MagnifyMoney

It seems like everyone has an opinion about millennials these days, but perhaps what they should be saying is that they are confident and optimistic. MagnifyMoney has surveyed more than 1,000 Americans on their views about wealth, and we found that millennials have a remarkably positive outlook when it comes to the subject.

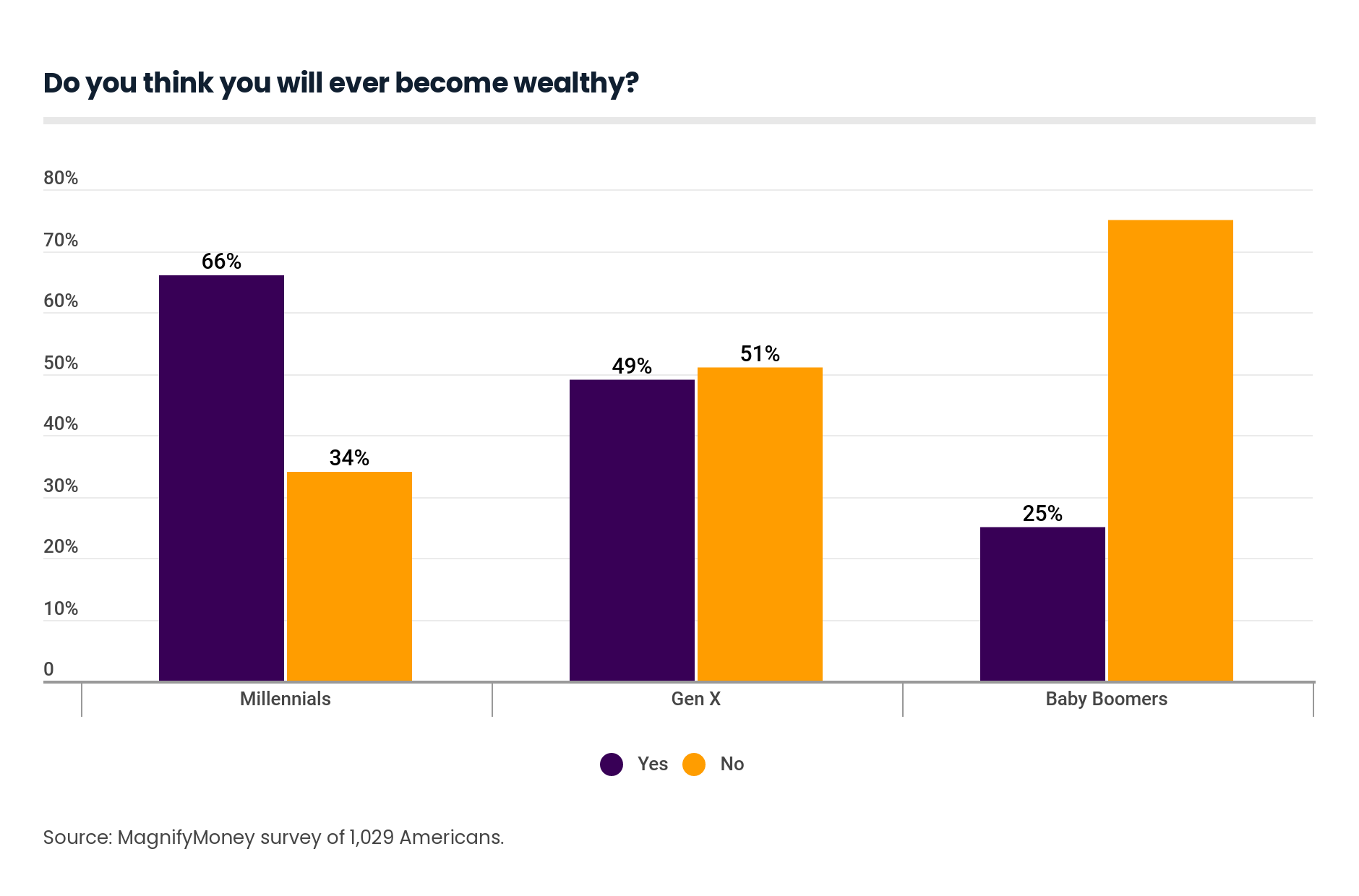

Compared to the other generations surveyed, millennials are much more likely than older generations to believe that they’ll become wealthy someday. Whether this comes from youthful exuberance, wishful thinking or a healthy attitude toward building wealth is not entirely clear. But what is clear are the striking generational perspectives on wealth revealed by our study.

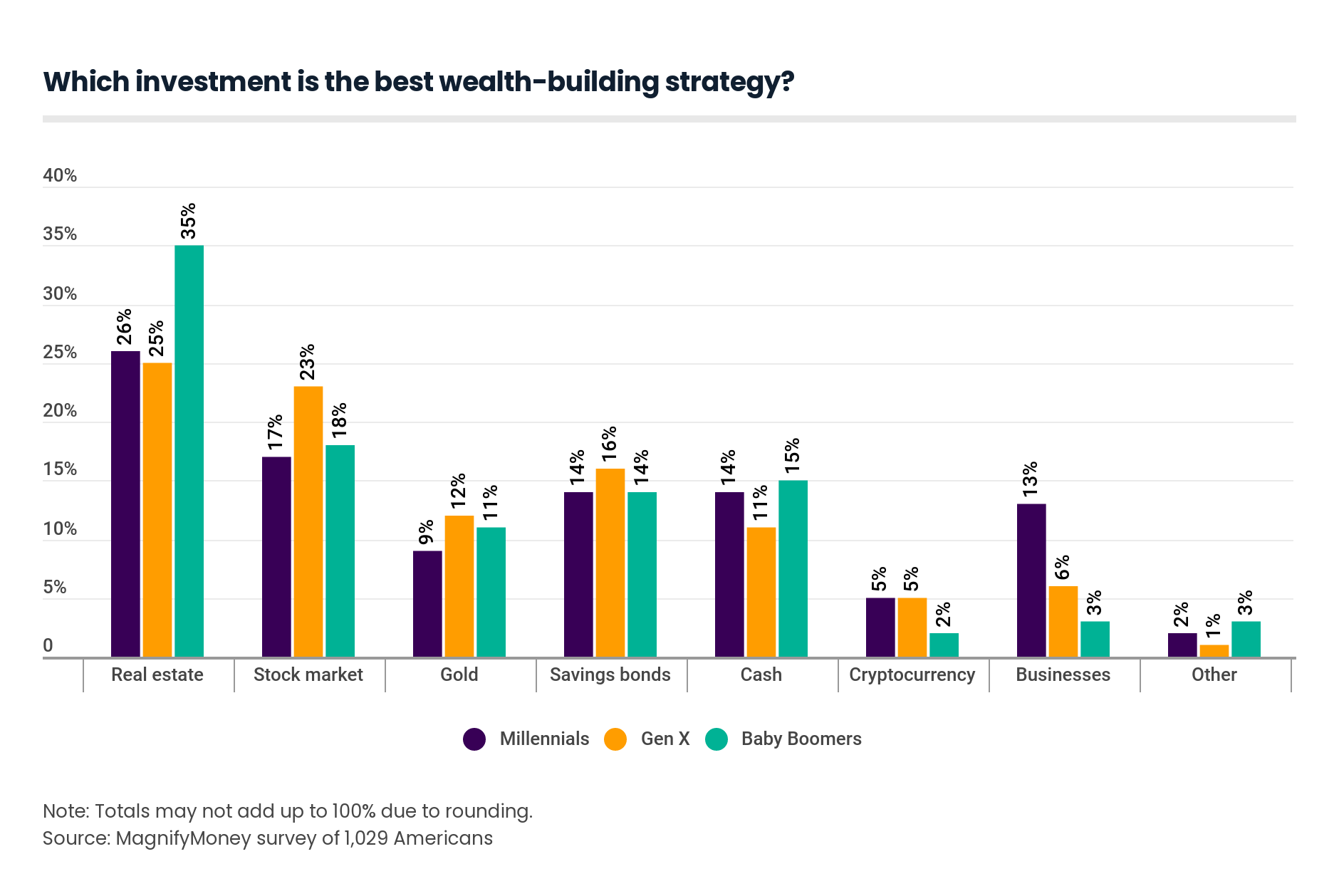

The two most popular strategies for wealth building among millennials are investing in real estate and in the stock market, but they’re hardly the only generation to take that approach. Across the board, real estate investing and the stock market were named as the two most popular investment strategies.

Still, both the real estate and stock market are subject to fluctuations, such as those seen during the Great Recession. According to a Gallup poll published in May 2019, during the Great Recession of 2008 to 2010, Americans were just as likely to name savings accounts or CDs as the best long-term investments, on par with stocks and real estate. As of 2019, the poll found that Americans currently view stocks and real estate as the best long-term investments.

Of course, this mindset could change quickly if another economic downturn hits. But for now, property owners have cause to celebrate. In 2018, home values were the highest on record, according to Gallup.

That same Gallup poll found that those who actually invest in stocks were more confident in the value of stocks as an investment, though stock ownership remains below pre-recession levels. Note that the S&P 500, which is considered a proxy for the stock market as a whole, has gained 9% per year on an annualized basis over the last decade — that return rises to an annualized gain of more than 11% per year when dividends are reinvested.

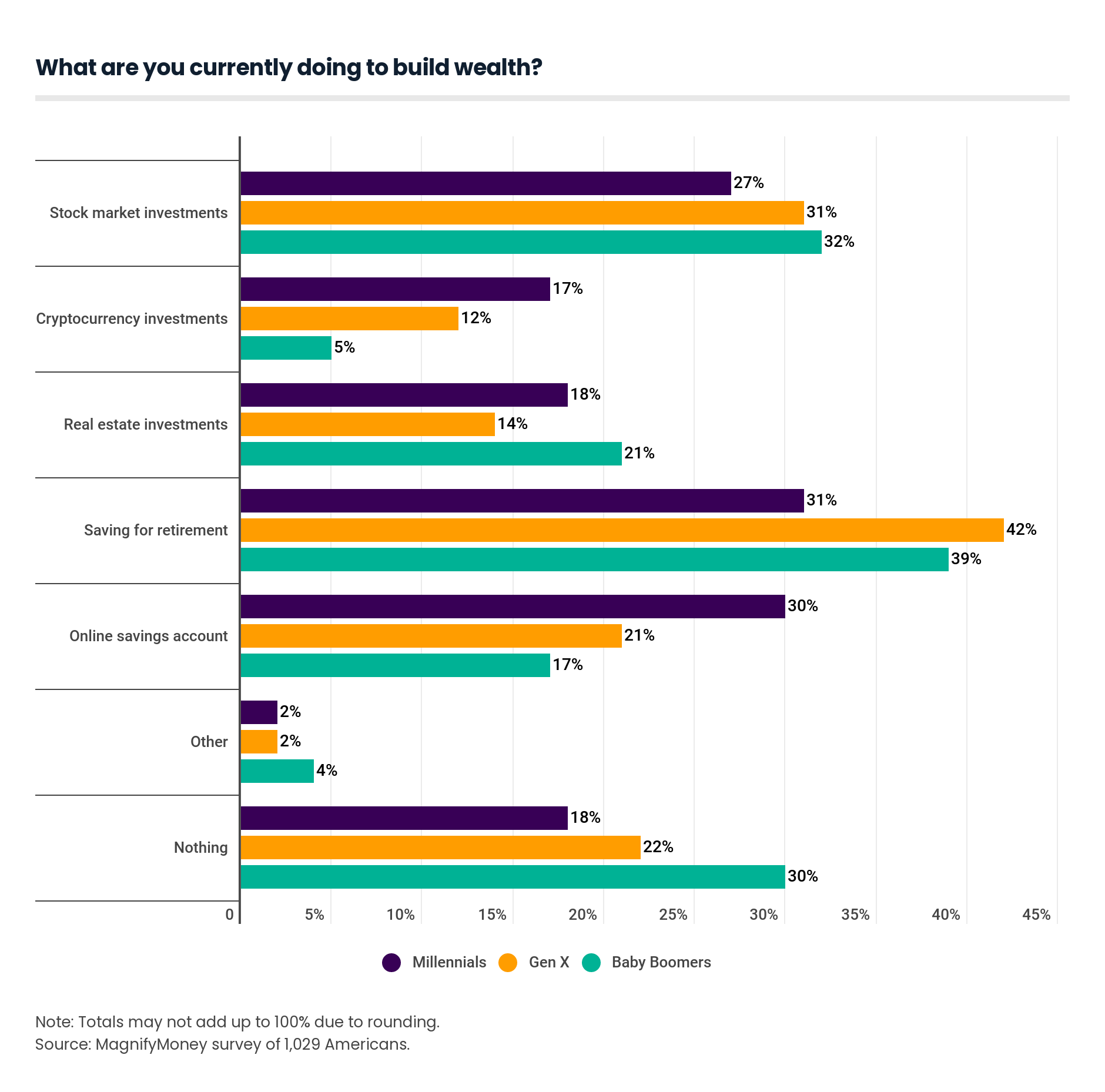

But even if stock and real estate strategies can be effective, debt may still stand in the way of some millennials’ wealth-building efforts. Due to rising student debt burdens, it’s not uncommon for millennials to carry large amounts of debt.

According to Misty Lynch, a Boston-based resident certified financial planner (CFP) with the savings and investing app Twine, millennials may be too accustomed to debt. “Millennials are used to having debt and feel like it is just part of life,” Lynch said. “This sometimes hurts them if they continue to add to their debt without considering the long term impact.”

Lynch also noted that the glitz of social media can affect millennial finances: “Social media has changed the definition of wealth. It is easier to appear wealthy in this Instagram-era even if your bank account doesn’t back that up.”

Plus, although 66% of millennials believe they’ll someday become wealthy, the survey also revealed that 18% of millennials currently aren’t doing anything to build wealth. For millennials looking to start the process, saving for retirement is a great launching point. One suggestion from Cynthia Loh, vice president of Digital Advice and Innovation at Charles Schwab in Denver, is that if your employer offers a 401(k) plan, you should set up recurring contributions that deposit money from your paycheck. Plus, you should max out annual contributions if you can afford to. The potential match from an employer is an added bonus worth taking advantage of.

For those without access to a 401(k), consider checking out a robo-advisor, which can be great for newer investors. Most robo-advisors have low investment minimums, which makes it easy to start investing your money.

More than other generations, millennials believe they can become wealthy someday. The survey found that 66% of millennials believe that they will become wealthy compared to only 25% of baby boomers.

As baby boomers are in the 54-72 year age range, their different perspectives make sense. Baby boomers are in the phase of their life where they either have already retired or are nearing the end of their career. They know their potential for wealth building is slowing down.

In general, younger generations seemed to be more optimistic. For instance, Gen Xers are more optimistic than baby boomers, and Generation Z seems to be even more hopeful than millennials.

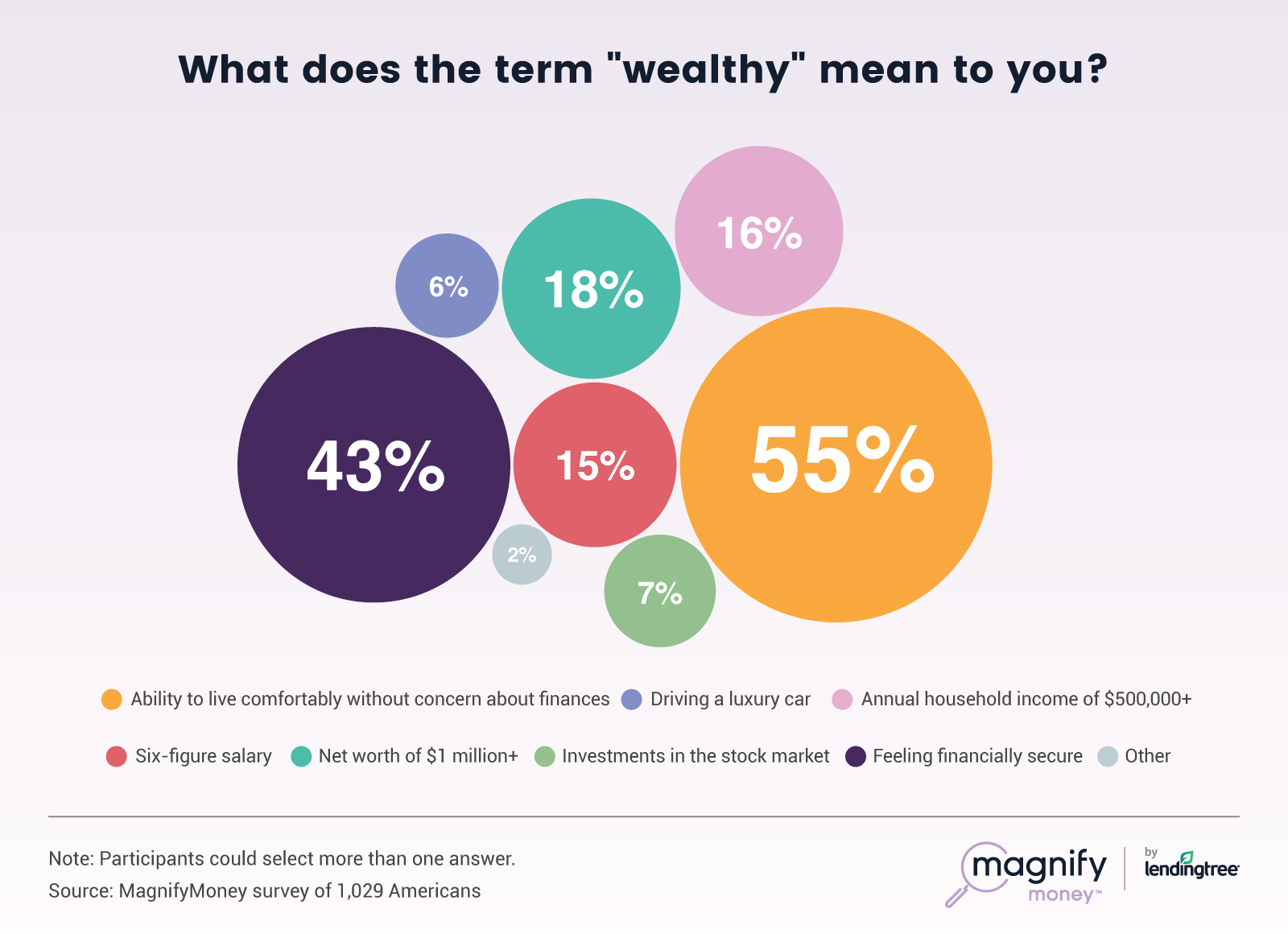

Youthful optimism aside, perhaps millennials simply have a different definition of wealth than older generations. Across all generations surveyed, 55% said they thought the definition of being wealthy was being able to live comfortably without worrying about their finances. If you’re looking to quantify wealth, 20% of millennials (more so than any other generation) reported that they define being wealthy as having $500,000 or more; only 8 percent of baby boomers feel this way. Networth finds more common ground between millennials and baby boomers — almost 18 percent of both generations feel a networth of at least $1 million signifies wealth.

Andrea Woroch, a money saving expert from Bakersfield, California, thinks that mindset may just be the key to millennial’s future financial success.

“Thinking positively about your money is key toward building better financial habits,” Woroch said. “Ultimately, your thoughts influence your behavior which will lead to a desired outcome, so if you think you will be wealthy then you can start acting in accordance with this vision.”

MagnifyMoney by LendingTree commissioned Qualtrics to conduct an online survey of 1,029 Americans, with the sample base proportioned to represent the general population. The survey was fielded June 24-27, 2019.

In the survey, generations are defined as:

Members of Generation Z (ages 18-21) and the Silent Generation (ages 73 and older) were also surveyed, and their responses are included within the total percentages among all respondents. However, their responses are excluded from the charts and age breakdowns due to the smaller population size among our survey sample.

Jacqueline DeMarco

Jacqueline DeMarcoJacqueline DeMarco is a freelance writer who is particularly passionate about finance. She began her career in the retirement industry. Today, she works with more than a dozen financial brands to create entertaining and educational money content.

Read More