MagnifyMoney

Each year MagnifyMoney asks consumers how much debt they racked up over the holiday season.

See historical results here:

—

With the holiday season drawing to a close, some Americans are going to find themselves nursing a pretty serious debt hangover.

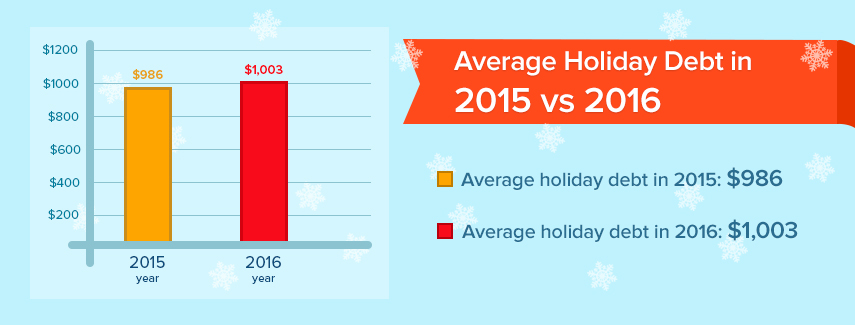

In our second annual holiday debt survey, MagnifyMoney found consumers who took on debt during the 2016 holiday season will kick off the New Year with an average of $1,003 worth of new debt. That is up from $986 in 2015, for a year-over-year increase of 1.7%.

Our survey consisted of a national sample of 552 Americans who reported they added debt during the holidays.

Here are key findings:

Racking up debt isn’t exactly a problem in and of itself, so long as you have the cash on hand to pay it off quickly. But in our survey, we found the vast majority — 65.2% — of consumers who took on debt did so unexpectedly this year, and didn’t budget for the extra expenses.

It’s easy to imagine scenarios in which people might spend more than they can afford over the holidays. Last-minute gifts, family emergencies, and, for some, fewer work hours, can all add up to a hefty bill if not planned for in advance.

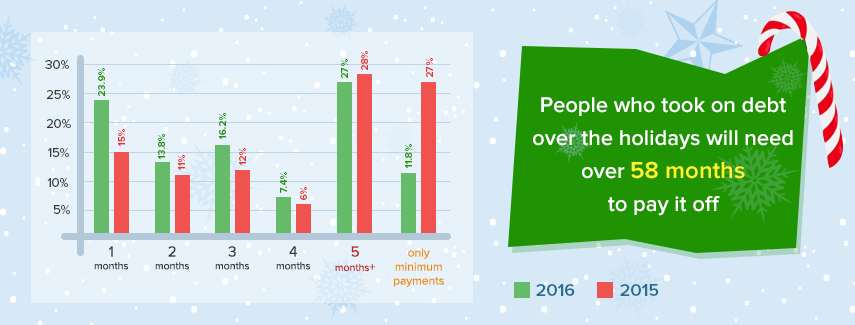

Less than one-quarter of those surveyed said they can pay off their debt within one month. Nearly half (46%) predict they’ll need four months or more to pay off their holiday debt, or will only make the minimum monthly payments.

Nearly 12% of respondents said they only plan on making minimum monthly payments, which can extend repayment for years.

Even a seemingly meager amount of debt can quickly balloon over time if it isn’t paid off aggressively.

A person carrying an average debt load of $1,003 who makes one $25 minimum payment per month would need 58 months (4.8 years) to pay off their debt. That calculation assumes an average APR of 16%.

On top of paying off their principal balance of $1,003, over that time they would pay an additional $442 worth of interest for a grand total of $1,445.

For another year, credit cards reign as the most popular source of holiday debt. In fact, even more consumers reported using credit cards for holiday debt this year than in 2015 — 59.9% vs. 52%.

Unfortunately, the number of consumers who turned to payday loans this year increased, from 6% in 2015 to 7.1% in 2016. Payday and title loans are hands down the most costly options for people who find themselves in need of cash.

We did find one bright spot, however. This year, the rate of consumers who said they used store credit cards fell dramatically, from 30% in 2015 to 17.1% in 2016. Store credit cards can often come with painfully high interest rates and other gotchas like dreaded deferred interest policies.

This year, half of survey respondents (50%) said their debt carries an APR of 10% and above. Among those, 34.7% have APRs between 10-19% and 16% carry APRs above 20%.

The rate of people who are stuck with 20% or higher APRs rose significantly year over year, from 9% in 2015 to 16% this year.

Despite the fact that almost half of respondents expect to take 4 months or more to pay off their debt, a mere 13% of respondents said they plan to shop around to find a better rate with a different bank or loan. That’s even worse than last year, when 22% of respondents said they would shop around for a better rate.

The most cited reason for not wanting to shop around is not wanting to deal with another bank, noted by 20.9% of respondents this year.

We found a consumer with $1,003 in debt at a 16% rate making minimum payments would shave over a year off debt repayment and save over $400 in interest payments by finding a 0% balance transfer.

Among all age groups, people ages 24-35 were most likely to say they went into debt this holiday season with a rate of 14.3%. With the exception of 45-54-year-olds, the likelihood of going into debt decreased with age. Seniors were least likely to say they went into debt, with a rate of 7.6%.

In preparation for the new year, MagnifyMoney released the 2nd edition of its free 45 page Debt Free Forever eBook – that you can download to prepare your action plan, tailored to whether your situation calls for a quick switch to a lower rate, or more significant debt payoff advice.

Key tips for beating the debt cycle include:

Before you consider a balance transfer:

If you need to buy yourself more time while you trim expenses and work on paying down your debt, a balance transfer can be a useful tool, but one that can backfire if you’re not disciplined. A balance transfer is simply a process where you transfer the balance from one or more credit cards onto a single new credit card with a different rate.

If it will help, you’ll first need to check your credit score to see where you stand since you’ll be applying for another credit card. Balance transfer offers typically require a credit score of 680 or higher to be approved.

You can check your FICO score for free using Discover’s free FICO® Score Card which is even available to non-customers who don’t use Discover products, or use another free source.

It’s also important to do the math before signing up for a new credit card. Be honest about how much you can afford to pay each month to determine how much a balance transfer will save you in the long run.

And keep these tips in mind:

Methodology: MagnifyMoney surveyed 552 U.S. adults who reported they added debt over the holidays via Google Consumer Surveys from December 26 – 27.

Average Debt Among Shoppers Who Said They Went into Debt Over the Holidays

2016: $1,003

2015: $986

Did you go into debt this holiday season?

Age 25-34: 14.3%

Age 35-44: 10.9%

Age 45-54: 12.5%

Age 55-64: 8.5%

Age 65+: 7.6%

If you went into debt, did you plan to go into debt this holiday season?

Yes: 34.8%

No: 65.2%

How much debt did you take on over the holidays?

$0-999: 62.1%

$1,000-1,999: 19.7%

$2,000-2,999: 6.6%

$3,000-3,999: 2.8%

$4,000-4,999: 0.7%

$5,000-5,999: 1.5%

$6,000+: 6.3%

Where did your holiday debt come from?

Credit cards: 59.9%

Store cards: 17.1%

Personal loan: 8.9%

Payday / title loan: 7.1%

Home equity loan: 5.3%

When will you pay the debt off?

I’m only making minimum payments: 11.8%

1 month: 23.9%

2 months: 13.8%

3 months: 16.2%

4 months: 7.4%

5 months+: 27.0%

Will you try to consolidate your debt or shop around for a good balance transfer rate?

Yes: 13.1%

No – Don’t want to deal with another bank: 20.9%

No – Too many traps: 16.0%

No – Rate is already low: 26.3%

No: – Don’t know enough about it: 11.0%

No – Wouldn’t qualify: 12.6%

How stressed are you about your holiday debt?

Stressed: 29.7%

Not Stressed: 70.3%

What interest rate are you paying on your debt?

Less than 9%: 41.7%

10-19%: 34.7%

20-29%: 16.0%

Mandi Woodruff

Mandi WoodruffMandi Woodruff is a former executive editor at MagnifyMoney. She was previously the personal finance correspondent at Yahoo Finance and the personal finance editor at Business Insider.

Read More