MagnifyMoney

Saving for retirement is a lot like hitting the gym: you know you should be doing it, but working up the motivation to go can be challenging. A recent MagnifyMoney survey of over 1,000 Americans found that while 55% of respondents would like to retire early, they simply aren’t saving enough to do so.

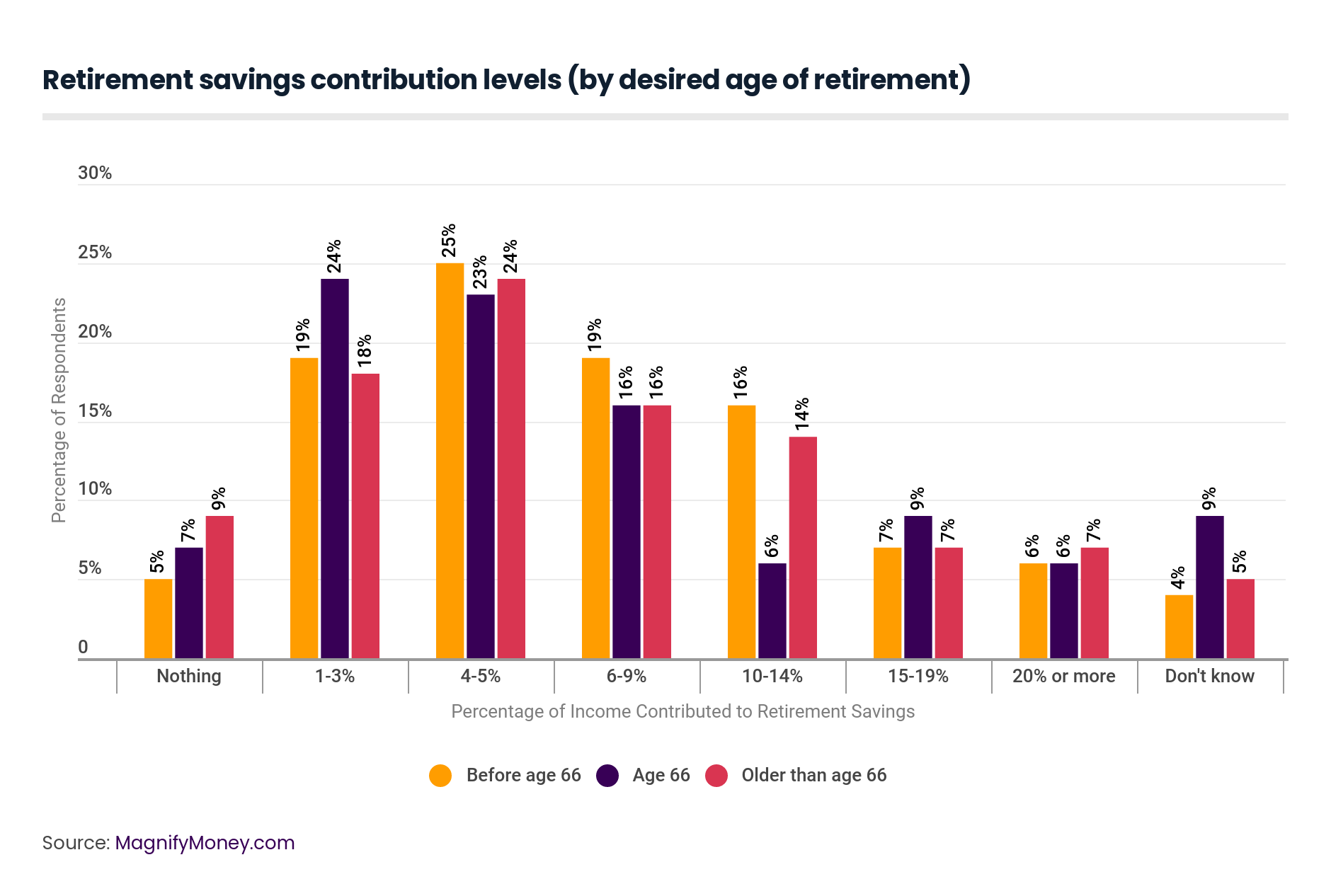

Of the survey respondents who said they’d like to retire before the age of 66, 25% are saving just 4% to 5% of their income, while 19% are saving only 1% to 3% of their income. At this rate, aspiring early retirees are setting themselves up for a major disappointment.

For our survey, we asked respondents to come clean about how much they are actually stashing away for their retirement years. We found that 23% of those surveyed contribute just 4% to 5% of their income to retirement — far less than the typical recommended amount of 15%.

Meanwhile, 18% contribute between 1% to 3% to retirement savings, and a stunning 12% don’t contribute anything at all. Not everyone is procrastinating on building a nest egg, though: 16% of respondents are saving between 6% to 9% of their income for retirement, 14% are saving between 10% and 14% and 6% are saving 15% to 19%. At the high end of the curve, only 5% of people are saving 20% or more of their income to retirement savings.

Younger people certainly have room for improvement. Over half of millennial respondents (51%) are saving only 5% or less of their income for retirement, while less than a quarter (24%) are saving over 10% of their income. Despite their relatively low rate of savings, 69% of millennials say they want to retire early, before the age of 66.

Gen Xers seem to be a bit out-of-touch with reality: many aren’t aggressively saving for retirement, but they’re still saying they would like to retire early. While 62% of Gen Xers say they want to retire before age 66, over half of them (56%) are socking away less than 10% of their income for retirement.

Our takeaway: Younger generations might be in for a rude awakening if they crunch the numbers to determine when they’d actually be able to retire, based on their current rate of savings.

Baby boomers are in a different situation, as many of them are close to or already retired. Understandably, as more boomers retire (according to our survey, 39% of that generation said they’re already retired), many are understandably stashing away less in retirement savings. It makes sense that our survey found 29% of boomers said they are not saving anything for retirement.

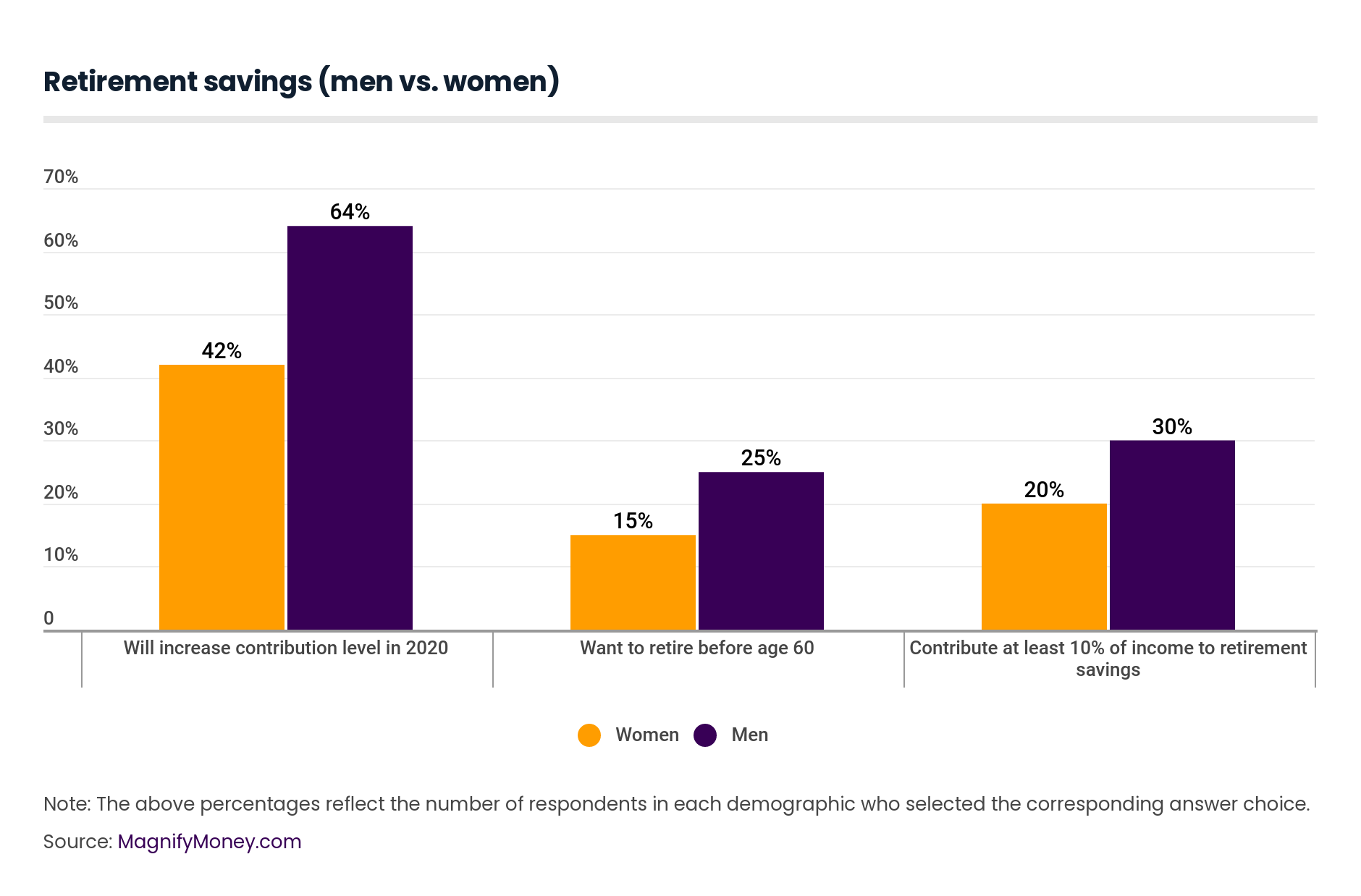

When comparing retirement contributions by gender, there are a number of stark differences — most notably the 18% of women who said they are not saving anything for retirement, compared to 7% of men. Additionally, only 20% of women are saving at least 10% of their income for retirement — much less than the 30% of men who are doing the same.

One possible reason for this discrepancy could likely be chalked up to the gender wage gap, as women are still earning just 82 cents for every dollar pulled in by a man. Less money earned means less money available to save. Lower earnings might also explain why women are less likely to say they want to retire early: Our survey found that 49% of women want to retire before age 66, compared to 60% of men.

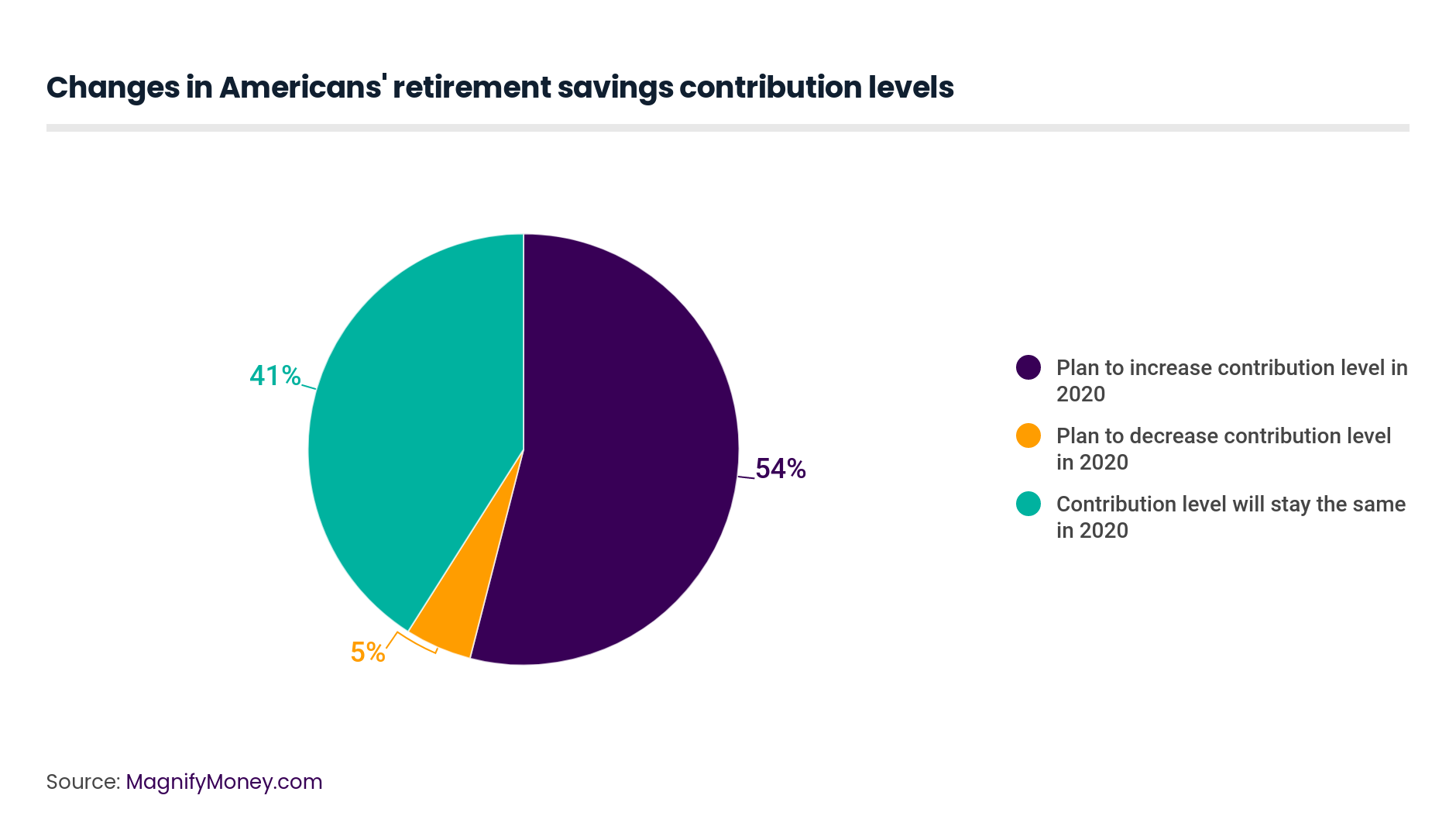

Our survey found that overall, 54% of respondents said they will increase their retirement contributions in 2020. By generation, that included 69% of millennials and 57% Gen Xers. Understandably, only 29% of baby boomers plan to up their contributions in 2020.

Of the respondents who say they plan to increase their retirement contributions in 2020, many aim to retire early: 63% of those who want to retire before age 66 are planning on upping their contributions this year.

Our survey found wide variance regarding when respondents had last increased their contributions. While 38% of respondents said that they have increased their retirement contributions in the past year, 17% admitted that they have never dialed up their contributions. Meanwhile, 24% of people said that the last time they increased their retirement contributions was two to three years ago, 7% said it was four to five years ago, another 7% said it was more than five years ago — and 6% said they do not know when they last increased their contributions.

Our survey found that when it comes to how much of their income people are devoting to retirement savings, it’s all over the map, from over 20% to nothing at all. So with no clear consensus among our survey respondents, how much should you actually be saving for retirement?

When it comes down to it, there are many factors that play a role in how much you should stash away for your golden years. The most important step, though, is to just start saving — check out our listings of the best IRA providers and the best robo-advisors to begin the process. That might sound simple, but a staggering 12% of our survey respondents did admit to saving nothing at all.

The importance of saving for retirement now rather than later cannot be emphasized enough: It takes time for your returns to compound. The sooner you start, the more time you allow your investments to grow. Additionally, you should contribute up the percentage that your employer matches (if they offer that benefit) — otherwise, you’re essentially leaving money on the table.

For those looking for specific metrics and benchmarks to gauge how much they should be socking away, there are a number of tried-and-true guidelines. Fidelity, for example, recommends saving 15% of your pre-tax income for retirement (that percentage includes any contributions you also get from your employer).

That percentage was calculated with the assumption that you’re saving for retirement between the ages of 25 and 67, and that most people will need to draw around 45% of their retirement income from their own retirement savings in order to live comfortably in their golden years. Looking at Fidelity’s 15% as a guideline, it’s clear that many people are falling behind, as our survey found only 12% of people are saving at least that much. Additionally, Fidelity’s guideline of 15% is assuming that the person wants to retire at age 67, when in fact our survey found most people (55%) want to retire before age 66.

MagnifyMoney commissioned Qualtrics to conduct an online survey of 1,064 Americans with a retirement savings account, with the sample base proportioned to represent the overall population. The survey was fielded Dec. 10-16, 2019. For the purposes of our survey, we defined generations as: millennials (ages 23 to 38), Gen Xers (ages 39 to 53) and baby boomers (ages 54 to 73).

Members of Generation Z (ages 18 to 22) and the Silent Generation (ages 74 and older) were also surveyed, and their responses are included within the total percentages among all respondents. However, their responses are excluded from the charts and age breakdowns, due to the smaller population size among our survey sample.

Sarah Berger

Sarah BergerSarah Berger is a former writer at LendingTree, where she covered personal finance, specifically focusing on challenges and opportunities facing millennials. Before joining LendingTree, she was a writer for CNBC and Bankrate.

Read More