MagnifyMoney

When the holiday season ends, you take down your festive decorations, ease back into work and resume life as normal. But for many Americans who rack up debt during the most wonderful time of the year, the holidays aren’t over until the bills are paid off.

Americans took on an average of $1,325 of holiday debt in 2019, according to a survey conducted by MagnifyMoney. The vast majority of respondents won’t be paying off their holiday debt by January.

It should come as no surprise that consumers are taking on holiday debt again, considering our survey findings from years past. Holiday debt rose 8% this year, from $1,230 in 2018 to $1,325 in 2019. Since we first conducted this survey in 2015, holiday debt has risen 34%.

For the purposes of our survey, holiday debt includes any seasonal costs, such as Christmas gift-giving, plane tickets for traveling home or groceries for Hanukkah dinner. Gift-giving (and, by extension, retail spending) is a large component of holiday debt. The industry trends of rising retail sales may contribute to the increase in holiday debt represented in our survey, which was fielded from Dec. 20 to Dec. 23.

Holiday retail sales grew 3.4% this year, while online sales grew 18.8%, according to Mastercard SpendingPulse™, a market intelligence service. SpendingPulse monitored sales activity from Nov. 1 to Dec. 24 across Mastercard accounts to compile its data.

Debt amounts were clearly split among generational lines:

Keep in mind that just because baby boomers only took on $606 in holiday debt this year doesn’t mean that they spent less this holiday season. It just means that they assumed less debt in doing so. They could have saved throughout the year or dipped into cash or savings to pay for holiday-related expenses.

Besides taking on less debt, older generations are more likely to pay off their debts sooner than their younger counterparts. Baby boomers are most likely to pay off their debt within one month, while millennials are most likely to just pay the minimum balance on their accounts.

Across gender lines, men were heavier spenders. Men assumed $1,450 in holiday debt, about $250 more than women.

A large majority of respondents (78%) said that they won’t pay off their holiday debt by January. This is a daunting prospect for credit card and store card users in particular, who will accrue interest unless they pay off their purchases when the statement balance is due.

Just 22% of respondents will pay off their debt within one month.

For the 15% of consumers who will only make the minimum payments on their holiday purchases, it could take months or years to pay off that debt. These borrowers will also pay the most interest on their purchases in the long run.

It would take more than five years to pay off $1,325 making minimum monthly payments of $30 with an interest rate of 15.1%. Plus, you’d be paying more than $600 in interest by the time you’re done paying down debt, years after the holiday has ended.

We used 15.1% because that is the average interest rate across all open accounts, according to the Federal Reserve. But holiday debt could take even longer to pay off (and cost more), since 36% of survey respondents said they’re paying an interest rate of 20% or more.

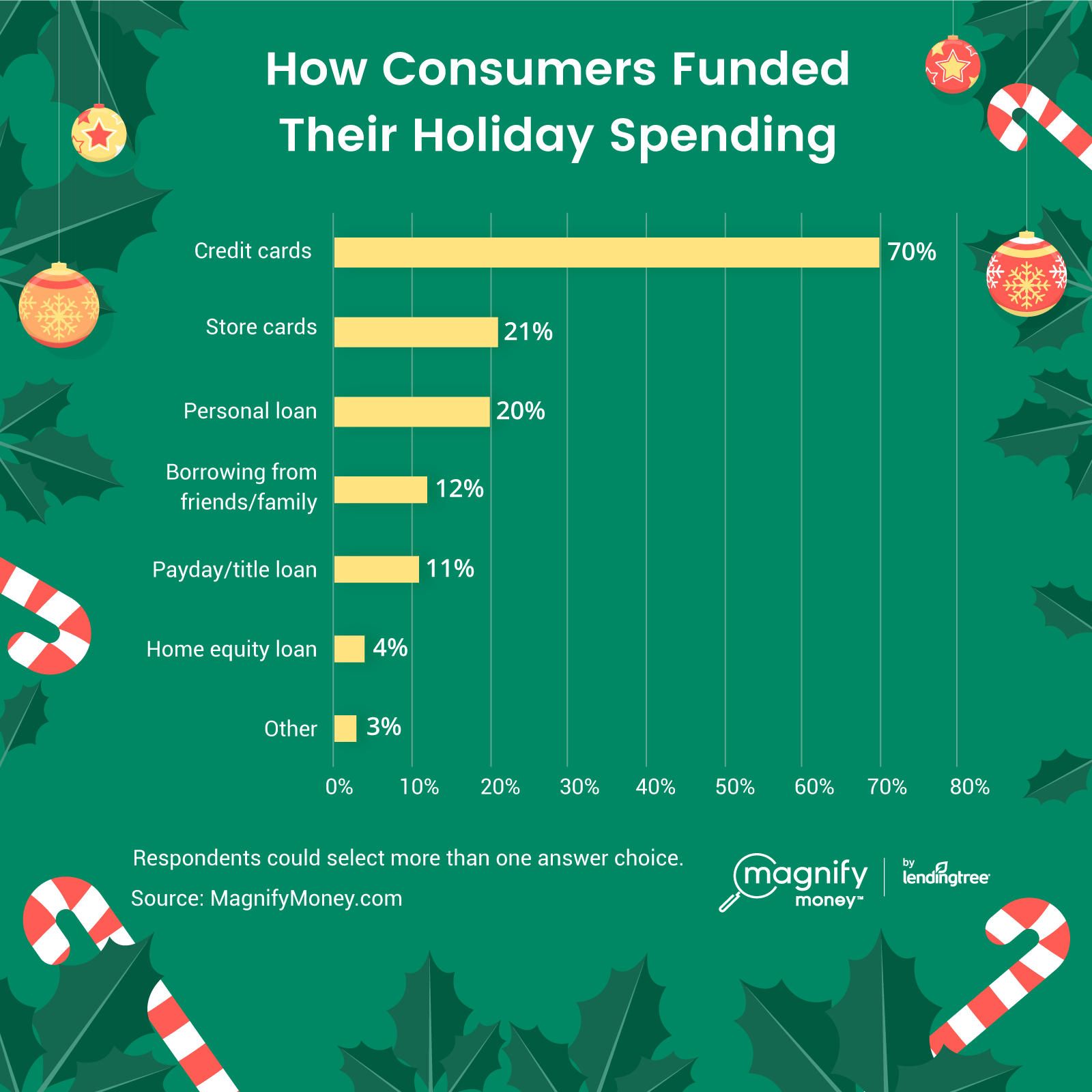

American families rely on credit cards to make Christmas miracles happen. Seventy percent of respondents funded their holiday spending with credit cards, about the same as last year. Plus, 21% of those surveyed used store cards.

More people are leaning on personal loans to cushion their holiday spending. Twenty percent of respondents used personal loans this holiday season, up from 14% in 2018 and 9% in 2017. So in the span of two seasons, consumers doubled their holiday usage of personal loans.

The use of store cards more than doubled from 10% in 2018 to 21% this year, despite the fact that these cards typically carry higher APRs.

The average store credit card APR is 25.41%, according to CompareCards, which, like MagnifyMoney, is owned by LendingTree. So consumers who don’t pay off their holiday debt by the time the statement is due risk paying much more than the value of the items they bought if they don’t pay off the store card on time.

A LendingTree survey released in early December found that 61% of Americans were dreading the upcoming holidays due to spending. About the same amount of our survey’s respondents (58%) reported being stressed about their holiday debt.

Millennials and Gen Xers reported the most debt-related stress at 68% and 63%, respectively, compared with just 37% of baby boomers. It’s worth reiterating that baby boomers have the least amount of debt, at $606, perhaps contributing to lower stress levels.

Despite the fact that many spenders are stressed about their holiday debt, more than half of them won’t try to consolidate debt or shop around for a better interest rate. Many simply don’t want to bother with another bank.

MagnifyMoney commissioned Qualtrics to conduct an online survey of 1,120 American consumers. The survey was fielded Dec. 20-23, 2019.

Erika Giovanetti

Erika GiovanettiErika Giovanetti is the debt and personal loans writer for LendingTree. She has reported on a multitude of subjects, from personal finance to human interest to politics.

Read More