MagnifyMoney

In August, we published our study of America’s biggest boomtowns. It looked at three categories of data — industry growth, population and housing changes and workforce opportunities. As a follow-up to our study, we are providing a look at the top 50 metro areas that are attracting millennials and helping them prosper.

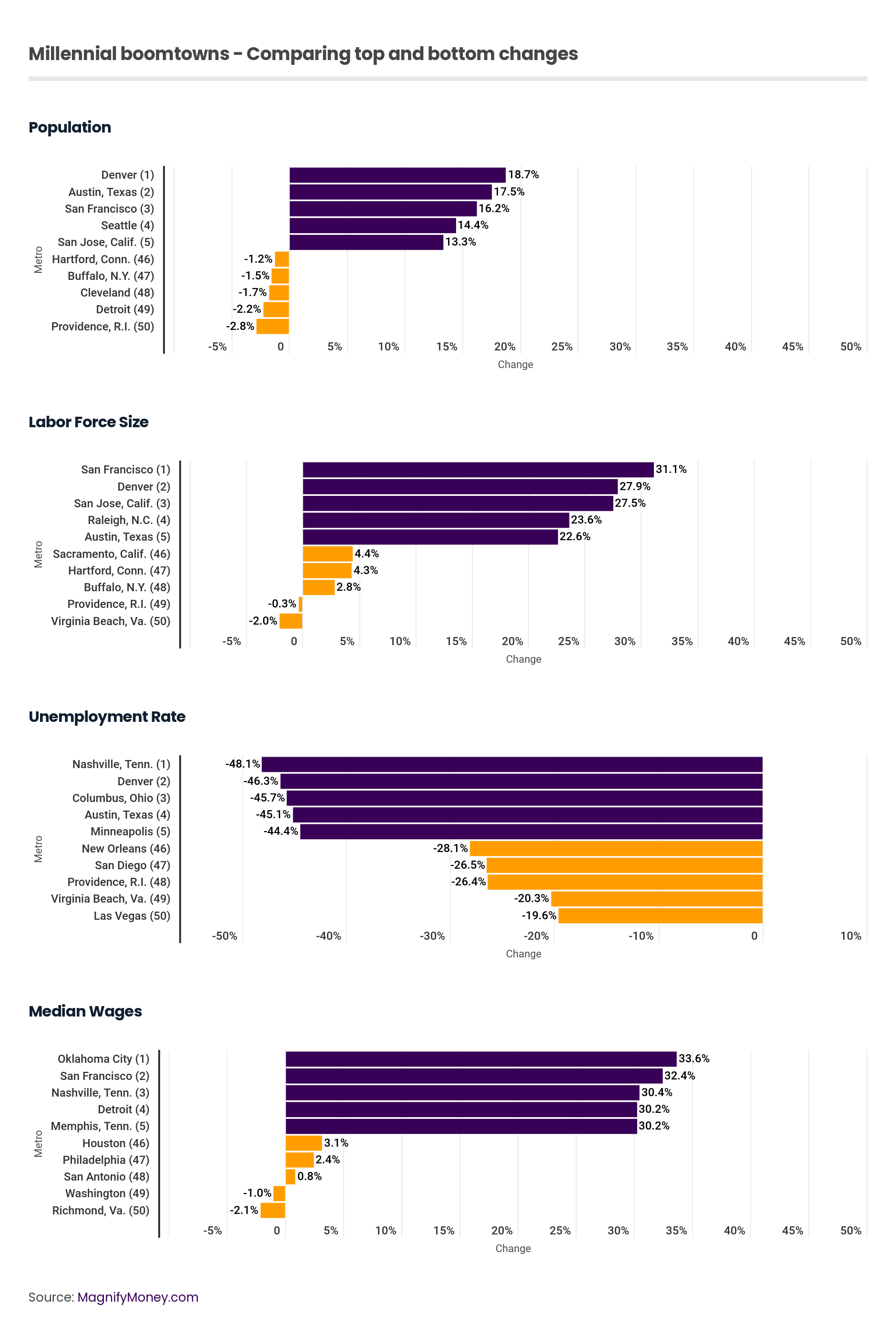

Using four metrics (millennial population change, workforce participation, unemployment rate and median wages), we scored the top 50 cities. A 100 was the highest possible score.

Here is a look at our findings.

Hover over a metro in the map below to see how it performed between 2011 and 2016.

Using the Pew Research Center’s definition of millennials (those born between 1981 and 1996) means that a portion of millennials would have been minors or pursuing an education or job training in 2011. To avoid including the working statistics of high schoolers, we limited this study to people born between 1981 and 1991, meaning people who would be between the approximate ages of 20 and 30 years old in 2011.

Even with that restriction, it’s important to remember that in general, people enjoy better employment opportunities and see higher wages as they gain experience, skills and workplace sophistication. Also, more people enter the workforce as they complete their educations, which often happens in their early 20s. Therefore, at least some of the increases in workforce participation and earnings are due to the natural age progression of this cohort.

Even so, we find that the millennial population is growing – and prospering – more in some places than in others. Millennials who live in the metros at the bottom of our list may be at risk for accruing more debt and less wealth over their lifetimes, thanks to opportunity losses. Those who move to the cities at the top of the list may find that they’re better equipped to pay down debt and gain assets at a faster rate as they gain toeholds in more lucrative job paths.

We tracked the five-year (2011-2016) population changes of those born between 1981 and 1991. Interestingly, millennial populations actually decreased in nine of the 50 metros we analyzed, which demonstrates that many millennials are actively migrating.

It’s a truism in economics that when local working conditions and opportunities improve, many people who don’t participate in the workforce will decide that it’s a good time to pursue outside employment. Therefore, we wanted to see not just the change in overall population, but the change in the number of people who work or are actively seeking work. The size of the labor force generally increased, even in places where the millennial population shrank, except in Providence and Virginia Beach.

How much has the unemployment rate declined for millennials over that five-year period? Unemployment for the nation as a whole has dropped significantly since 2011, but there’s a big difference between the 19.6% drop for millennials in Las Vegas and the 48.1% drop in Nashville.

We calculated the change in median wages for those born between 1981 and 1996. As discussed above, we would expect wages to go up for this group, generally, simply because they aged and gained worked experience during the intervening years. However, we found that median wages actually dropped a smidge in Richmond, Va., and Washington, D.C.

| Rank | Metro | Final Score | Population Change | Labor Force Change | Unemployment Change | Median Wages Change |

|---|---|---|---|---|---|---|

| 1 | San Francisco | 89.0 | 16.2% | 31.1% | -40.3% | 32.4% |

| 2 | Denver | 80.6 | 18.7% | 27.9% | -46.3% | 13.1% |

| 3 | Austin, Texas | 80.0 | 17.5% | 22.6% | -45.1% | 21.7% |

| 4 | Nashville, Tenn. | 76.4 | 11.4% | 16.7% | -48.1% | 30.4% |

| 5 | San Jose, Calif. | 74.7 | 13.3% | 27.5% | -37.2% | 25.9% |

| 6 | Raleigh, N.C. | 69.8 | 12.7% | 23.6% | -39.0% | 22.7% |

| 7 | Portland, Ore. | 69.5 | 11.3% | 18.8% | -40.3% | 28.3% |

| 8 | Seattle | 65.1 | 14.4% | 19.9% | -40.6% | 15.4% |

| 9 | Oklahoma City | 59.4 | 8.2% | 6.6% | -40.3% | 33.6% |

| 10 | Dallas | 57.4 | 9.4% | 17.3% | -42.3% | 14.8% |

Final score: 89.0

Housing is a struggle in San Francisco, but that isn’t deterring millennials. While the overall population of millennials increased by 16.2%, the millennial workforce jumped by 31.1%. To put that into context, the workforce increase represents about 5,000 more people than the population increase. That could be because so many people in the Bay Area have secondary and advanced degrees, meaning they may not have entered the workforce until they were well into their 20s, or may have dipped out of the workforce to further their education.

The unemployment rate for millennials dropped 40.3%, which is fairly impressive. That still only put San Francisco at No. 15 for highest unemployment rate drop among millennials. Fourteen other metros had bigger drops, including Detroit (42.9%), Minneapolis (44.4%), and Columbus, Ohio (45.7%).

But for millennials who are working, median wages have skyrocketed 32.4%, to $40,304. That’s the second highest wage on our list after neighboring city San Jose, and the second largest wage increase after Oklahoma City.

Final score: 80.6

Denver boasts the biggest increase of the millennial population between 2011 and 2016, at 18.7%.

Its 27.9% increase in labor force is second to San Francisco. But about 13,000 of the new arrivals aren’t working or are looking for work. That may be because despite the second sharpest drop in millennial unemployment (46.3%), median millennial wages have only increased 13.1%, to $32,243. That increase is the 15th smallest jump on our list.

Final score: 80.0

Austin has changed immensely in recent years. It has seen a population explosion over the last few years, and millennials were certainly part of that burst. Their numbers increased by 17.5%, the second biggest gain on our list behind Denver.

Despite an impressive workforce gain of 22.6% (5th highest), more millennials simply moved to Austin over joining the workforce. However, that’s not surprising for a major university town with extensive graduate and undergraduate programs.

Further, unemployment dropped 45.1% for millennials — the fourth biggest decline on our list — and median wages increased 21.7%, to $30,228.

Final score: 76.4

Nashville seems eager for new millennial employees, as demonstrated by the biggest drop in unemployment of any metro on our list (48.1%). The city also has the 6th lowest millennial unemployment rate (5.3%). Overall, the millennial population increased by 11.4% (9th highest), and the labor force rose by 16.7% (15th highest).

Although Nashville also saw the third highest median wage increase (30.4%), that still only increased median wages up to $29,220. That median wage puts Nashville in the middle of the pack in terms of absolute dollars.

Final score: 74.7

The seat of Silicon Valley is the first place on our list where more millennials entered the labor force than actually moving into the metro. The millennial population increased by 13.3%, and 27.5% more are working or looking for work. That comes out to a difference about 4,000 people.

That’s somewhat surprising considering the relatively mediocre millennial unemployment rate of 6.7% (18th lowest) and comparatively modest median earnings increase of 25.9% (10th highest on the list). Of course, millennials in this city see the highest earnings of any metro on our list, with a median wage of $42,319.

| Rank | Metro | Final Score | Population Change | Labor Force Change | Unemployment Change | Median Wages Change |

|---|---|---|---|---|---|---|

| 50 | Virginia Beach, Va. | 9.7 | 3.2% | -2.0% | -20.3% | 6.6% |

| 49 | Providence, R.I. | 13.3 | -2.8% | -0.3% | -26.4% | 9.9% |

| 48 | Philadelphia | 21.7 | 0.7% | 10.6% | -31.6% | 2.4% |

| 47 | Richmond, Va. | 26.3 | 3.9% | 12.4% | -32.3% | -2.1% |

| 46 | St.Louis | 26.8 | -1.1% | 6.0% | -32.6% | 14.2% |

| 45 | Phoenix | 27.7 | 5.3% | 8.6% | -29.9% | 6.2% |

| 44 | Cleveland | 27.7 | -1.7% | 6.7% | -35.5% | 11.3% |

| 43 | Riverside, Calif. | 29.5 | 0.6% | 4.5% | -32.3% | 18.7% |

| 42 | Buffalo, N.Y. | 30.3 | -1.5% | 2.8% | -35.6% | 18.7% |

| 41 | Sacramento, Calif. | 30.4 | 1.9% | 4.4% | -32.9% | 16.9% |

Final score: 9.7

Virginia Beach came in last on our list by performing dismally across all four metrics. The metro did enjoy a small bump (3.2%) of millennials between 2011 and 2016, but 2% fewer millennials were engaged in the labor force, the worst showing on our list. That could be because while the 7% unemployment rate isn’t the highest on our list (Riverside, Calif., takes home that honor), the 20.3% reduction was actually the smallest across the 50 metros.

Median wages for millennials have only increased 6.6%, which is 7th lowest among metros we reviewed, to $28,212. That median is distinctly middle of the pack, but the growth rate suggests there may be wage stagnation, as we would expect this age group to see wage gains just by moving from entry-level to more experienced levels over that five-year period.

Final score: 13.3

Providence saw its millennial population drop by 2.8%. Part of this may be attributed to the fact that Providence is a college town. Thus, this drop may represent millennial students who have moved on after completing their undergraduate and graduate degrees. However, we did find that this metro area had one of the smallest population increases in our previous study.

Similarly, the millennial labor force shrank by 0.3%. The high millennial unemployment rate of 8.5% (8th worst) may have something to do with that, along with the 11th lowest income increase (9.9%).

Final score: 21.7

Perhaps it’s no surprise that the millennial population of Philly only increased by 0.7%. Unemployment for that age group is 8.8% and median earnings only increased by 2.4%. That earnings increase represents a paltry five-year cost of living raise for most people.

The millennial workforce did rise by 10.6% during that period, however. It seems that local residents are picking up whatever new jobs are becoming available.

Final score: 26.3

Richmond has the ignominy of the worst wage change for millennials. Median earnings went down by 2.1%. Washington, D.C., was the only other metro to see a negative earnings change, at 1%, but still managed to rank 18th overall, thanks to strong showings in other categories.

Although Richmond has a respectable millennial unemployment rate of 7.6%, an unemployment decrease of 32.3% was 12th lowest on our list and thus didn’t earn many points. A workforce increase of 12.4% was dead center of the pack, and the millennial population growth of 3.9% ranked 32 out of 50.

Final score: 26.8

St. Louis saw its millennial population shrink by 1.1%. Workforce participation was up by 6% (40th out of 50), but some or all that can probably be attributed to young adults entering the workforce after school or training, rather than attractive economic conditions.

Even though median earnings in 2016 were the 16th highest at $30,228, the earnings increase of 14.2% ranked 33rd highest on the list of 50. Despite these findings, a March 2018 study we conducted found that St. Louis was one of the best places for working women.

Using data from the U.S. Census American Community Survey, hosted on American FactFinder and by IPUMS USA, we tracked the five-year change between 2011 and 2016 (the last year for which all data was available) for those born between 1981 and 1991. This represents a subset of millennials, who are generally defined as those born between 1981 and 1996 (the reason for limiting the population to this subset is described above). These millennials would have been between the approximate ages of 20 and 30 in 2011 and 25 and 35 in 2016.

We limited the review to the 50 largest metropolitan statistical areas (“MSAs”) due to limited data availability.

The analyzed metrics were:

Because the U.S. Census has changed the boundaries of some MSAs in the intervening years, we collected the data from FactFinder at the county level and then mapped it to the current MSA borders.

Each data series was scored relative to the other metros so that the biggest positive change received a score of 100 and any 0 or negative changes received a score of 0 (except for unemployment rate, where this was reversed). The highest possible score for each metric was 100 and the lowest was 0. The four metric scores were then summed and divided by four for a final score. The highest possible final score was 100 and the lowest was 0.

Kali McFadden

Kali McFaddenKali McFadden is a senior research analyst at LendingTree and MagnifyMoney based in Charlotte, N.C., where she conducts data-driven studies of issues related to personal finance and economics.

Read More