MagnifyMoney

Almost 70% of Americans are feeling frustrated that the money they’re saving isn’t growing, according to a new MagnifyMoney survey of more than 1,000 consumers.

DepositAccounts founder Ken Tumin says it’s likely the Federal Reserve will keep its benchmark interest rate near zero for several years, which means Americans’ frustration with low annual percentage yields (APYs) will continue.

“We are unlikely to see significant improvement in savings account rates until after the Fed starts hiking rates,” he says.

About 7 in 10 consumers say they feel frustrated that the money they’re saving isn’t growing, and younger consumers are especially likely to express this sentiment.

Only 5% of consumers are earning an APY between 0.50% and 0.99% and 8% are earning an APY of 1.00% or higher through their primary savings account, though the best high-yield online savings accounts average an APY of 0.55%.

These rates may sound low, but more consumers are earning even less interest. In fact, 18% say they’re earning an APY of less than 0.05%, which is below the national average APY of 0.06% for savings accounts, according to the Federal Deposit Insurance Corp. (FDIC).

While the majority of consumers are aware of how much interest they’re earning, 34% admit they have no idea how much interest their bank pays them. The more money you make, the more likely it is that you know how much interest you’re earning on your savings. A little more than half (52%) of those making less than $35,000 have no idea, compared with 19% of those making $100,000 or more.

When choosing the best savings account for you, Tumin recommends looking past the current rate. “Promotional rates from banks are common, especially when banks launch new online divisions,” Tumin says. “Rates may be above average for several months, but after one or more years, few banks will be able to maintain above-average rates.”

If your savings account is at a brick-and-mortar bank, Tumin believes the easiest thing to do to earn more interest is to open a savings account at an online bank.

Online savings accounts can be easily opened and linked to your existing checking account. You don’t have to switch banks, as the link makes it easy to electronically transfer funds between the two accounts.

If you prefer to bank locally, Tumin suggests looking for community banks and credit unions that offer high-yield checking accounts. These accounts allow you to earn interest rates that are often higher than the rates with online savings accounts.

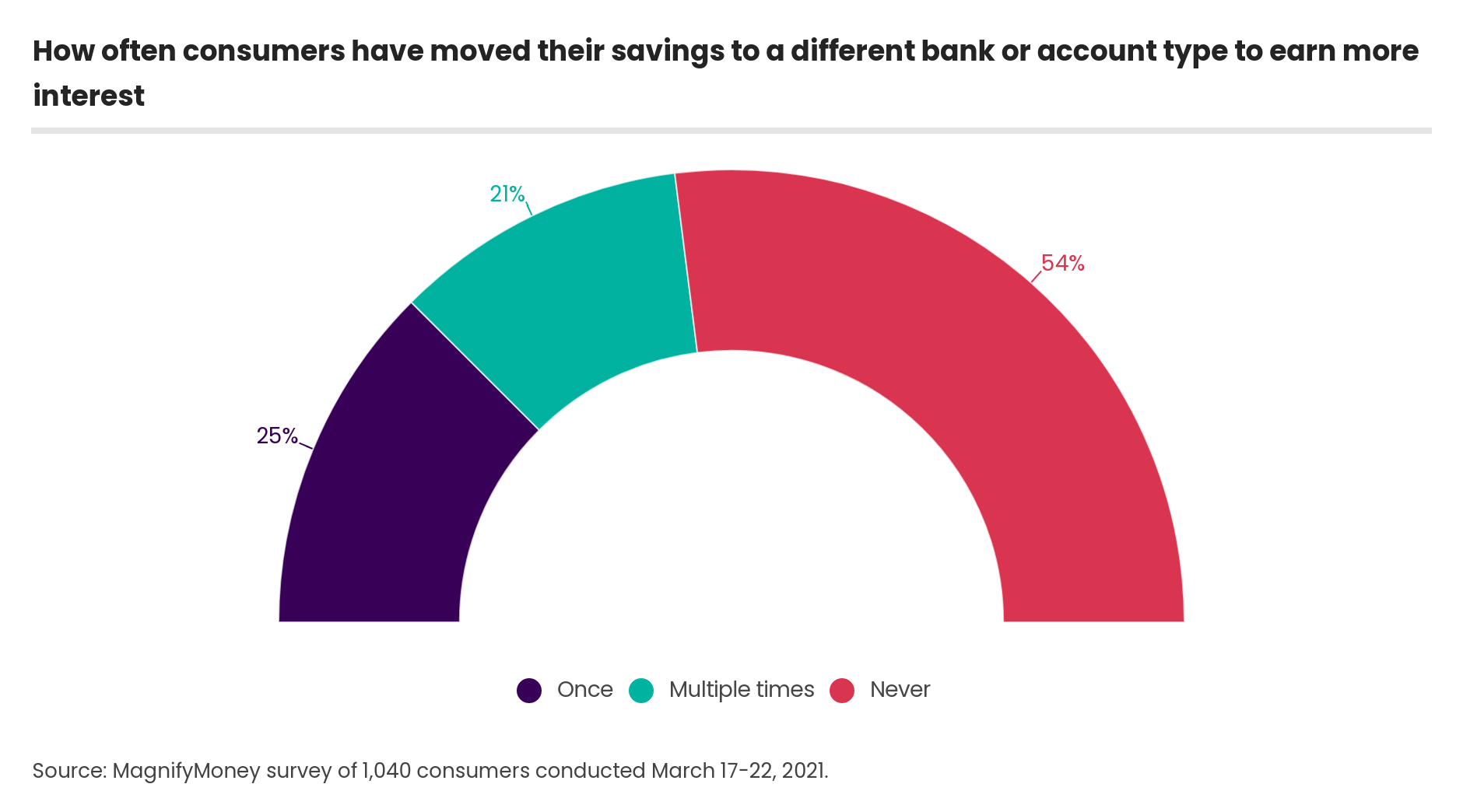

Frustration surrounding low savings APYs may be driving consumers to switch banks. At some point, 46% of consumers have switched to a different bank or account type to earn more interest.

Gen Zers (ages 18 to 24) appear most savvy when it comes to doing this, as 66% have changed banks to earn more interest — about half of which have done so more than once.

That’s followed by millennials (ages 25 to 40) at 56%. On the other hand, older generations are more stuck in their banking ways, as just 37% of baby boomers (ages 56 to 75) and 36% of Gen Xers (ages 41 to 55) have switched banks to earn more interest.

Reasons for switching banks: It’s important to note that MagnifyMoney’s question focused specifically on consumers changing banks to earn more interest. It didn’t address other reasons for switching banks, from poor customer service to high fees to a lack of ATMs.

There also appears to be a gender divide when it comes to jumping ship, as more men have changed banks for better interest rates than women (52% versus 39%). Separately, the more money consumers make, the more likely they are to switch banks (65% for those who earn $100,000 or more versus 26% for those who earn less than $35,000).

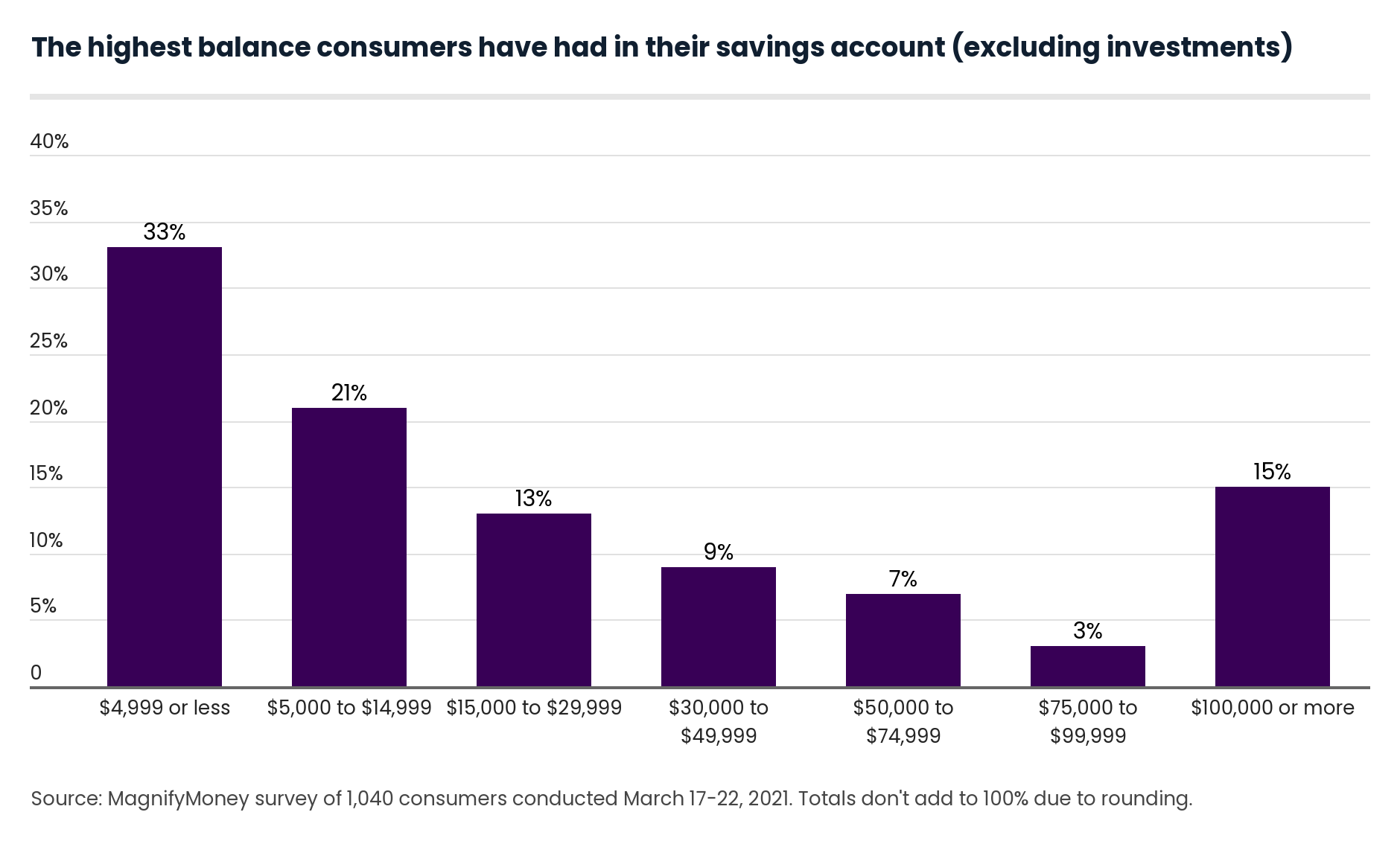

The MagnifyMoney survey also examines how Americans save in general, showing 1 in 3 Americans have never had $5,000 in their savings account, and just 15% of consumers have saved $100,000 — excluding any investments — at some point.

That percentage jumps to 25% for baby boomers who are more established in their careers and financial lives. However, high salaries don’t guarantee high savings rates. Even those who make $100,000 don’t always have that amount in their savings — only 33% of the highest earners say it’s the highest balance they’ve ever saved.

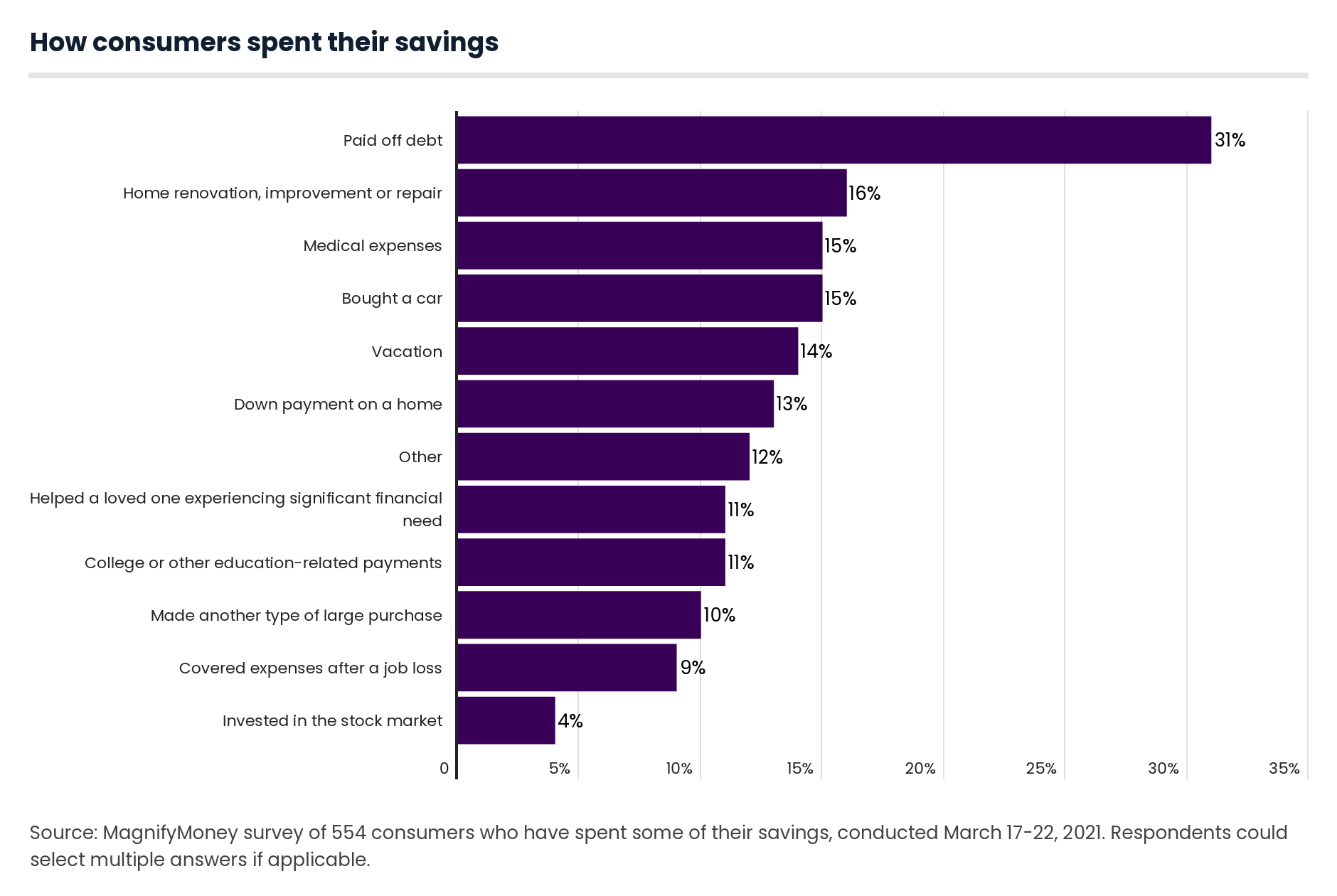

Current spending needs may be outweighing savings goals. In fact, 53% of consumers say they’ve spent some of their savings, so their current balance is less than their highest balance. Despite that, 47% say their current balance is their highest balance.

For those who say their current balance is not their highest balance, nearly a third (31%) used some of their savings to pay down debt and 16% funded home renovations, improvements or repairs.

Job loss: Almost 1 in 10 utilized their savings to help cover expenses after a job loss. High rates of job loss and pay cuts during the coronavirus pandemic may be forcing many to use their savings to cover day-to-day expenses.

“It’s good that consumers are using savings to pay off debt since that will save many from paying interest on their debt, which is often at a very high rate compared to the rates of savings accounts,” Tumin says.

However, he noted that the downside is that it indicates that many people aren’t saving first for short-term goals and expenses.

MagnifyMoney commissioned Qualtrics to conduct an online survey of 1,040 U.S. consumers from March 17-22, 2021. The survey was administered using a non-probability-based sample, and quotas were used to ensure the sample base represented the overall population. All responses were reviewed by researchers for quality control.

We defined generations as the following ages in 2021:

While the survey also included consumers from the silent generation (defined as those 76 and older), the sample size was too small to include findings related to that group in the generational breakdowns.

Jacqueline DeMarco

Jacqueline DeMarcoJacqueline DeMarco is a freelance writer who is particularly passionate about finance. She began her career in the retirement industry. Today, she works with more than a dozen financial brands to create entertaining and educational money content.

Read More