MagnifyMoney

When you’re young and just starting out your career, choosing where to live can truly make or break your finances.

Young people today already have to manage a host of financial stressors, like student loan debt and rising housing costs, with the usual demands of early adulthood, like starting their first retirement fund and learning to balance work and play.

When you couple these competing responsibilities with a location that only contributes more financial obstacles, you could be setting yourself up for failure.

On the other hand, some cities are affordable enough to give even the lowest earners a fighting chance at a decent quality of life.

With this in mind, MagnifyMoney decided to take a look at some of the biggest cities in the U.S. and determine which cities are the best places to be young and broke today.

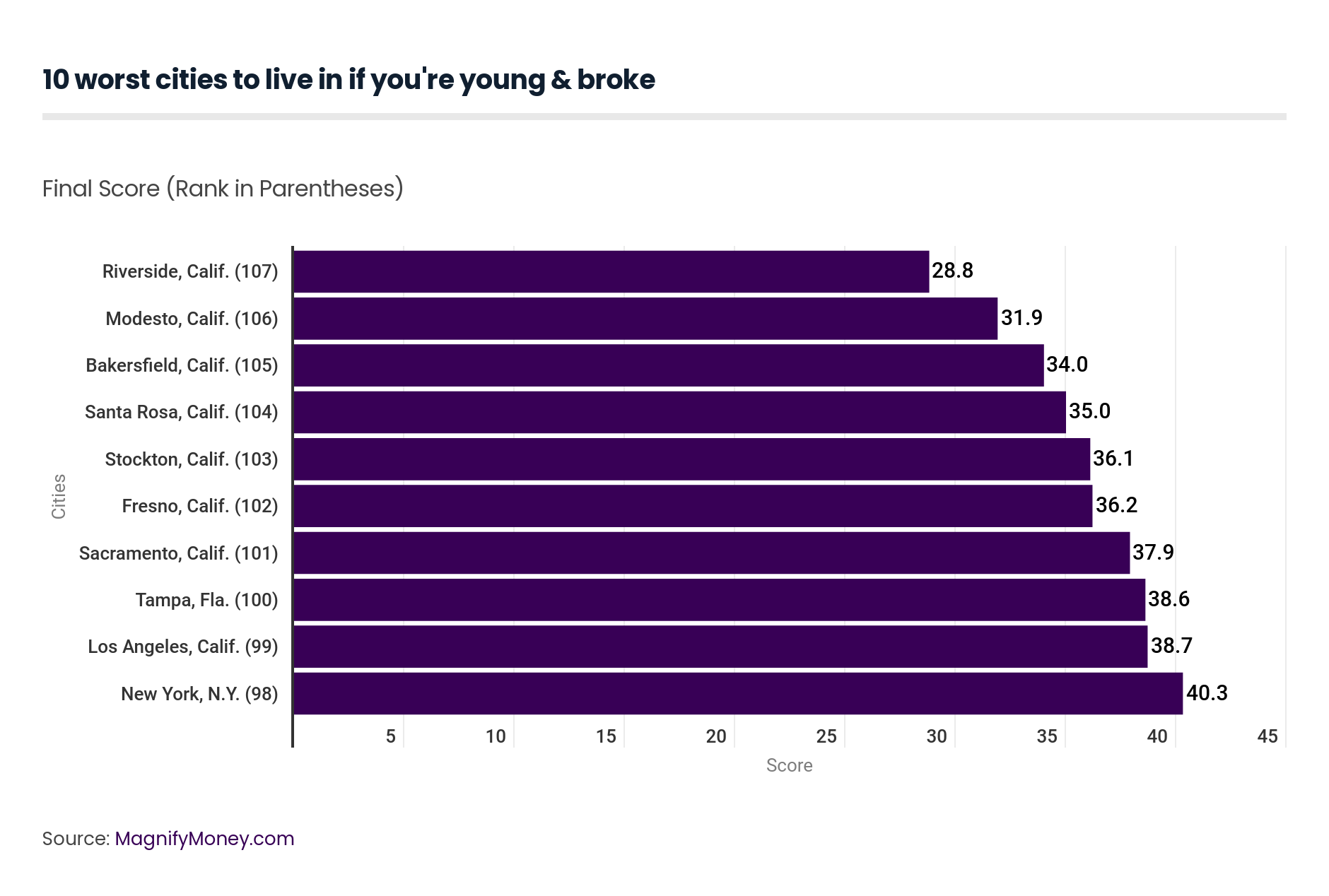

We started by analyzing more than 100 U.S. cities to find the most favorable and affordable places for people between the ages of 18 and 24. Among other data points, we not only looked at obvious expenses like housing and food, but also unemployment rates, income taxes and the rate of young adults who are living in poverty.

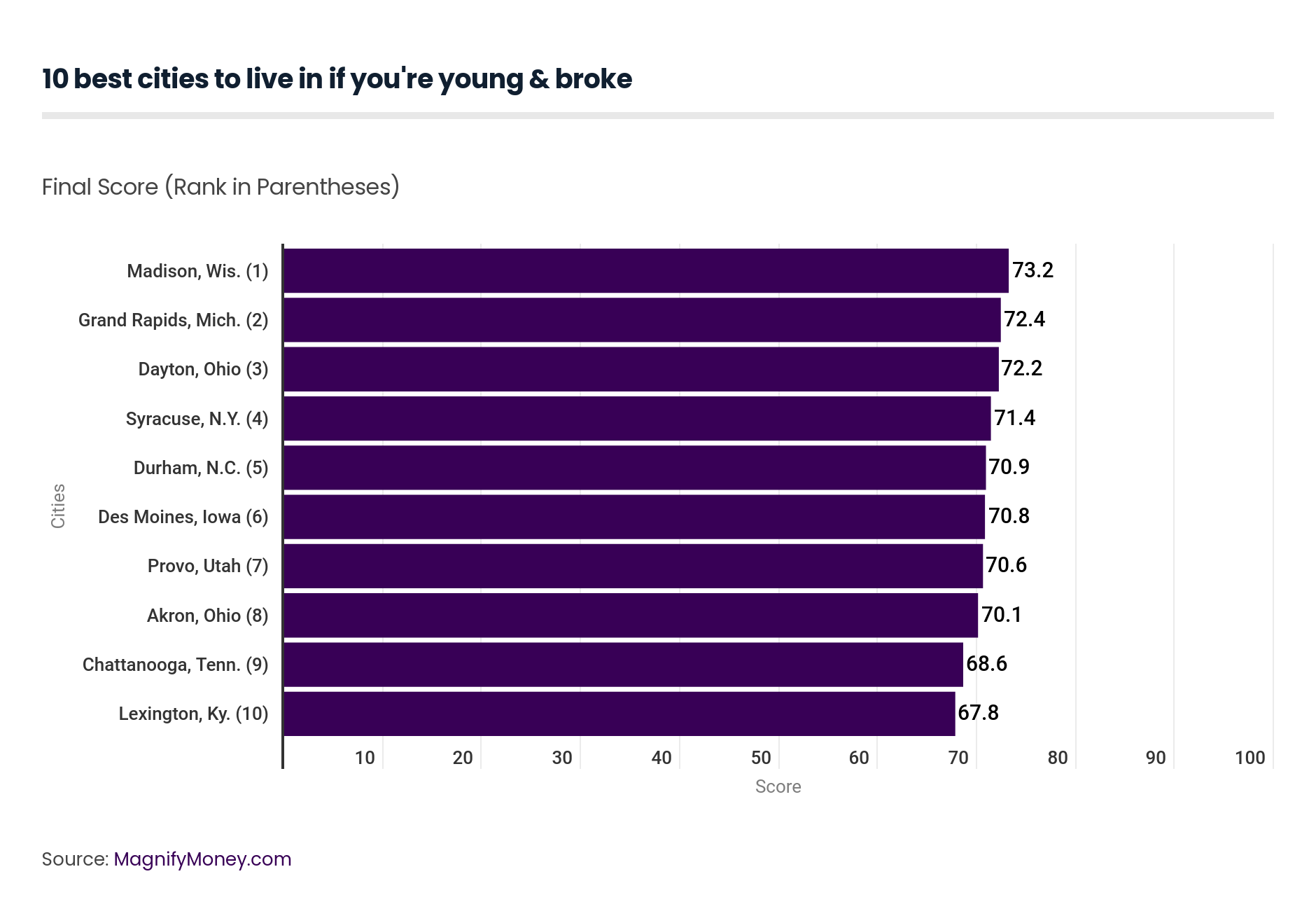

Of the 10 best places to make the most of a tight budget, five were in the Midwest — Madison, Wis., Grand Rapids, Mich., and Dayton, Ohio.

Although Midwestern cities did not score highest on all of the features analyzed, when they were put up against what young adults said matters to them the most, low rents and short commute times pushed these places ahead.

“It’s not that these cities necessarily scored the highest on all the features we analyzed, but when we weighted those features according to what the young adults we surveyed said mattered the most, the lower-than-typical rents and price combined with modest commute times to bring Midwestern cities to the top of the list,” said MagnifyMoney Senior Research Analyst Kali McFadden.

Overall score: 73.2/100

It stands to reason that a renowned university town would be a draw for the young and broke, but Madison stands apart, thanks to a relatively low cost of living (median rent is $950, and goods run almost 5% cheaper than the rest of the country) and a fairly robust public transportation system.

About 4% of the population use public transportation, which may not seem like a lot, but that’s enough to rank 21 among the cities reviewed. Moreover, the average commute is just over 21 minutes.

Only two other cities (Provo, Utah and Springfield, Mass.) have a higher proportion of young adults, yet no other big city has more young people who either attended or graduated from college (70%), and the city ranks in the top 10 for lowest youth unemployment.

The bad news is that there are more young adults living in poverty in Madison than other city analyzed, but this may have to do with how college students and their families file their taxes. When considering what city features young people in our survey said they care most about, Madison still places 1st, with an overall score of 73.2.

Overall score: 72.4/100

With an overall score of 72.4, Grand Rapids misses 1st place by a hair. Grand Rapids shines in many of the same ways that Madison does, such as the price of goods, relative to the rest of the country (almost 5% less), average commute time (just over 21 minutes) and low youth unemployment rates (6.7%).

Grand Rapids is also full of young, educated citizens, with over 10% of the population between the ages of 18 and 24, and 59% of those young people either college graduates or on their way. Most young people are local, with fewer than 5% newly arrived from out of state.

Fewer than 2% of people use public transportation, which is pretty middle-of-the-pack, and statewide and income taxes are lower than most, ranking 42nd and 44th out of the 107 big cities. Grand Rapids exceeds Madison in a few areas, such as median rent at $812, fewer young people in poverty and over twice as many pizza joints per capita.

The other Midwest cities that made the top ten were Des Moines, Iowa (6) and Akron, Ohio (8).

Overall score: 72.2/100

It turns out that Ohio is a great place to be young and broke. Statewide, income and sales taxes are low, ranking 23rd and 33rd among the 107 big cities we reviewed, and Dayton’s modest median rent ($761) and low cost of goods (over 4% cheaper than the national average) add to Dayton’s affordability.

Of the 10% of Dayton’s young population who are between the ages of 18 and 24, 63% have or are working toward an undergraduate degree (13th highest). Average commute times also compare favorably with the rest of the nation, coming in at just under 23 minutes. Dayton does fall short in the areas of youth unemployment (11%) and youth living in poverty, ranking in the bottom half of all cities we reviewed.

Overall score: 71.4/100

Our first city outside of the Midwest is another university town in the northern reaches. With a score of 71.4, Syracuse compares very favorably with the rest of the country in average commute times (21 minutes), statewide sales tax (4th lowest), and percentage of the population between the ages of 18 and 24 (11%).

As one would expect for a college town, a lot of young adults are newly arrived from out of state or country (11%), and Syracuse ranks 11 out of 107 for number of young people who attend or have graduated from college (64%).

Rents are low at $790, as is youth unemployment (8%), but as seen with the other top cities on our list, a lot of young people live below the poverty line (26%).

#5 Durham, N.C.

Overall score: 70.9/100

Durham-Chapel Hill is home to two large schools, Duke University and University of North Carolina, which helps explain why over 11% of the population is between the ages of 18 and 24.

It also helps to explain why 68% of those young adults either have or are pursuing a college degree (the 3rd largest proportion in our study), and why 11% of them arrived in the last year from another state or country. Durham is also relatively affordable, with a middle-of-the-pack median rent of $947 and prices almost 4.5% lower than the national average.

Commute times are also middle of the pack at under 25 minutes, but almost 5% of the population use public transportation. Again, 5% may not sound like a lot, but it’s actually the 15th highest among cities with populations over half a million. Some 30% of young people live below the poverty line, although that may be because so many college students don’t have much, if any, income.

It’s not all roses in the Midwest

Ironically, the best five cities for the young and broke also have a high rate of young adults living in poverty, comparatively. As we said, the reason these cities have an edge is that they tended to rank well in the factors that young people said mattered most to them, like rent costs and commute times.

Top-ranked Madison, Wis., for example, also boasts the highest rate of young adults living in poverty in Madison than any other city analyzed. Similarly, in Durham, N.C (5), 30% of young people live below the poverty line.

However, this doesn’t necessarily mean these cities are rife with homeless young adults. One explanation could be that these cities are home to several colleges and with a high volume of college students in the population, it’s easy to see how it could appear that young adults aren’t earning much.

“These two things are likely connected, as college students often have little or no income, but that doesn’t mean they’re not being supported through family assistance or loans,” McFadden said.

On the plus side, college towns are affordable

The list also boasts a number of college towns like the aforementioned Madison, Wis. (1) and Grand Rapids, Mich. (2). Rounding out the top five were college towns outside of the Midwest, Syracuse, N.Y. (4) and Durham, N.C. (5). The results suggest college towns may be more affordable destinations for young people who want to keep their expenses relatively low.

To find city features most appealing to young people without a ton of disposable income, MagnifyMoney asked 100 young people (ages 18-24) to rank the importance of 12 city features that factor into quality of life for the young and broke. The responses were weighted according to which were the most important to the youth surveyed.

Here are the most important city features, according to this survey:

Once we know what to look for, our team weighted the features of 107 metro areas with populations over 500,000 against what young people said they wanted most in the city.

Based on this information, the cities were then scored, for a highest potential score of 100 and a lowest potential score of zero to find the best places for broke young adults.

Brittney Laryea

Brittney LaryeaBrittney Laryea is a personal finance writer for MagnifyMoney.com. She recieved her bachelor’s degree from the University of Georgia in digital and broadcast journalism and digital marketing.

Read More