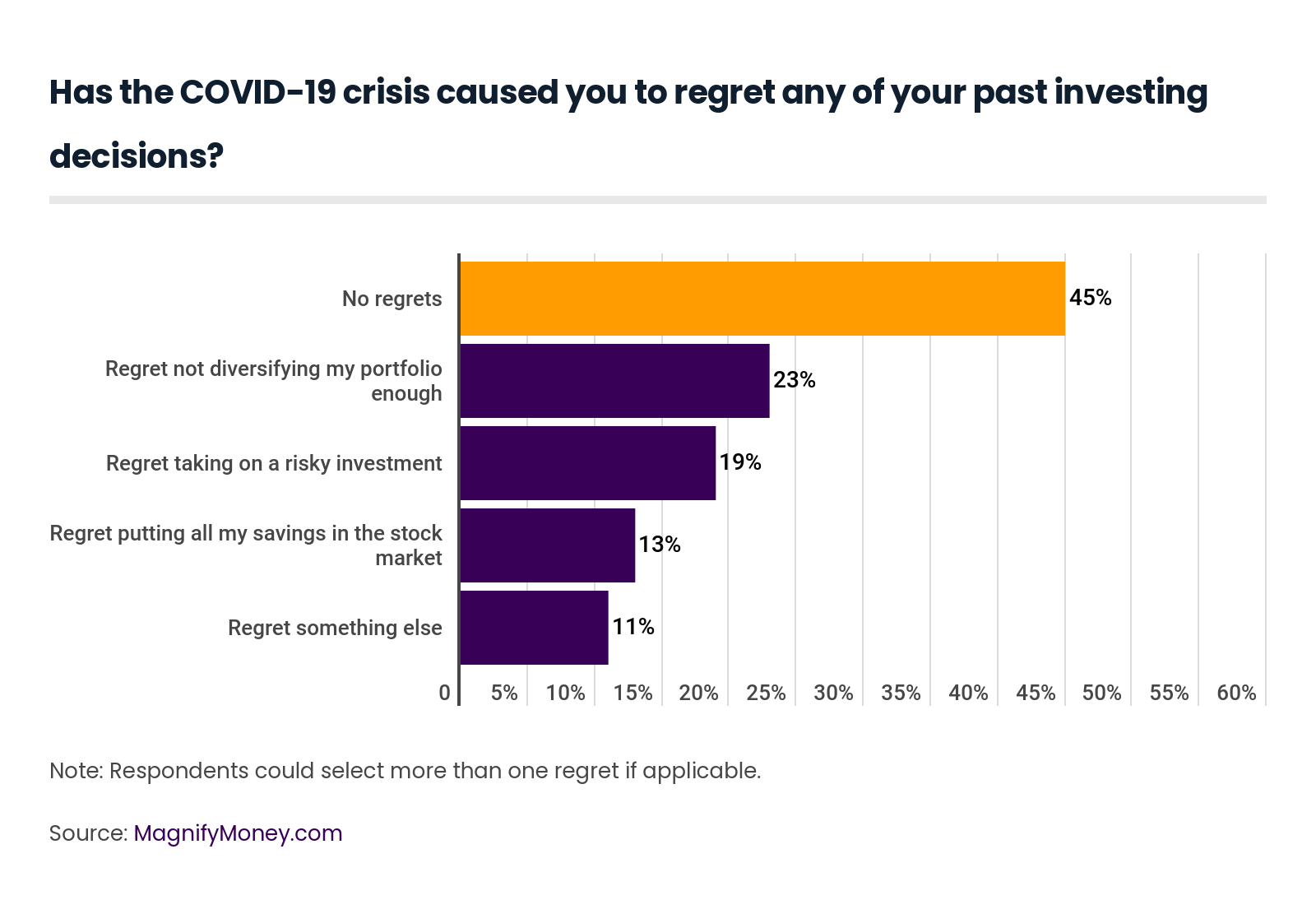

Among our respondents, the top investing regret was a lack of portfolio diversification, a regret cited by 23% of respondents. Gen X respondents regretted this mistake the most at about 29%, with millennials not far behind at 27%. At 30%, men also cited this regret more than the 13% of women who admitted to making this error.

The second most common investment regret cited (19%) was taking on risky investments. Nearly one-third of Gen Z investors got burned by a risky investment. And while baby boomers and the silent generation were less likely to make this mistake, a quarter of Gen X confessed regretting this potentially costly move.

Some examples of high-risk investments can include initial public offerings (IPOs), structured products and venture capital trusts. You also may take on considerable risk if you’re trying to time the market for maximum returns, which many experts caution against.

The third common investment regret among respondents (13%) was keeping all of their savings in the stock market. Gen Z investors were the most guilty of this mistake, with 27% regretting keeping all of their savings in investments, followed by 15% of millennials, 13% of Gen X, 7% of baby boomers and a mere 2% of the silent generation.

Luckily, these investing regrets are easily avoidable. Even if you found yourself regretting your pandemic-induced investment moves, there’s still time to recover.

For starters, it’s important to keep your assets diversified, or spread among different investments and across industries, whether you’re a beginner or an investing veteran. That way, when one part of the market takes a tumble, the other parts of your portfolio aren’t hit as badly, or at all. Essentially, by avoiding putting all of your eggs in one basket, your investments can be better protected in a downturn.

Keeping your portfolio well-balanced and diversified can also help mitigate risky investments that you might have taken on. It also helps to invest your money incrementally rather than in lump sums. That way, you’ll invest in both down and up times, balancing out your investment gains rather than going all in now and regretting your risk-taking later.

Acting reactively to the market is also a risk of its own. If you sell your assets just because everyone else is panicking, prices are driven down and you end up losing money because you’re making less on the sale than what you paid when you bought the asset. Instead, ride it out and keep your money invested. The markets will recover, and your assets’ valuation will go back up, too.

Due to its nature, investing is a risky business. There’s the chance of losses and there is no guaranteed payout amount waiting for you. Because of these factors, it’s generally a bad idea to place all your savings bets on your investments. If you need cash in a downturn, you’ll be selling at a loss to withdraw from your investment accounts. Even further, selling off assets and turning them into cash takes time, making this a much less convenient method of withdrawing money than, say, heading to the ATM.

Instead, you should keep your investments geared toward the future, establishing more long-term goals for your investment accounts. This is why retirement accounts are often investment-based — it gives your investments time to accumulate, but also to ride out the many fluctuations of the market.

For your more immediate cash needs, keep money in a high-yield savings account. This allows for easier withdrawals and transfers, and ensures your money still grows. You can also open an interest-bearing checking account to make sure your money is growing no matter what account it’s in.

MagnifyMoney commissioned Qualtrics to conduct an online survey of 2,008 Americans, with the sample base proportioned to represent the overall population. The sample population included 1,183 investors and 866 non-investors. We defined the generations in 2020 as follows:

The survey was fielded from April 28 to May 1, 2020.

Lauren Perez

Lauren PerezLauren Perez is a former writer at MagnifyMoney who covered deposit accounts and Federal Reserve meetings. Prior to joining LendingTree, she was a personal finance writer for SmartAsset. She has a B.A. in English from the University of Rochester.

Read More