MagnifyMoney

In a new study, MagnifyMoney researchers sought to find out which state is home to the happiest people.

The methodology was inspired by a recent Oxford Economics study of the components of well-being, in which researchers found sleep is the largest factor contributing to well-being, followed by other health, lifestyle and economic factors.

In line with the Oxford team’s findings, MagnifyMoney evaluated how each of the 50 states rank on 20 factors in the categories of health, lifestyle, and prosperity. Based on an analysis of those elements, our study found the state where you live may impact your baseline level of happiness.

Minnesota is the happiest state. Minnesota didn’t rank highest in either of the three categories, but it ranked highest overall. The home of the Mall of America scored an overall 73.3 out of 100. Minnesota ranked third in health, third in lifestyle and sixth overall in prosperity. Minnesota is trailed by South Dakota with an overall score of 72 and Colorado with 70.5.

Midwesterners are generally happier than people living in the South. Of the top ten happiest states in our ranking six of them — Minnesota, North Dakota, South Dakota, Wisconsin, Nebraska, and Iowa — are in the Midwest. And of the top ten unhappiest states, seven of the states — Louisiana, Alabama, Mississippi, Kentucky, Arkansas, Tennessee and Georgia — are in the South.

No. 1 in health: South Dakota. South Dakota ranked first in the health category and second overall in prosperity after weighing all factors. Boosting the state’s ranking was its first-place rank in the percentage of people who get at least seven hours of sleep. South Dakota ranked sixth in the state health index. The state landed 20th in lifestyle, which brought it down just below Minnesota to the number two spot overall in our happiest states ranking.

No. 1 in lifestyle & prosperity: Utah. Utah was top in both lifestyle and prosperity in our analysis. In the lifestyle category, Utah had the third lowest divorce rate and ranked first in volunteering (43.20%), beating out Minnesota by nearly 10 basis points. In prosperity, the state ranked tenth overall in homeownership (71.87%) and had the fifth lowest unemployment rate at 4%.

However, the state ranked ranked among the bottom 10 states in depression, suicide rate and air quality. It ranked 48th, 46th and 47th in each factor, respectively, bringing its ranking in the health category down to 21st overall and thwarting its shot at No. 1.

Louisiana is the unhappiest state

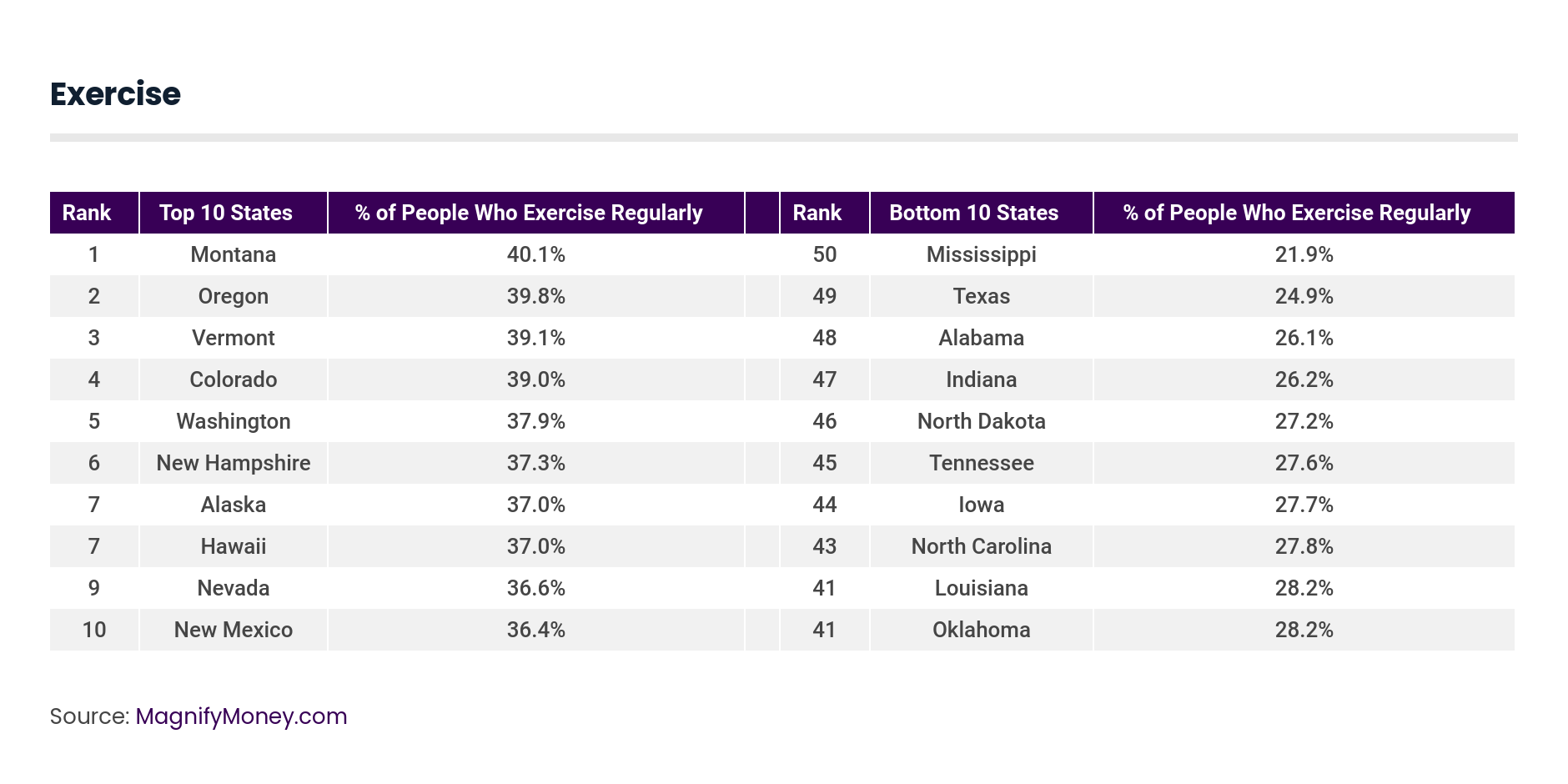

According to our findings, Louisiana was the unhappiest state to live in, with an overall score of 29.8. The state was weighed down by its bottom ranking in both lifestyle and prosperity factors, although it ranked a little higher in overall health. In lifestyle the state ranked 50th in the percentage of people married with and without children. In health the state ranked 50th again in volunteering (18.40%) and 42nd overall in the percentage of people who exercise (28.20%).

In prosperity, Louisiana ranked 49th in the percentage of people with a late payment in their credit history and an unemployment rate of 7.10% landed Louisiana 41st place in that category. Louisiana ranked 47th in median household income with an average of $45,146.

Rhode Island and West Virginia preceded Louisiana to round out the top three unhappiest states. What’s bringing these states down? Rhode Island ranked 49th in lifestyle and West Virginia ranked 49th in the health category.

As the Oxford researchers found, focusing on sleep, health, lifestyle and prosperity can lead to a life of wellness.

“Happiness comes when you’re thriving in your relationships, career, finances, health and in your engagement with your community,” said Victoria Craze, co-founder and life coach at Wellbeing Coaches.

Of course, that can be easier said than done. Only about 7 percent of people worldwide thrive in all areas of wellness, a 2010 study found.

Each of the key elements of happiness are related, however, so even making changes in one area may benefit you in others, Craze noted. To get enough sleep, for example, exercise is helpful, which can also have good long-term health effects. For stress, exercise again is a recommendation as well as eating healthier and practicing breathing techniques such as meditation. And to be more active, Craze recommended an effort to walk a bit more than you already do.

“Any additional movement do each day is a good thing that can help improve your well-being over time,” said Craze.

Using the Sainsbury’s Living Well Index (September 2017) from Oxford Economics analysis of well-being in Britain as a broad guide, we used 20 factors in the categories of health, lifestyle, and economic for each of the 50 states. Health and lifestyle factors had double the weight of economic stability, and within health, sleep was weighted three times higher than the other factors.

Health:

Lifestyle:

Economic Stability (Prosperity):

Sources include the U.S. Census Bureau, the Centers for Disease Control and Prevention, the Environmental Protection Agency, the Bureau of Economic Analysis, Gallup Inc., Blue Cross Blue Shield, Corporation for National and Community Service, Project: Time Off, and STAT News.

Media contact: Kellie Pelletier/Kpelletier@magnifymoney.com

Brittney Laryea

Brittney LaryeaBrittney Laryea is a personal finance writer for MagnifyMoney.com. She recieved her bachelor’s degree from the University of Georgia in digital and broadcast journalism and digital marketing.

Read More