MagnifyMoney

More than 4 in 10 consumers with emergency funds have had to use money from them during the coronavirus pandemic, according to the latest MagnifyMoney survey.

We surveyed more than 1,000 consumers to find out the impact the crisis — which has sent shock waves through many Americans’ finances — has had on emergency funds, looking at everything from balances to when people think they should be used.

For the purposes of the survey, emergency funds are defined as separate savings accounts for covering emergency expenses. Here’s what we learned.

Two in 3 consumers (67%) with emergency funds have tapped their savings, which includes the 43% who have done so during the coronavirus pandemic.

The pandemic has hit some segments of the population harder than others. Generation Xers, for example, were most likely to use emergency funds during the pandemic (62%), compared with:

And 58% of parents with at least one child younger than 18 said they dipped into emergency savings to get by during this crisis.

“The pandemic and the lockdowns caused a surge in unemployment, and the unemployment rate remains elevated,” said Ken Tumin, founder of DepositAccounts. “Many American households that have experienced a job loss had to tap their emergency funds. Even if they were able to avoid drawing from their emergency fund, saving has become more challenging.”

While 41% of Americans reported having emergency savings in the 2018 U.S. Financial Health Pulse survey, MagnifyMoney found that 54% of consumers now say the same.

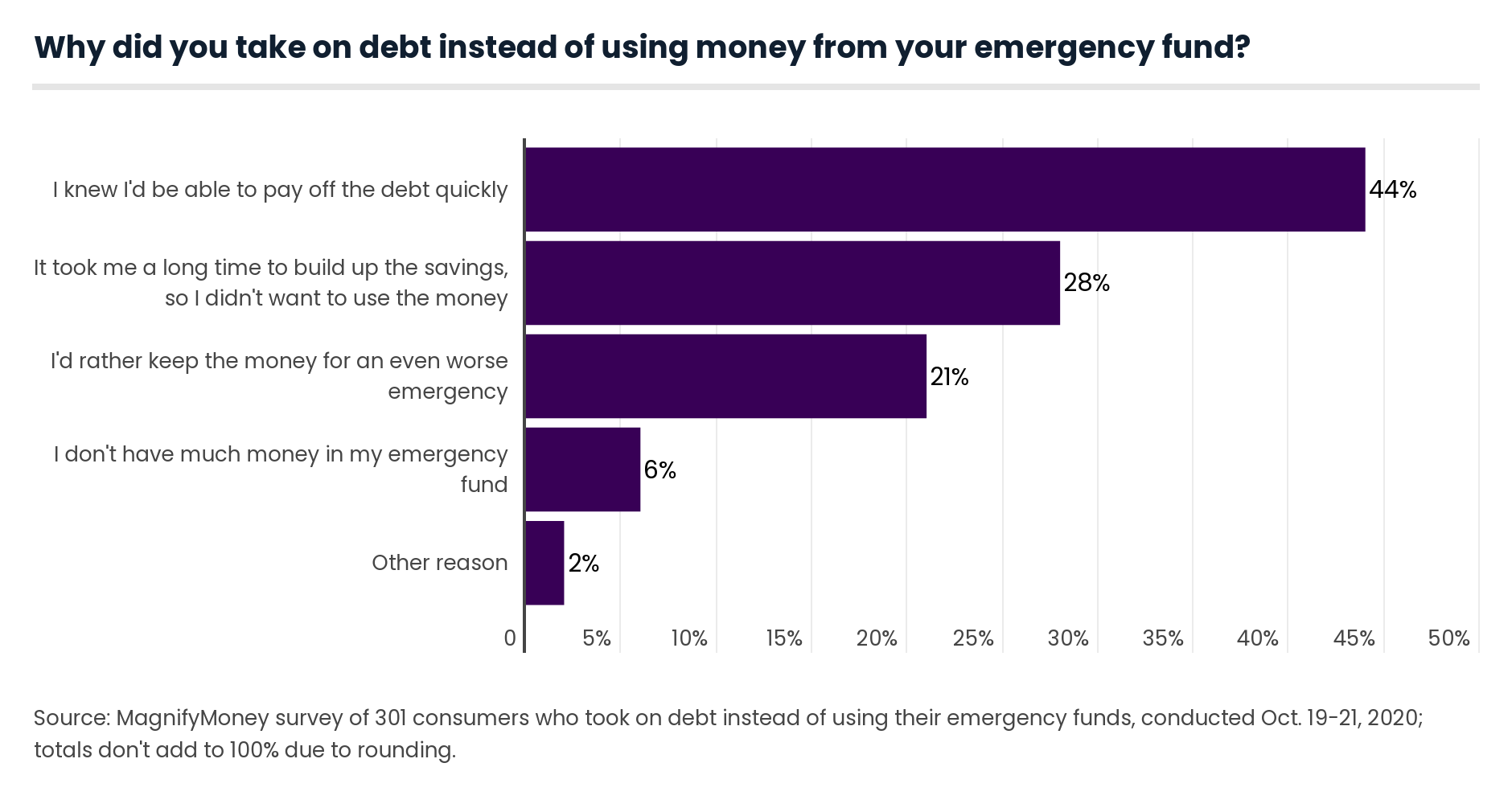

Having an emergency fund isn’t always a guarantee that someone isn’t going to take on debt. And 54% of those with emergency funds opted to take on debt instead of using that money at some point.

This is more common among men (62%) than women (43%). Also, 71% of Gen Xers and 64% of millennials reported taking on debt in lieu of using an emergency fund in the past.

There were several reasons why people took on debt rather than used their emergency funds, but paying off the debt quickly emerged as the top reason.

Men (48%) were more confident than women (37%) in their ability to pay off their debt quickly. But more women (25%) would rather keep the money for an even worse emergency than men (18%).

More than 2 in 10 (22%) respondents said they took on between $1,000 and $1,999 of debt instead of using their emergency fund. But a significant 15% said they took on $5,000 or more in debt rather than dipping into an emergency fund.

That high debt level was also most likely to occur among those earning $100,000 a year or more (30%), compared with 3% to 15% among the other income demographics.

“The whole point in having a rainy day fund is to be able to spend that money without having to go into debt,” Tumin said. “Keep in mind, an emergency fund is separate from any retirement savings you have. If you have funds set aside for an emergency or unexpected hardship, it is always better to use those funds than go into debt.”

There are many scenarios in which someone would — or wouldn’t — use their emergency fund. To gather more insight, our survey looked at six reasons people might dip into their rainy day funds:

The majority of people said a medical emergency or job loss are reasonable circumstances to use their emergency fund. More than 2 in 5 (41%) Gen Xers said they’d use it to pay off a large chunk of debt — the largest segment of the population.

By contrast, 55% of those with an emergency fund wouldn’t use that money to cover holiday gifts. Curiously, 30% of those who were laid off and 32% who had reduced salary or hours said they wouldn’t use their emergency fund in the event of a medical emergency expense. And almost half of those earning $25,000 a year or less said that they wouldn’t use that money for a major home repair.

Emergency funds aren’t just about deciding when to use them. To add perspective, we took a step back and looked at the “who” and “how much” components of these savings accounts for covering emergency expenses.

While 62% of men have emergency funds, just 45% of women reported having one — a 38% difference.

The ability to have an emergency fund can be influenced by many factors. For example, more than half of those younger than 55 have an emergency fund, but just 47% of baby boomers (age 55 to 74) do. That’s especially concerning during a pandemic when medical expenses are more likely to crop up.

Another trend our study revealed is that parents with at least one kid younger than 18 (62%) are more likely than parents with grown children (53%) or those without kids (46%) to have an emergency fund.

Consumers’ emergency fund balances vary greatly, from less than $1,000 (16%) to $20,000 or more (19%).

Gen Zers were the most likely to have less than $1,000 in emergency savings, with 31% reporting so, compared with 19% of millennials and 11% of Gen Xers.

Nearly all consumers — including those without emergency funds — said people should have at least one to two months of living expenses saved. And 95% think emergency funds are necessary.

Opinions can vary depending on individual circumstances, but about a third of respondents said that kind of savings should be able to cover three to four months of living expenses. Interestingly, those earning $100,000 or more a year were somewhat split on the issue — 25% said it should be one to two months’ worth of expenses, while another 26% said it should cover more than six months of expenses.

It’s generally recommended to have at least three to six months’ equivalent of your net income or take-home pay, with six months being the goal, Tumin said.

“Those that are the sole provider for their family, freelancers or have home or artisan businesses should strive to have a year’s income in their emergency fund,” Tumin said.

For these funds, Tumin suggests an easily accessible FDIC-insured savings account that doesn’t have withdrawal fees. That way, you’ll be able to use that money when you need it.

MagnifyMoney commissioned Qualtrics to conduct an online survey of 1,038 Americans, with the sample base proportioned to represent the overall population. We defined generations as the following ages in 2020:

The survey also included responses from the silent generation (ages 75 and older). However, their responses weren’t included in the generational breakdowns due to low sample size among that age group.

The survey was fielded Oct. 19-21, 2020.

Devon Delfino

Devon DelfinoDevon Delfino is an independent journalist with work featured in the Los Angeles Times, U.S. News & World Report, Teen Vogue, Forbes, MarketWatch, CNBC and USA Today, among others.

Read More