MagnifyMoney

The coronavirus pandemic is affecting Americans’ retirement savings in distinct ways. Some people are able to funnel more into their retirement accounts since they’re spending less on things like travel and dining. Others have had to put savings on the back burner or even tap into their retirement savings plans to cover living expenses due to lost income.

To get a sense of the retirement savings landscape, MagnifyMoney surveyed more than 1,200 working Americans, finding that 17% of those who work for employers that offer retirement plans don’t currently contribute. Among working Americans who do contribute, 12% leave company matching funds on the table.

Not every employer offers a retirement savings plan, but the majority do. Of the 1,200-plus workers surveyed by MagnifyMoney, 59% say their employer offers a retirement saving plan, while 34% say their employers do not. A head-scratching 7% say they don’t know if their employer offers one. (Quick, check with your human resources — HR — department!).

Those with higher annual household incomes are more likely to work in jobs with employer-sponsored retirement savings plans — 78% among those with incomes of $100,000 or more, versus 41% among those with incomes below $35,000. And so are men — 64%, versus 56% of women.

Of interest: Among respondents whose employers offer plans, 83% say they’re currently contributing to theirs, while 12% have contributed to it in the past but aren’t doing so currently. Lastly, 6% have never enrolled in their company’s retirement savings plan.

Not contributing to a plan is one thing, but not contributing to a plan in which the employer offers matching funds is a whole other thing. Matching is when an employer “matches” your contributions to your 401(k) or other retirement plan up to a certain amount.

In some cases, it’s a dollar-for-dollar match, while it’s a partial match in others. Either way, it’s free money for the taking. Yet our survey finds that about 1 in 10 American workers (12%) are leaving it right there on the table.

“If your employer offers to match a certain amount of your retirement contributions, that’s a part of your total compensation package,” says Ismat Mangla, MagnifyMoney senior content director. “Matching contributions from your employer will help you save and invest more for retirement. If you don’t contribute enough money to get your employer match, you are literally leaving free money on the table — money that belongs to you and is part of your compensation. Don’t forfeit it!”

While employees have to do their part (i.e., contribute), many also wish their employers would step up their retirement plans. For example, 49% wish their employer contributed more, 25% wish they’d offer more educational resources, 8% wish their employer provided a different provider and 6% wish their employer provided a different plan type. Less than one-quarter of respondents say there’s nothing they would change about their employer’s plan at all.

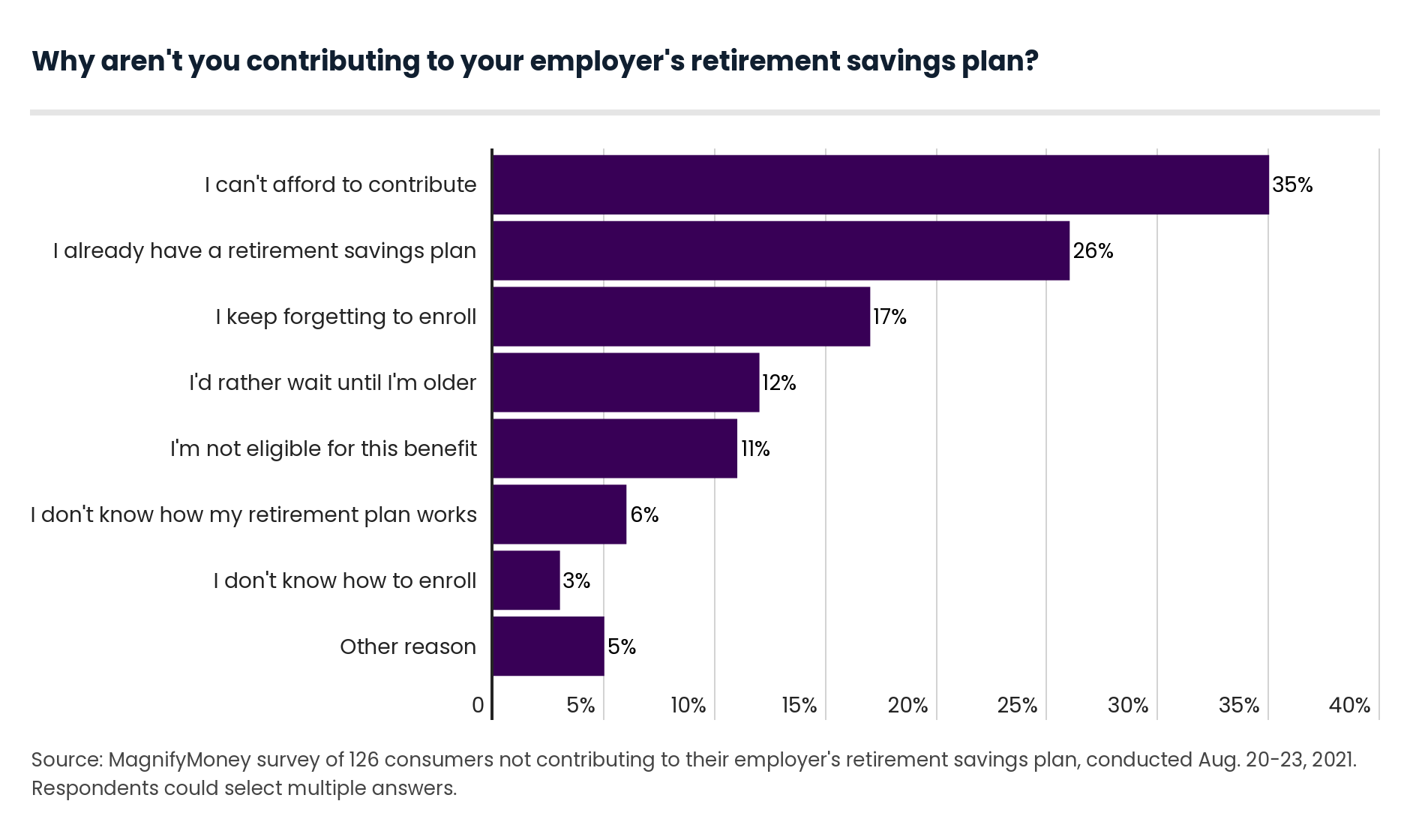

The reasons people don’t contribute to their employer-sponsored retirement plans vary, though money is the most common.

In fact, 35% of respondents say they can’t afford to contribute to their plan. Other top explanations include having another retirement plan (26%), forgetting to enroll (17%) — set a reminder now — and preferring to wait until they’re older to contribute (12%).

Do people know what they may be leaving on the table? In most cases, yes. Of those not contributing to their retirement plans, 62% say they know their employer offers matching funds, while 17% say they don’t know if they do.

Women are less likely to know if their employer offers matching funds than men — 20% versus 12%. And somewhat surprisingly, it’s the older generations — 31% of Gen Xers (ages 41 to 55) and 29% of baby boomers (ages 56 to 75) — who are less likely to know than the younger generations — 14% of Gen Zers (ages 18 to 24) and 13% of millennials (ages 25 to 40) — whether their employer offers matching funds.

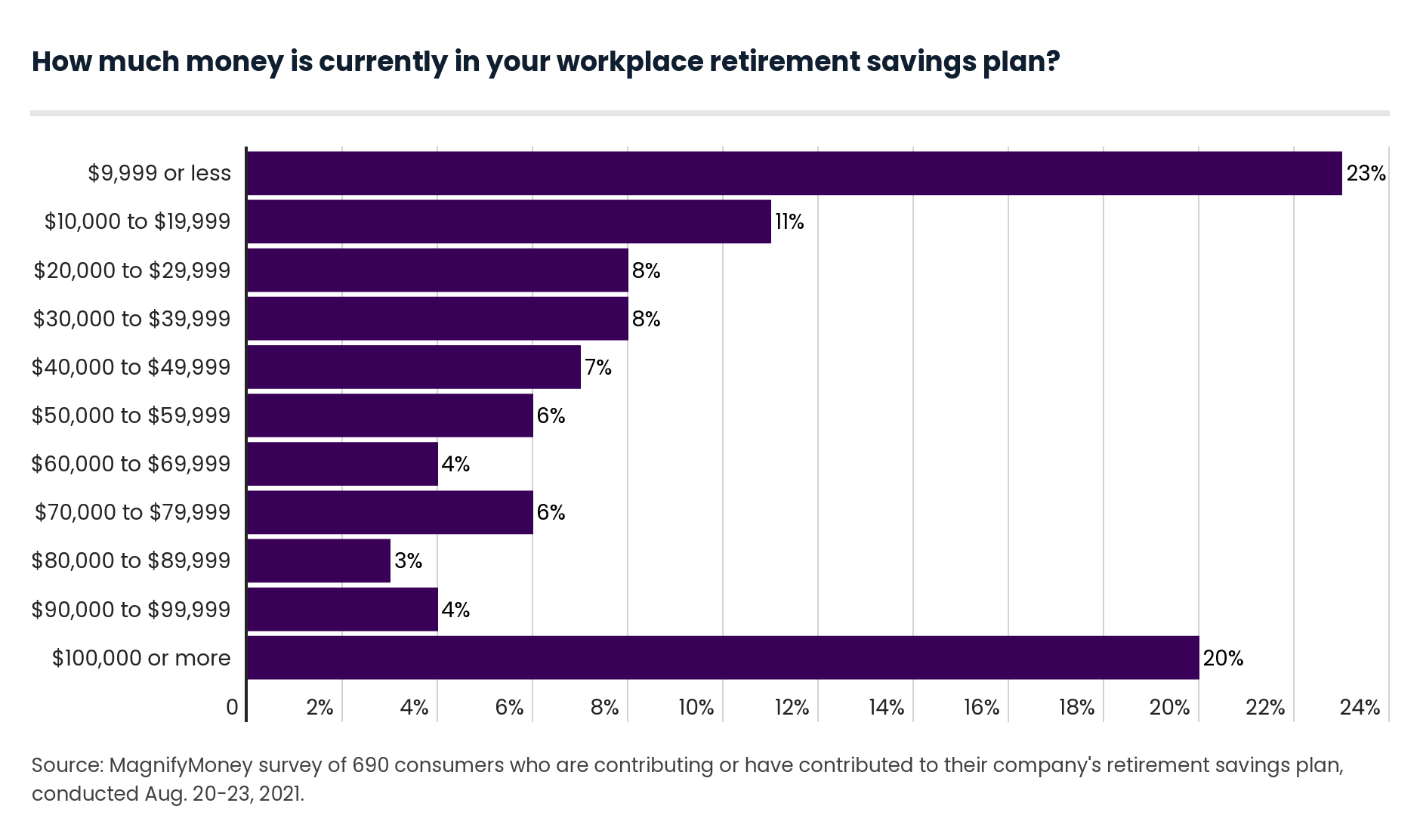

So, of those who are saving, are they saving enough to make their golden years golden? While the amount people need to save for retirement varies, respondents overall report retirement plan balances that aren’t brimming.

Just 20% of respondents say their employer-sponsored retirement plan balances have reached $100,000 or more, with significantly more men (30%) than women (11%) in this category.

“It’s no secret that Americans are behind on saving and investing enough money for retirement,” Mangla says. “Women may feel even less confident about investing.”

And older generations are, understandably, more likely to have higher balances in their retirement accounts. In fact, 48% of baby boomers and 31% of Gen Xers have balances of $100,000 or more, versus 9% of Gen Zers and millennials. But still, that means more than 50% among both of the older generations have yet to reach the $100K mark.

The good news is that some have other retirement savings besides their employer-sponsored plan. In fact, 58% of respondents report having at least one other account, such as an individual retirement account (IRA). However, that means 43% only have one account.

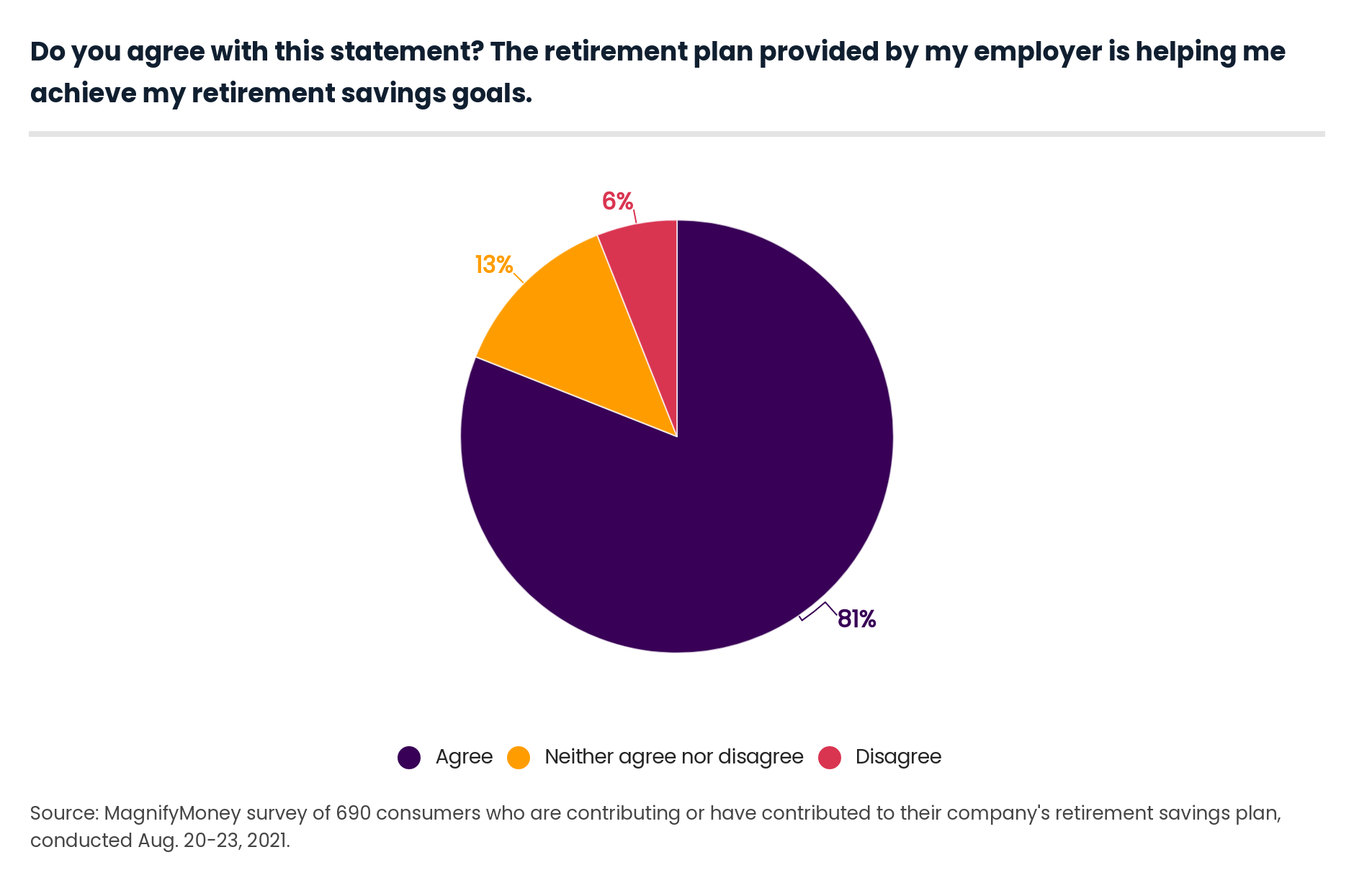

While, as mentioned earlier, there are changes employees wish their employers would make in regard to the retirement plan they offer, workers are generally happy with the benefit. When asked if they agree their employer is helping them meet their retirement goals, 81% either agree or strongly agree. Just 6% disagree or strongly disagree, while the rest are neutral.

There’s quite a bit of blind faith when it comes to employer-sponsored retirement plans. While those saving for retirement get a financial gold star, many would fail a test about how exactly they’re doing so. Less than half of respondents (43%) say they know what’s in their retirement plan in terms of the stocks and funds in which they’re investing. This is particularly true for women, with just 30% stating they know what’s in their plan, versus 57% of men.

Retirement savings roadblocks often come with a change in jobs. While most report rolling their account balances into a new account or leaving them in the existing one when they switched employers, 33% report withdrawing the funds or doing something else with them.

That may feel like a nice windfall at the time, but it’s a windfall that typically comes with tax penalties, and the vast majority of those who withdrew funds — 71% — say they regret it.

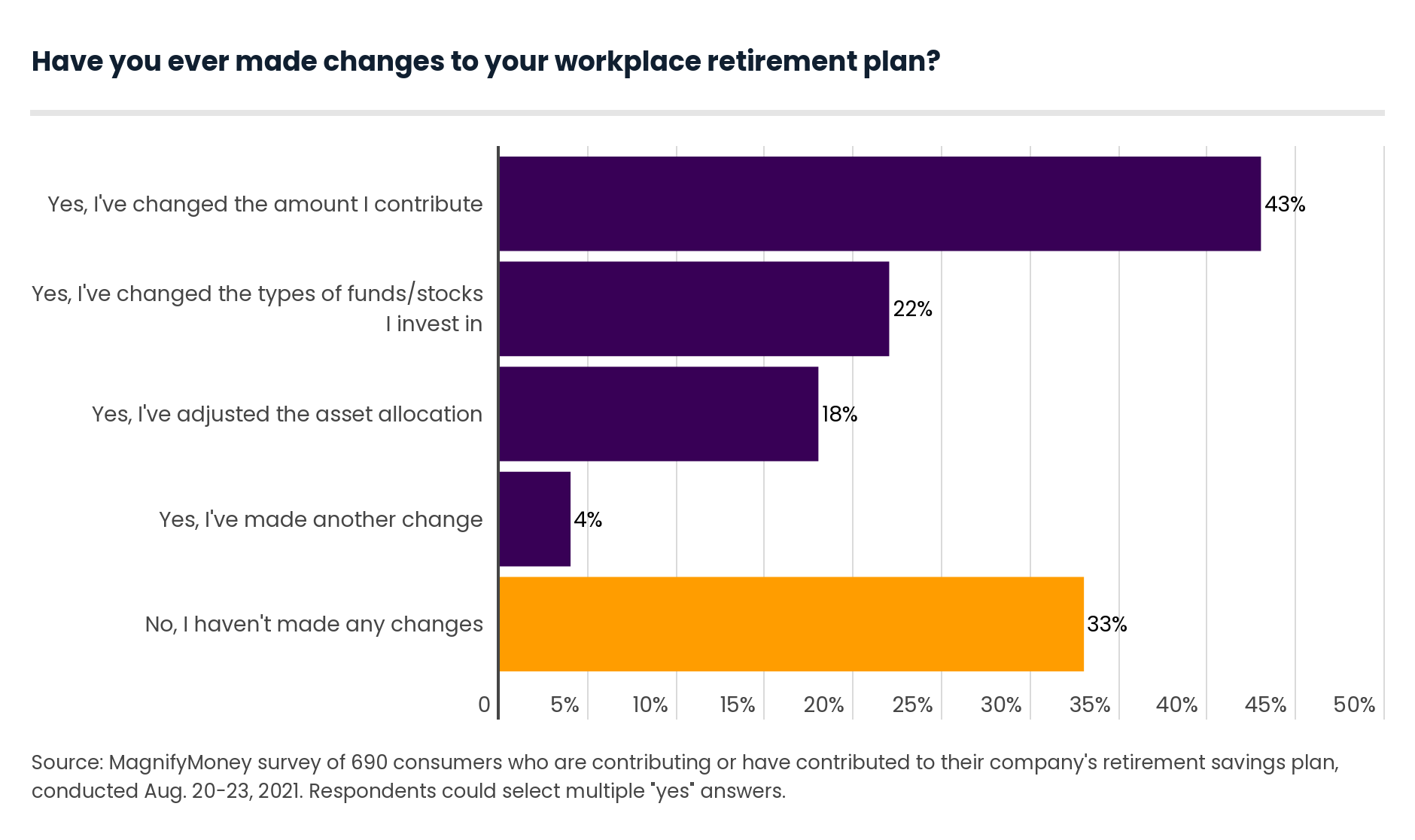

Even if you’ve made mistakes in the past or you want to adjust how much you contribute and where those contributions go, you can make changes to your workplace retirement plan. In fact, most experts say you should make changes to your plan throughout the years as the default contribution amount is generally not enough for people to reach their goals. However, nearly one-third of plan participants say they’ve never made changes to their plans.

Mangla suggests that people take a look at their plan at least once a year. She encourages taking advantage of any company matching and making sure the money in your account is invested in low-cost index funds.

She also suggests that each year you try to increase your contribution by a certain amount, such as a percentage point, up to the maximum amount. In 2021, you can contribute up to $19,500 in a 401(k). Beyond that, however, she says, set it, forget it and let the magic of compound interest do its work.

MagnifyMoney commissioned Qualtrics to conduct an online survey of 1,233 U.S. consumers who are currently employed, from Aug. 20 to 23, 2021. The survey was administered using a nonprobability-based sample, and quotas were used to ensure the sample base represented the overall population. All responses were reviewed by researchers for quality control.

We defined generations as the following ages in 2021:

While the survey also included consumers from the silent generation (76 and older), the sample size was too small to include findings related to that group in the generational breakdowns.

Julie Ryan Evans

Julie Ryan EvansJulie Ryan Evans is a writer and editor who has covered small business, real estate and personal finance for nearly a decade. She has written for an array of publications, including USA Today, Realtor.com, LendingTree and Debt.com.

Read More