MagnifyMoney

The good news about living paycheck to paycheck: You are earning paychecks. The bad news: There’s nothing left over after your expenses are paid, which can be earth-shattering if those paychecks stop coming.

That’s the reality for many Americans, though, as 50% of working Americans report living paycheck to paycheck, according to the latest MagnifyMoney survey of 2,100 people.

While people in lower income brackets are most likely to live paycheck to paycheck, results show that this also affects a sizable portion of those in higher income brackets. To break the cycle, experts say establishing an emergency savings fund should be a priority for all Americans — though it’s not a quick fix.

Among American workers surveyed by MagnifyMoney, only 35% say they don’t live paycheck to paycheck. That leaves 50% who do — and 15% who say it varies.

Perhaps surprisingly, even a high percentage of earners in the highest salary range — $100,000 a year or more annually — live paycheck to paycheck (31%). And though that’s significantly less than the 76% of those earning less than $35,000 who live paycheck to paycheck, it is still considerable.

Meanwhile, age doesn’t seem to have too much impact on whether people live paycheck to paycheck, with one notable exception. Baby boomers (ages 57 to 76) have a relatively small portion — 34% — reporting they live paycheck to paycheck, while between 52% and 53% of Gen Zers (ages 18 to 25), millennials (ages 26 to 41) and Gen Xers (ages 42 to 56) do.

Still, no matter who you are, it’s not an ideal financial situation.

“Living paycheck to paycheck often translates into a lot of uncertainty,” says Ismat Mangla, MagnifyMoney executive editor. “How will you pay for an unexpected emergency? What do you do if your income is suddenly affected? Not having a cushion can add a lot of stress to Americans’ lives. The pandemic has just exacerbated the stress because of so much uncertainty when it comes to jobs and health situations.”

So, what if Americans found themselves going from paycheck to no check? Things could get pretty difficult pretty quickly, as 67% of Americans say they couldn’t pay all their bills if their paychecks stopped.

Consumers who would be most likely to miss bill payments include:

And there are some pretty important bills at stake. Nearly 4 in 10 working Americans (39%) say they couldn’t pay their rent or mortgage without their next paycheck. Electricity, internet and other utility payments would be on the line for 33% of working Americans, while 33% also report that they wouldn’t be able to pay their phone bill.

Gen Zers are most likely to be unable to afford their housing payments if they lose their paychecks — 45% of them report this, compared with:

As alarming as these percentages may be, the proportion of people living paycheck to paycheck has actually decreased slightly since a 2019 MagnifyMoney survey found 53% of respondents were living paycheck to paycheck.

In addition, the percentage of people who say they wouldn’t be able to pay all their bills if they lost their paycheck also slightly decreased — from 70% in October 2019 to 67% this year.

Plus, housing may be a bit more secure now, too: In 2019, 44% said that they wouldn’t be able to make their rent or mortgage payment if their paychecks stopped, compared with 39% this year.

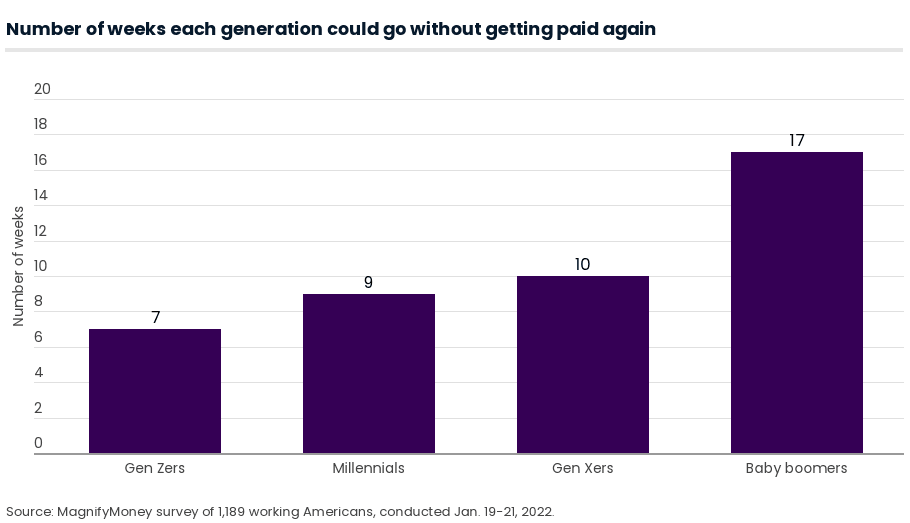

Overall, in the new version of the survey, respondents say they could go 10 weeks without getting paid and still pay their bills.

Baby boomers report being able to go the longest without pay — an average of 17 weeks, which is up several weeks from the 14 reported in 2019. Baby boomers are followed by:

And with the COVID-19 pandemic continuing to affect many people, nearly 45% of Americans — regardless of whether they’re working or not — say they’ve had to skip paying at least one bill they couldn’t afford since March 2020.

If you ever find yourself unable to pay a bill, Mangla says you should immediately see if you can negotiate an alternative payment plan.

“Many vendors would rather get paid something or get on a schedule than get nothing at all,” she says. “Focus on paying the most important bills first — the ones that keep a roof over your head and food on the table. You also want to try to at least make minimum payments on credit cards so that you don’t become delinquent or impact your credit further.”

Overall, the paycheck-to-paycheck life takes a far greater toll on women than men. First, there’s the fact that a smaller proportion of men live paycheck to paycheck — 42%, versus 59% of women.

And even if men were to lose their next paycheck, they’d have fewer issues paying their bills — 38% say they could still pay all their bills, versus 28% of women. On the bills front, women are more likely than men to report their housing payments would be at stake — 45% versus 33%. The same is true with utility bills — 42% of women, versus 25% of men.

Men could pay their bills for far longer, too — men say they could go 13 weeks without a paycheck, while women say they could only go seven weeks. This compares to 11 weeks for men and eight weeks for women in the 2019 survey.

However, the disparity isn’t as large when it comes to the percentage of people who say they skipped paying at least one bill they couldn’t afford since the pandemic began — 47% of women, versus 42% of men.

The cost of living paycheck to paycheck often comes at the expense of one’s mental well-being. More than 7 in 10 Americans (71%) say they’re “constantly stressing” that they don’t have enough money saved for emergencies, with women (75%) feeling the stress more than men (66%).

Those in the lowest income bracket are the most stressed, with 85% who earn less than $35,000 affirming that. But those in the highest income brackets aren’t immune — 48% of those making $100,000 or more say they face constant financial stress.

That stress is likely because so few Americans have the security of an emergency savings fund. Less than 50% — 46%, to be exact — report having saved an amount equal to at least three months of living expenses.

Again, men are in better shape here: 55% of them report having at least three months of living expenses saved, versus 39% of women. Baby boomers are the most likely to (58%), but Gen Zers are more likely to (48%) than Gen Xers (42%) and millennials (40%).

So, what if a moderately expensive car repair or medical expense came up: Could Americans cover that?

When asked if they would have enough money in their accounts to cover a $1,000 emergency, or if they’d have to take on debt or borrow from loved ones for it, 47% report the latter. And, continuing the trend, more men than women say they could cover such an emergency with money in their accounts — 64% versus 44%.

So, is there a way to stop the stress and move beyond the paycheck-to-paycheck lifestyle? In most cases, there’s no quick fix. Rather, it’s a series of deliberate choices and discipline over time that can provide a cushion if those paychecks stop — here are some tips:

“Something is better than nothing,” she says. “Start by socking away whatever you can — even 10 bucks a week is better than nothing.”

MagnifyMoney commissioned Qualtrics to conduct an online survey of 2,100 consumers on Jan. 19-21, 2022. The survey was administered using a nonprobability-based sample, and quotas were used to ensure the sample base represented the overall population. All responses were reviewed by researchers for quality control.

We defined generations as the following ages in 2022:

While the survey also included consumers from the silent generation (those 77 and older), the sample size was too small to include findings related to that group in the generational breakdowns.

Julie Ryan Evans

Julie Ryan EvansJulie Ryan Evans is a writer and editor who has covered small business, real estate and personal finance for nearly a decade. She has written for an array of publications, including USA Today, Realtor.com, LendingTree and Debt.com.

Read More