MagnifyMoney

What it means to be retired in America may look differently than we imagine, as more than 6 in 10 Americans think they’ll keep working after retirement, according to the latest MagnifyMoney survey.

The financial impact of the COVID-19 crisis may lead to more unemployment, households borrowing money from their retirement savings to cover expenses and Americans rethinking how they can retire comfortably.

MagnifyMoney surveyed more than 2,000 Americans — nearly 1,700 of which haven’t already retired — to learn how people are envisioning retirement. This, in many cases, still involves working to some extent.

While it seems like a bit of an oxymoron to be retired and still working, those who will continue to work after retirement will likely have a vastly different work life than they did pre-retirement.

They may choose to work part time in a service field such as retail or in their former industry as a consultant or freelancer. Some may choose to monetize a hobby, such as teaching yoga, or start their own business.

There wasn’t a huge generational divide when it came to planning to work less during retirement. Generation Z (47%) was the only group that was far less likely to believe they’ll keep working after retirement, compared with:

Sarah Berger, MagnifyMoney’s millennial finance columnist, said one potential reason that Gen Zers might not feel like they’ll have to keep working after retirement could have to do with their level of financial literacy.

“Younger generations have less experience managing their finances, and older generations likely have a more realistic picture as to how much money they will actually need to retire, and the amount of money that they will need to live comfortably within retirement,” Berger said.

Household incomes appeared to have a stronger impact on retirement plans than age. Respondents within the highest income category — $100,000 or more — were most likely to plan to work after they retire (80%).

While it’s difficult to say why this may be, it could be because high-income earners are accustomed to maintaining a more expensive lifestyle. Or, their career paths can lead to more appealing options for working post-retirement, such as part-time consulting within their industry.

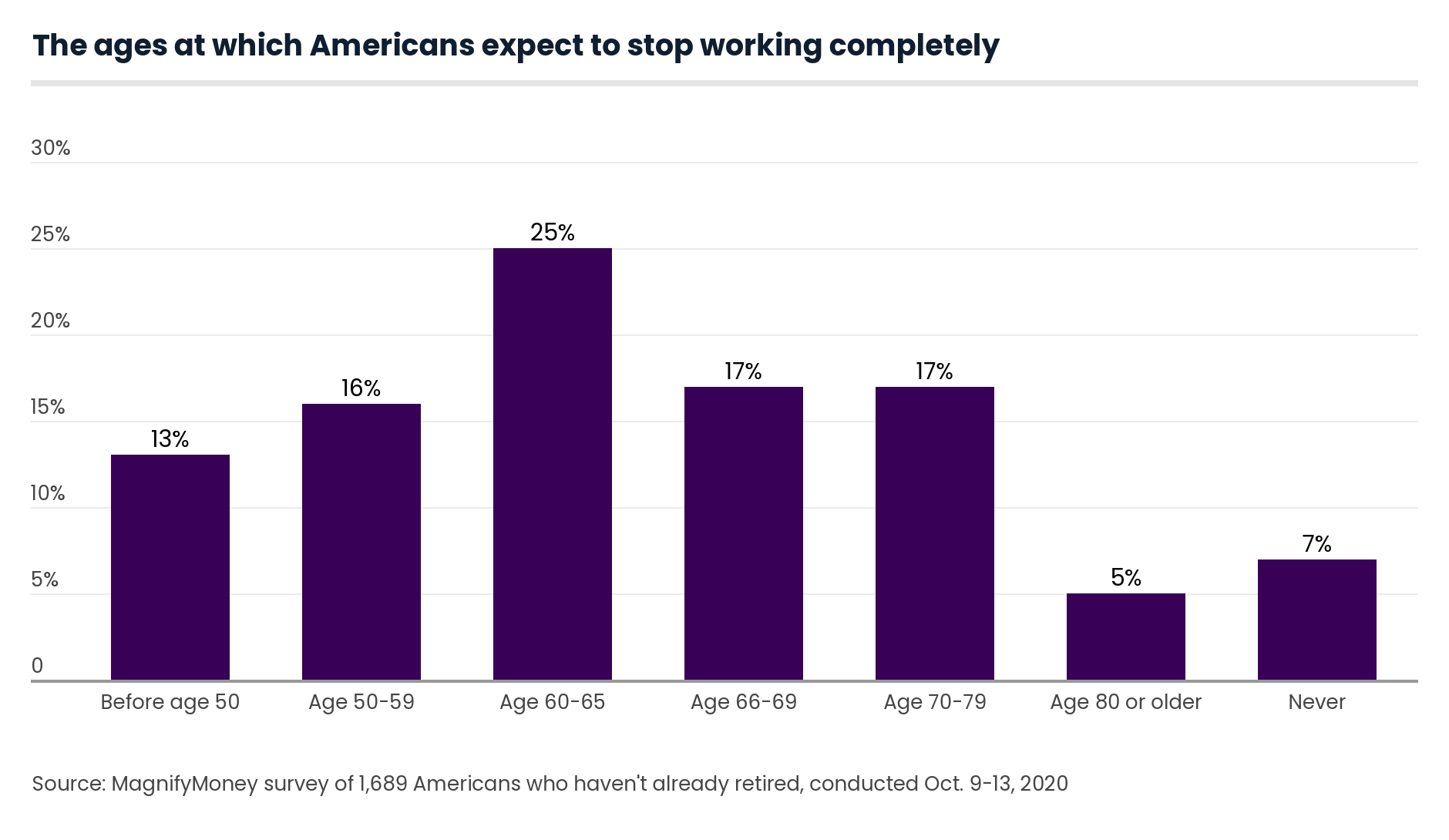

While 7% of American don’t think they’ll ever stop working, a more promising 25% of Americans do think they’ll be able to retire between 60 and 65. Meanwhile, 17% of Americans expect to retire between 66 and 69.

There appears to be a gender divide when it comes to planning when to stop working. While 23% of women think they’ll retire between 66 and 69, only 11% of men said the same. More men think they’ll retire between 60 and 65.

Respondents that have a household income of $100,000 or more were the most likely group (29%) to expect to retire between 60 and 65.

Even though someone is retired and not working, that doesn’t mean there may not come a day when they feel the need to return to work for either financial or personal reasons.

Even though 67% of retired Americans aren’t considering a return to work, it’s still impactful that 33% of retired individuals are either continuing to work during retirement or are thinking about beginning working again.

More men than women are either working during retirement or are considering returning to work post-retirement in some manner. In fact, 15% of men are working during retirement, compared with 12% of women. And 23% of men are considering continuing to work in some form, versus 18% of women.

It’s worth repeating that this portion of the survey is based on the responses of 332 Americans who identified as retired.

While 57% of Americans who think they’ll keep working after retirement reported this will likely be because they need to earn more income, 44% of respondents named curing boredom as their motivation.

Other respondents listed other reasons for planning to work during retirement, such as:

Older Americans who plan to keep working after retirement mainly said they’d do so because they’d need the money:

Meanwhile, Gen Zers predominately said they’d be bored otherwise (59%).

While more than 1 in 2 of those who make $100,000 a year or more said they’d do so because they need the money, nearly 1 in 5 said they truly love their career and want to continue.

By contrast, 71% of those who make less than $25,000 and plan to keep working would do so for the money, while just 6% said they’d do so because they love their career.

Alongside uncovering why people want or need to keep working during retirement, MagnifyMoney also investigated why some wouldn’t want to continue working during that stage of their life.

The main motivation to stop working? Family. In fact, 51% of respondents reported wanting to have more time to relax and spend with family as a motivation for retiring fully.

More than 2 in 10 (21%) respondents believe they’ll have enough money saved to replace any lost income and won’t need to work past retirement. In particular, 31% of men reported feeling financially confident enough to retire fully, compared with 14% of women.

When it comes to working post-retirement, what that work looks like can vary greatly.

Those who think they may continue working after retirement would be most likely to pursue part-time work in a service field such as grocery or retail (33%), followed by:

Of the Gen Zers who think they’ll keep working after retirement, 20% would do so by starting their own business, which they reported more than any other generation. Meanwhile, 16% of millennials agreed, but only 8% of Gen Xers and 5% of baby boomers felt the same way.

Gen Zers were also most likely to say they’d monetize a hobby (28%), versus:

For those who want to retire fully, there are steps they can take that can help them prepare for a comfortable retirement and ensure they don’t need to work during that stage of their life. Here are a few best practices for preparing for a happy retirement, via Berger.

MagnifyMoney commissioned Qualtrics to conduct an online survey of 2,021 Americans, with the sample base proportioned to represent the overall population. Of the total sample size, 1,689 respondents identified as not retired and 332 identified as retired. The survey was fielded Oct. 9-13, 2020.

Generations are defined as the following ages:

Jacqueline DeMarco

Jacqueline DeMarcoJacqueline DeMarco is a freelance writer who is particularly passionate about finance. She began her career in the retirement industry. Today, she works with more than a dozen financial brands to create entertaining and educational money content.

Read More