MagnifyMoney

Spending money is easy and saving money is hard. We get it. That being said, there are concerning savings habits that more than 7 in 10 consumers share.

A MagnifyMoney survey of more than 1,000 Americans looked at how consumers prefer to save money, finding that 72% don’t have a preset monthly savings amount in their budget. Only 28% of consumers said their favorite savings strategy is setting automatic monthly transfers to their savings account each month.

We asked two of our experts — DepositAccounts founder Ken Tumin and MagnifyMoney millennial finance columnist Sarah Berger — to weigh in on these discoveries and how consumers can make better savings choices.

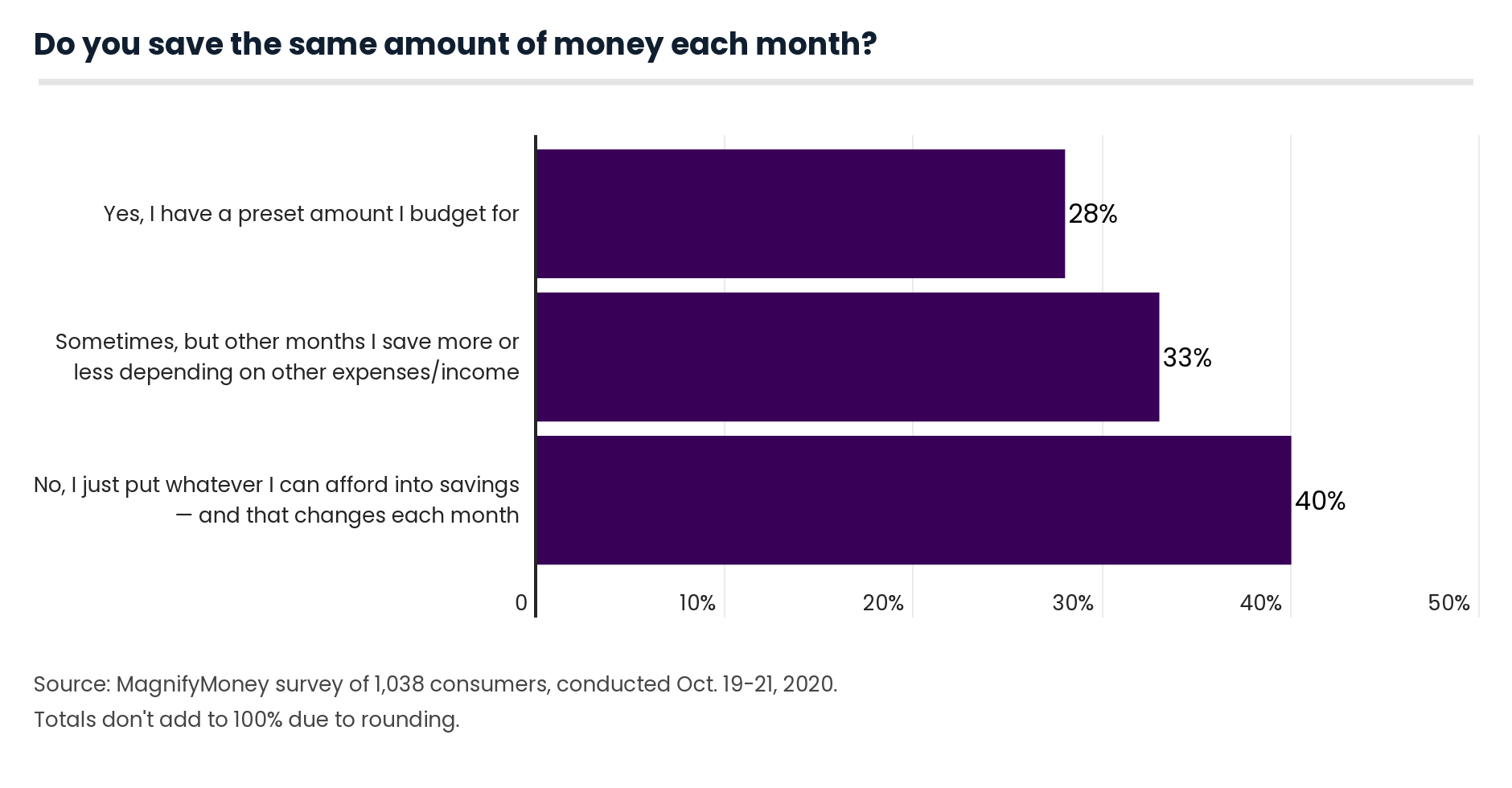

Only 28% of consumers set savings targets in their budget, with men doing so more often than women.

By gender, 35% of men have a preset amount they budget for, versus 21% of women.

“Time after time, we have found that the effects of the gender wage gap are very real — and they often put women at a financial disadvantage,” Berger said. “In many cases, you can only afford to save money if you are able to pay all of your bills and meet your basic living needs.”

More Than a Third of Working Americans Experienced a Pandemic Pay Cut

If men are earning more money, Berger said, they’re less likely to be living paycheck to paycheck and therefore are more likely to save. Berger commented that eliminating the gender wage gap is a crucial step in putting women on an even playing field when it comes to setting — and reaching — savings targets.

As expected, income affects whether consumers set savings targets. In fact, 46% of those who make more than $100,000 a year have a preset savings amount they budget for each month, compared with just 16% of those who make less than $25,000.

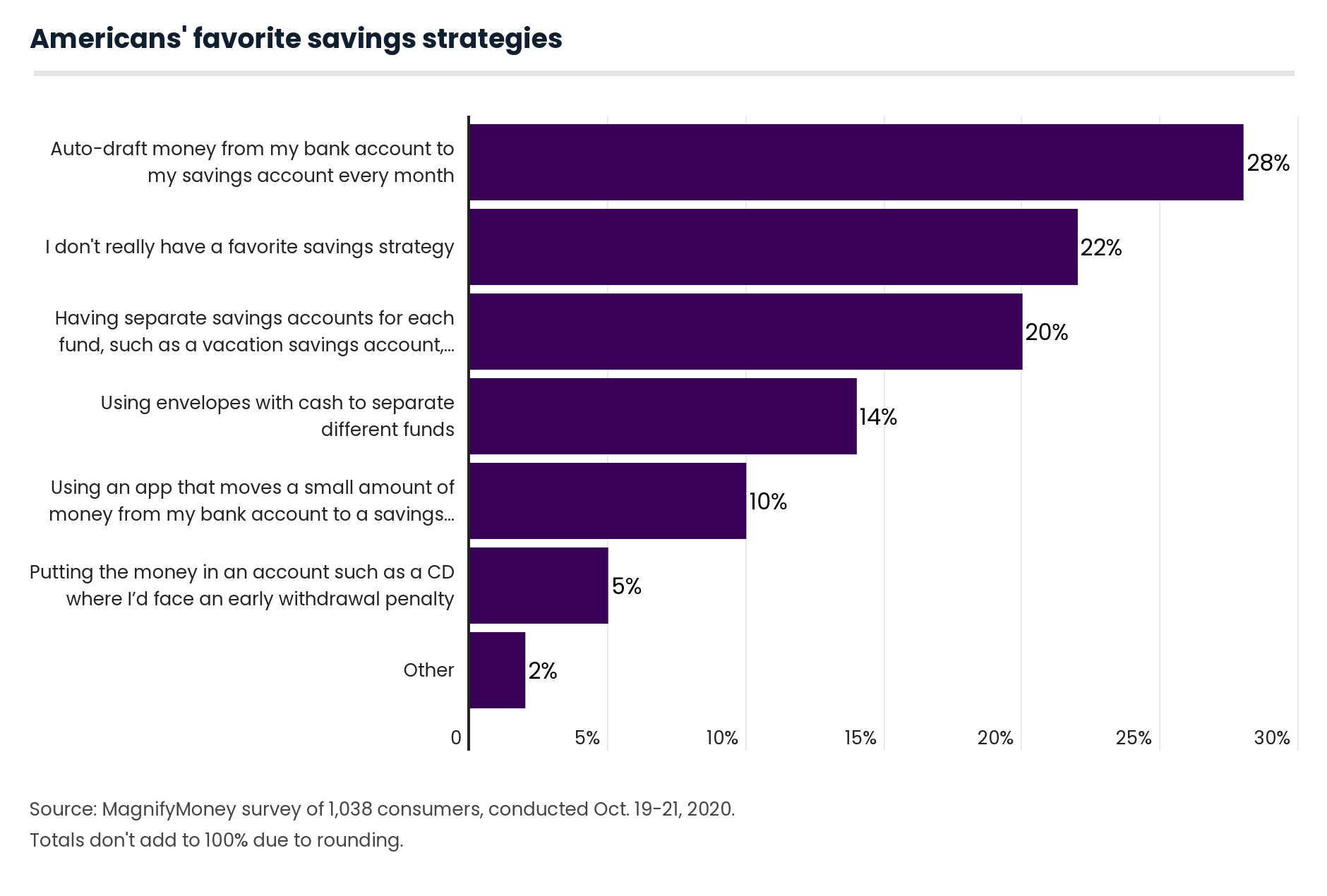

Consumers have their preferences when it comes to how they like to save money, with the most favored method being setting up automatic transfers each month (28%).

Consumers with higher incomes are more likely than those who earn less to prefer automatic monthly transfers to their savings account, possibly because lower earners may be at risk of overdrafting their account. This may explain why men (31%) enact this method more than women (26%), if you consider the gender wage gap.

Berger said she’s a fan of the automatic transfer method. “Personally, I like having 20% of my paycheck — after retirement contributions are taken out — automatically rerouted to a separate savings account on payday,” she said. “It makes me feel accomplished and like I am paying myself first, as opposed to just saving whatever is left over from my monthly budget.”

That being said, she doesn’t believe the method of saving is as important as the act of saving itself. “As long as you are saving, that’s what counts,” Berger said. “So, you should feel confident in taking whichever approach is best for you.”

Tumin sided with the 28% of consumers who said automatic transfers are their favorite way to save. “Everyone is busy, and if you have to manually add to your savings, the odds are high that you’ll put it off,” Tumin said. “When the transfers are scheduled to take place automatically on a regular basis, the savings will build even when you’re busy.”

Another popular savings method that respondents mentioned was the envelope method. Just about 1 in 7 Americans rely most on this method to save money, which involves setting aside cash in envelopes marked for different categories. This means people aren’t earning any interest on their savings, but the tangible experience can help some feel less tempted to spend.

Having a savings strategy in place isn’t a guarantee, though, as 22% of consumers reported not having a favorite approach. Again, there’s a noticeable gap between the savings habits of men and women. Nearly twice as many women (28%) said they don’t have a go-to savings strategy, compared with 16% of men.

There are various savings methods for consumers, and how they get there can vary greatly.

The most respondents (36%) save the amount of money left over after paying for living expenses. Those who earn less are more likely to save what’s left after discretionary spending than those who make more.

One smart path toward savings that only 16% chose was to create a monthly budget to understand how much they can afford to save each month. This is a great step to take before setting monthly savings goals or setting up an automatic transfer to a savings account.

Deciding to save based on what’s left over suggests that there is little planning and budgeting involved, Tumin said. Creating a monthly budget that includes savings is the best approach to take if you want to prioritize saving, he said.

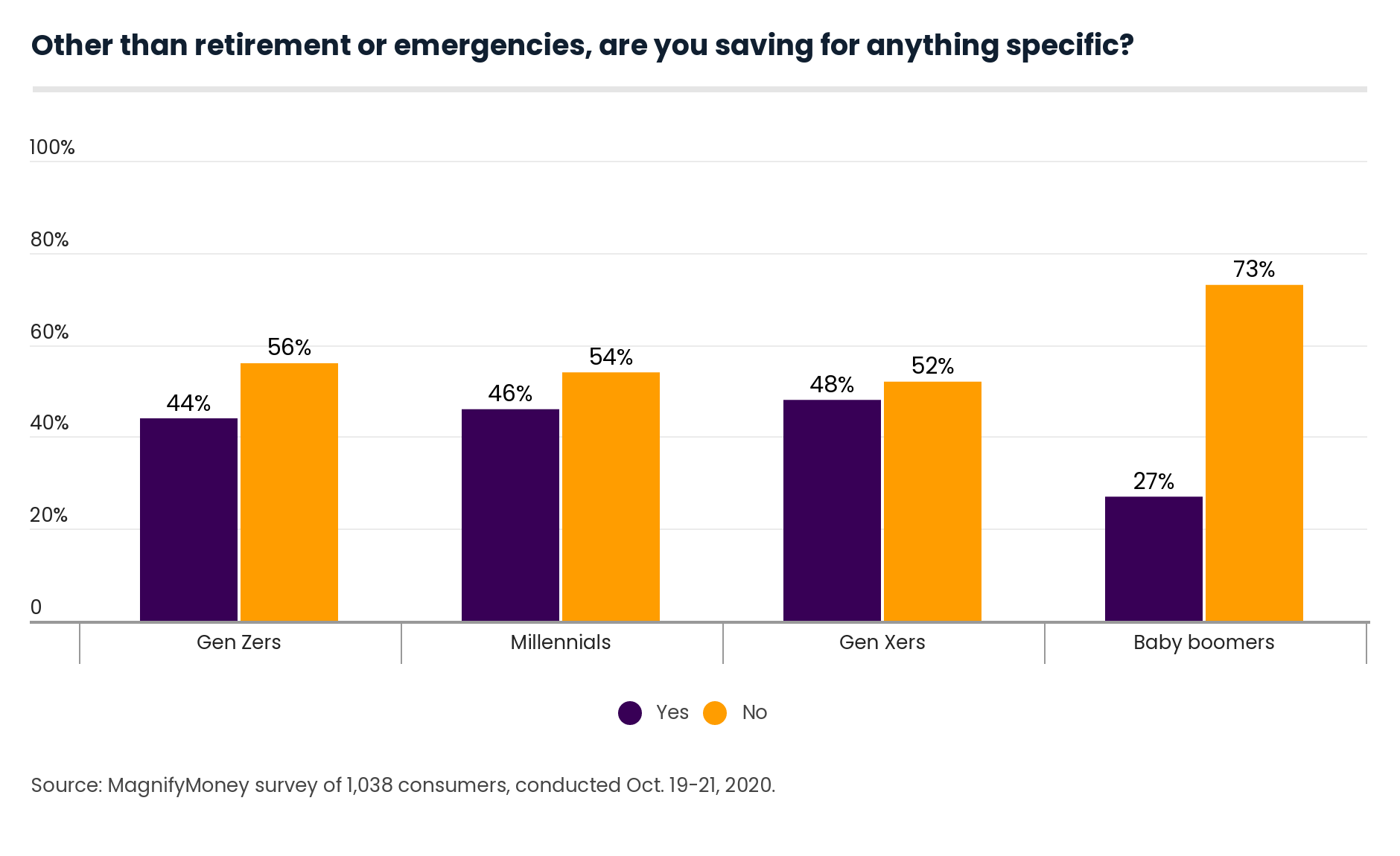

The majority of savers are doing so without any specific goals in mind. Other than saving for retirement or emergencies, only 40% of consumers are saving for something specific.

While baby boomers are the least likely to be saving for something specific (27%), Generation Xers are most likely to have a specific saving goal in mind.

Almost half of Gen Xers (48%) are saving for something specific. Gen Xers are still pre-retirement age and likely have more income coming in and expenses coming up (think college and weddings for children) than baby boomers.

According to the latest edition of MagnifyMoney’s monthly savings index, 21% of Americans don’t save any money at all. Other than general savings, emergencies or retirement, the highest percentage of consumers in December were saving up for vacation or a new car.

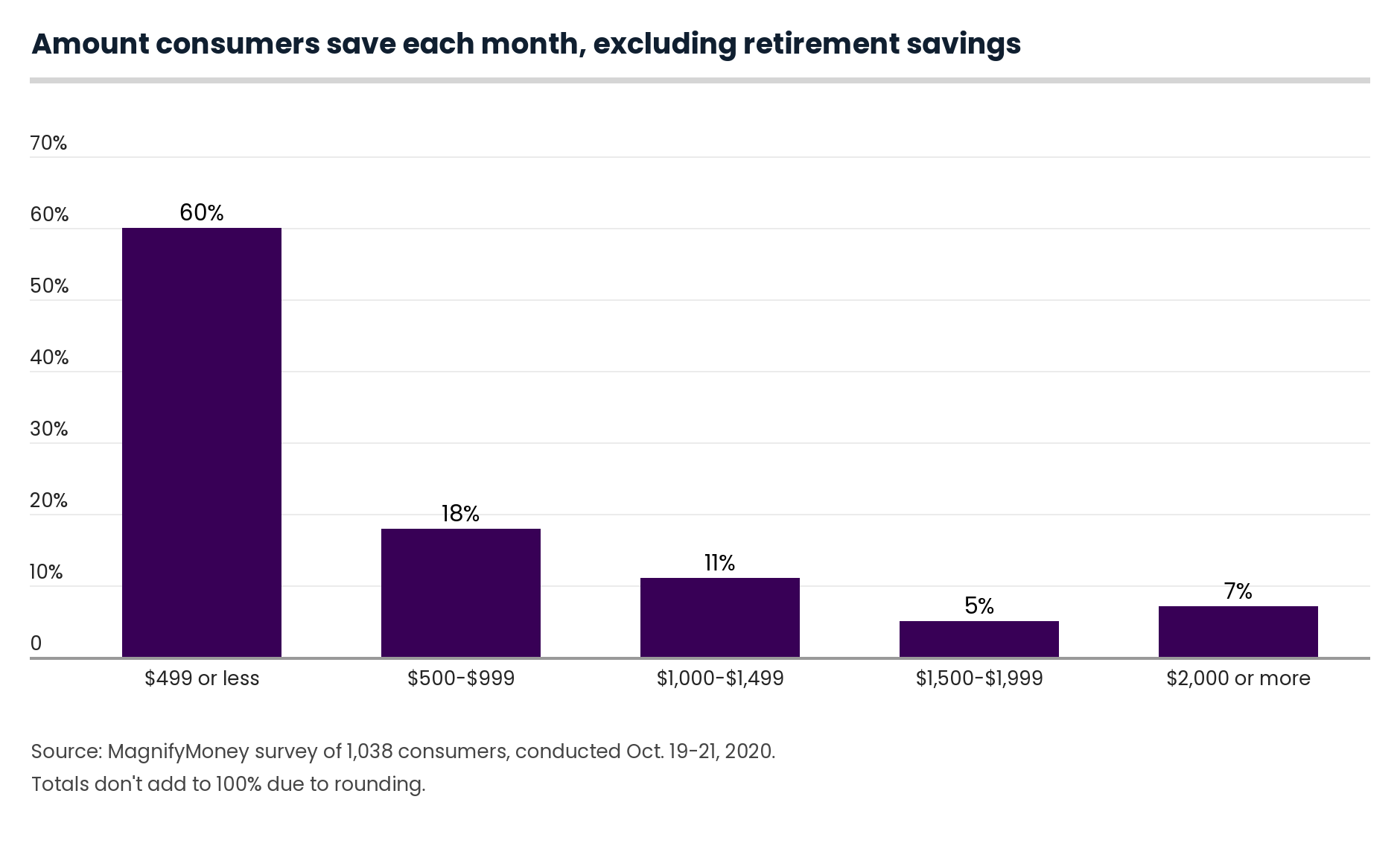

When it comes to how much is put in savings, 6 in 10 Americans save less than $500 a month.

Breaking it down by education, 13% of those with a bachelor’s degree or higher put $2,000 toward non-retirement savings each month, compared with 5% of those with some college and 1% with only a high school education.

Once again, men come ahead in how much they save compared to women. While 71% of women save less than $500 a month outside of retirement contributions, only 49% of men reported doing the same.

Understandably, household income also plays a role. The group most likely to save less than $500 a month earns less than $25,000 a year. On the flip side, the group most likely to save $2,000 or more each month earns $100,000 or more annually.

“Most Americans aren’t saving enough,” Tumin said. “Generally, it should be more than $500 a month.”

He explained that the amount Americans should save depends on their emergency and “sinking” funds. The latter is a small amount of money set aside every month. Having a well-funded emergency fund will help if you lose your job or face unexpected expenses, while having a well-funded sinking fund will help you afford planned expenses such as car maintenance or vacation.

Understandably, the COVID-19 pandemic is likely hindering savings efforts. “Those who have lost jobs during the pandemic will likely have to draw on their savings rather than add to their savings until they’re able to find a new job,” Tumin said.

43% of Consumers With Emergency Funds Tapped Those Savings Amid Pandemic

He believes that in times of uncertainty — like during a pandemic — it’s especially important to have a well-funded emergency savings fund. This fund can ensure you have savings for you, your pet or some other emergency expense.

“Any additional savings, such as from the government economic impact payments, should be used to build up your emergency fund,” Tumin said.

MagnifyMoney commissioned Qualtrics to conduct an online survey of 1,038 Americans, with the sample base proportioned to represent the overall population. We defined generations as the following ages in 2020:

The survey also included responses from the silent generation (ages 75 and older). However, their responses weren’t included in the generational breakdowns due to low sample size among that age group.

The survey was fielded Oct. 19 to 21, 2020.

Jacqueline DeMarco

Jacqueline DeMarcoJacqueline DeMarco is a freelance writer who is particularly passionate about finance. She began her career in the retirement industry. Today, she works with more than a dozen financial brands to create entertaining and educational money content.

Read More