MagnifyMoney

Stock market declines can be scary for both novice and experienced investors. Everybody loves it when markets are climbing to new highs session after session; however, it’s the stomach-churning declines that test your nerves. A new survey from MagnifyMoney finds that for many retirement investors, even a minor dip in the market makes them want to quit.

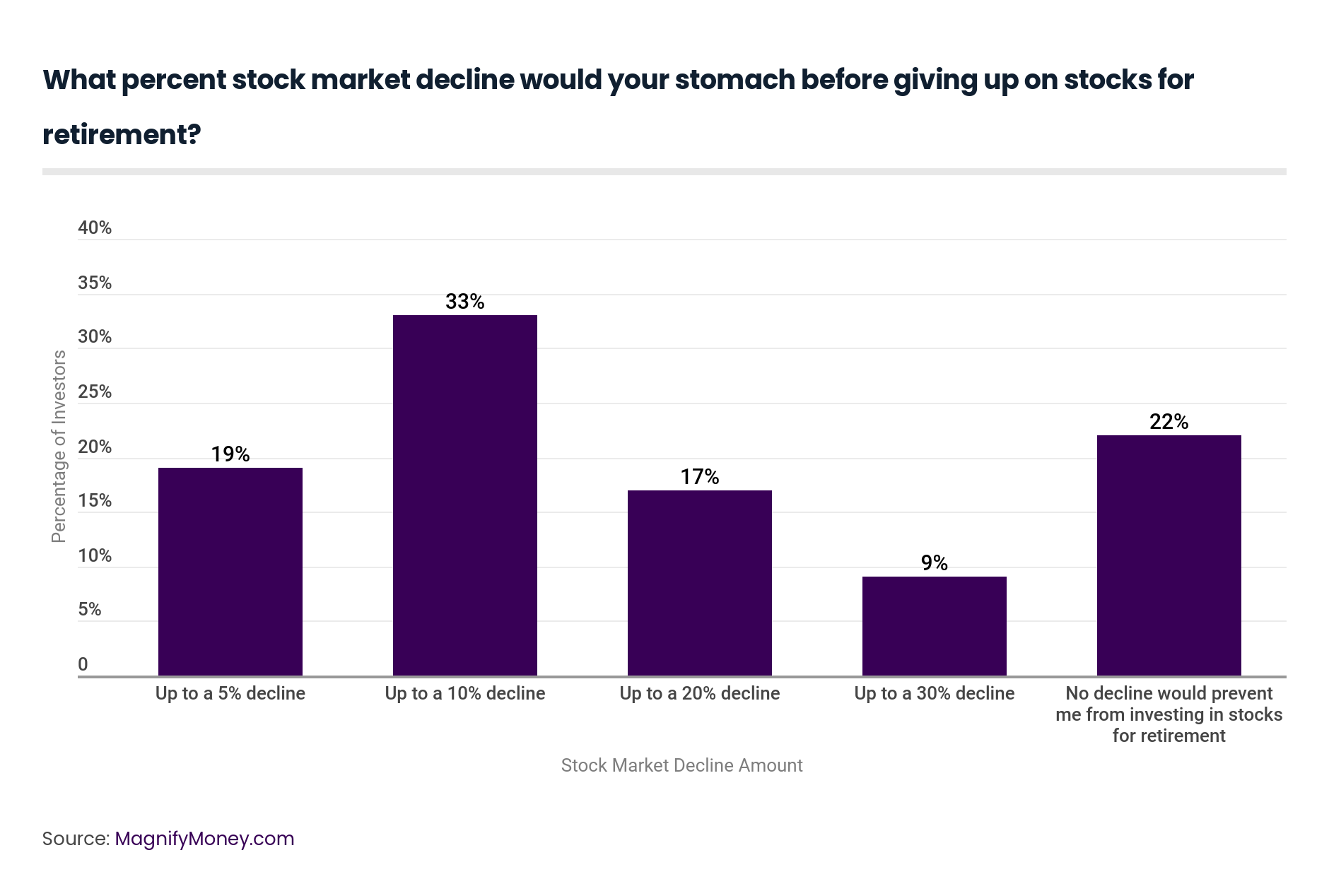

Our survey of over 700 Americans asked one simple question: How large a percent decline in the stock market would compel you to give up on stocks for retirement? The results were surprising: 19% of people would abandon the stock market after just a 5% drop. Seasoned investors know that declines in the stock market are par for the course when it comes to investing.

The idea of risk tolerance is a core concept for investing in the stock market. An investor’s tolerance for risk helps dictate how they invest, where they invest and the assets they choose to invest in.

But let’s be clear about what we mean by risk: the risks you take when you do extreme sports or gamble in Las Vegas are quite different from the risks involved with investing. Another way to refer to risk in the context of the stock market is volatility, or how often and how much a given stock or stock index rises or falls over a set period of time. Your ability to prepare for volatility and learn to cope with it goes a long way to determining how much tolerance you have for risk.

It’s important to remember that ups and downs of the market are normal, and that market corrections — when a stock market drops 10% or more from its most recent high — happen every two to three years. Over the longer term, factoring in all the corrections, the S&P 500 has an annual rate of return of around 10%.

This is why you frequently read that younger investors can take on more risk than older investors — because they have more time to ride out the lows and wait for the inevitable arrival of fresh highs. Viewed over a longer timescale, younger investors can handle bigger swings in the market.

But your tolerance for market volatility is not just based on your age and investing timeframe, though — one key contributing factor to your overall risk tolerance is just how much you can emotionally handle. So, if the market dips 10% in any given month, would you take your money out of the market? Or ride it out? Our survey aimed to find that out.

Our survey found that overall, most people can’t stomach even a 10% market decline. In fact, 19% of respondents said that when it comes to their retirement savings, they could only stomach up to a 5% decline in the stock market before giving up on stocks. Meanwhile, 33% said they could handle only up to a 10% market decline before abandoning stocks for retirement.

Others, though, indicated they had higher tolerance for volatility. Our survey found that overall, 17% of respondents said they could handle up to a 20% decline in the market before giving up on their stocks for retirement, while 9% said they could stomach up to a 30% dip in the market before giving up. Overall, 22% responded that there was no decline in the stock market would prevent them from keeping their stocks for retirement investing. If you need advice in investing in stocks read our review here.

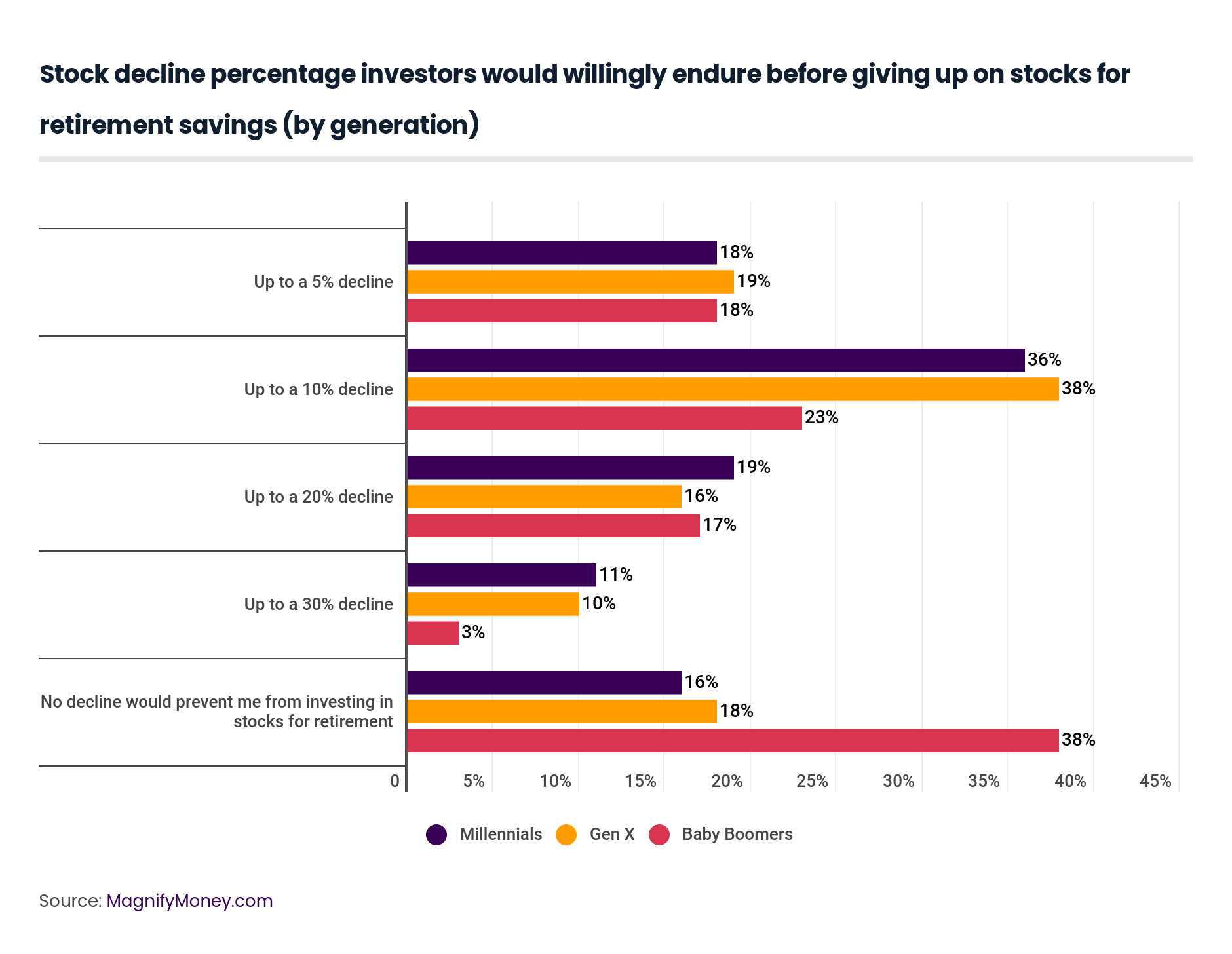

Overall, our survey found that different generations can stomach vastly different levels of stock market risk. That makes sense, considering that age and your investing time horizon can play a big role in your overall risk tolerance.

The survey suggests that baby boomers have the highest tolerance for stock market declines. This bucks the notion that younger investors should have higher risk tolerance because they have a longer time horizon. But this makes sense when you consider that many baby boomers are more likely to be seasoned investors, with a better grasp on investing concepts like the ability of the market to bounce back after market corrections and how downturns are a normal part of the investing cycle.

Overall, 38% of baby boomers said no amount of market decline would cause them to give up on stocks in their retirement plan, compared to only 18% of Gen Xers and 16% of millennials.

For baby boomers, 18% could handle up to a 5% decline in the stock market, 23% could handle up to a 10% dip, 17% could handle a drop up to 20% and 3% could handle up to a 30% decline.

Gen X had similar results, with 19% being able to stomach up to a 5% decline, 38% up to a 10% decline, 16% up to a 20% decline and 10% up to a 30% decline in the stock market. Millennials weren’t much different, either, with 18% being able to handle up to a 5% dip in the market before abandoning stocks for their retirement, 36% could handle up to a 10% drop, 19% could handle up to a 20% dip and 11% could deal with up to a 30% drop in the market.

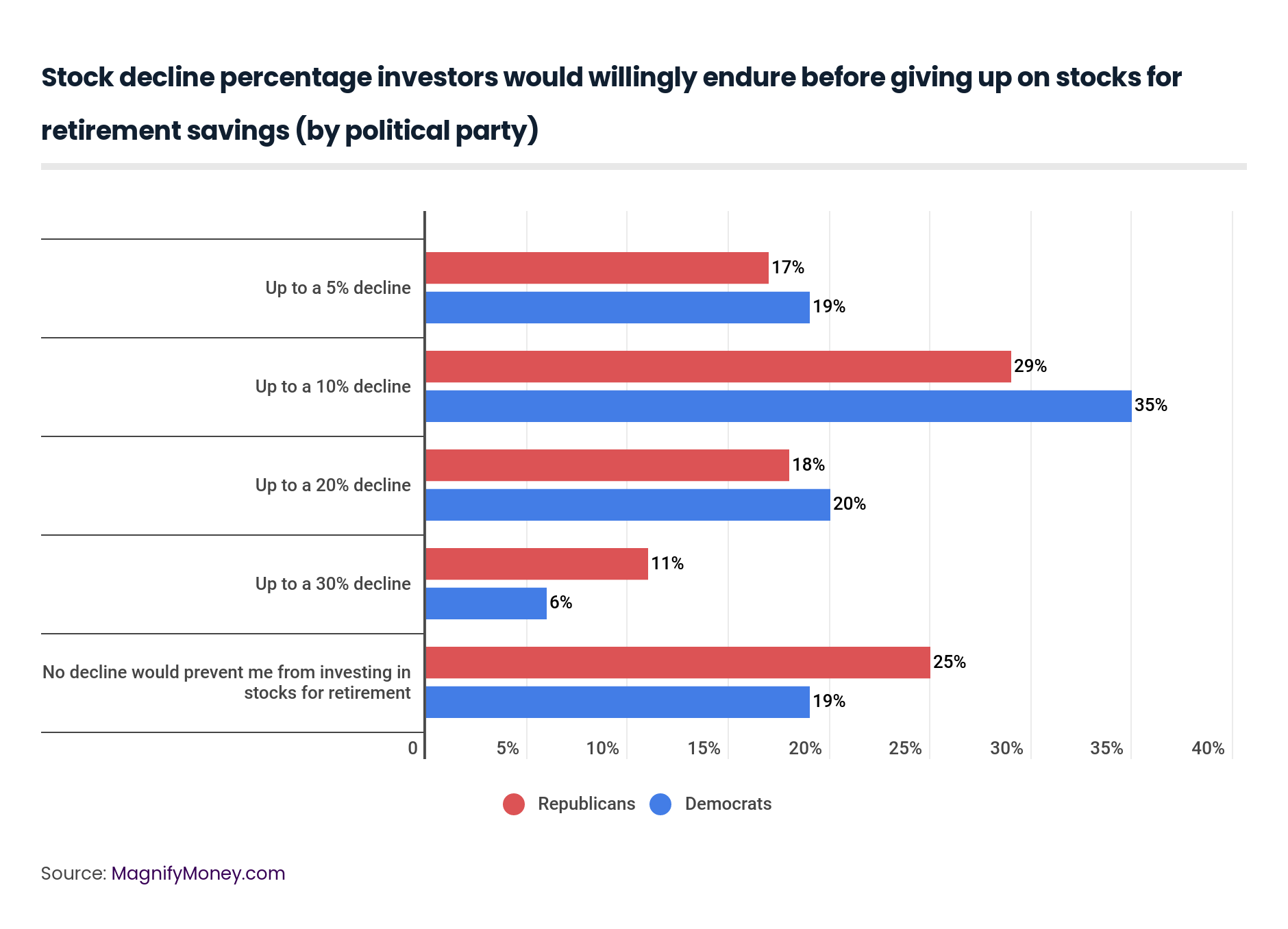

The survey also tried to capture how an investor’s political views might impact their risk tolerance. We uncovered a few differences in risk tolerance among people of different political persuasions.

Survey respondents who identified as Republicans showed a higher stock market risk tolerance than reported Democrats: 25% of Republicans responded that no amount of decline in the stock market would cause them to give up on stocks, compared to 19% of Democrats.

Meanwhile, 19% of Democrats could stomach only up to a 5% decline in the stock market before giving up on their stocks, versus 17% of Republicans. On the flip side, only 6% of Democrats could handle up to a 30% dip in the market, compared to 11% of Republicans.

Your risk tolerance is based on several factors, some that are more concrete and others that are more emotional. Determining your risk tolerance is important because it helps dictate your asset allocation: how much of your investments are in stocks, bonds, or other asset classes. Stocks are typically higher risk, but offer higher returns. Bonds are generally considered a safer asset, though with smaller returns.

There are a number of questions you can ask yourself to help determine your risk tolerance:

There are a multitude of online questionnaires that can help you determine your risk tolerance. Another good option for those assessing their risk tolerance is to enlist the help of an RIA – or registered investment advisor. These are trained professionals who can help you make sense of the wild world of investing, although you will often have to pay a fee. If you’re looking for a place to start, MagnifyMoney has reviews of RIAs.

MagnifyMoney commissioned Qualtrics to conduct an online survey of 740 Americans who have a retirement savings account. The survey was fielded October 1-3, 2019.

In the survey, generations are defined as the following ages in 2019:

Members of Generation Z (ages 18 to 22) and the Silent Generation (ages 74 and older) were also surveyed, and their responses are included within the total percentages among all respondents. However, their responses are excluded from the charts and age breakdowns due to the smaller population size among our survey sample.

Sarah Berger

Sarah BergerSarah Berger is a former writer at LendingTree, where she covered personal finance, specifically focusing on challenges and opportunities facing millennials. Before joining LendingTree, she was a writer for CNBC and Bankrate.

Read More