MagnifyMoney

You said “I do,” but now you don’t. Divorce can certainly take a toll on one’s emotions, but it’s the long-term financial toll that may come as a surprise. Sure, there are immediate costs, such as legal fees and moving expenses, but the impact on one’s retirement savings and overall financial health may reverberate well into the future.

How much of an impact? A new study from MagnifyMoney analyzing Federal Reserve data found that married couples are much more prepared for retirement than their divorced peers. In fact, divorced people are 23% more likely to have nothing saved for retirement.

Can divorce tarnish one’s golden years? Financially, perhaps. Our study found that divorced people are far less prepared for retirement than their married counterparts.

In fact, 54% of divorced or separated people report having no money saved for retirement at all. Of those who do, they’ve only saved an average of $37,000 in retirement, savings and investment accounts combined. Compare that to the average of $141,225 that married couples have saved in the same accounts, and the gap is wide.

However, just because married couples are more prepared for retirement in general than their divorced peers doesn’t mean they’re well prepared. In fact, 44% of them have nothing saved for retirement.

Neither group is particularly optimistic that they’ll have enough saved by retirement either, but married couples are more confident:

They may be right, too. Our study found that married couples said they need $1.7 million to retire, while divorced or separated people said they need nearly $1.2 million. Both groups have hefty gaps between those amounts and the funds they have saved.

Once again, that gap is larger for divorced people. Our study found the retirement funding gap for married couples to be 34%, while divorcees had a retirement funding gap of 75%.

The average household income for married couples was $147,365, compared with the average divorced person’s income of $73,308.

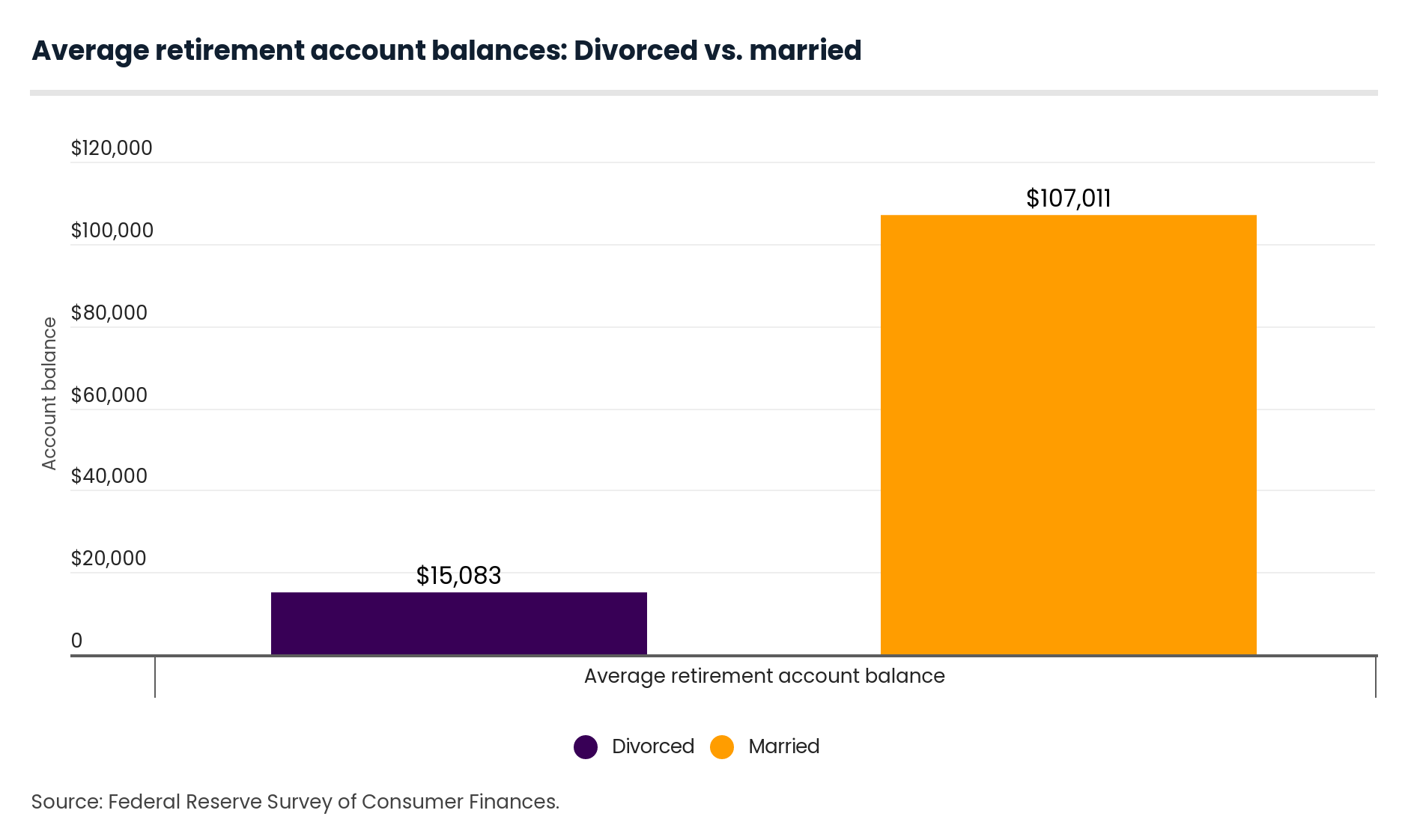

The retirement-preparedness divide is especially wide when looking at the retirement account balances of those who are married compared with those who are divorced. In fact, our study found that married people’s accounts are more than seven times heftier than those of divorced people — an average of $107,011, versus $15,083.

Across the marital-slanted financial board, in general, divorced people tend to come up short when it comes to assets compared with married people:

As for overall wealth, it’s once again divorced people who are often at a financial disadvantage. Married couples have 3.7 times more overall wealth on average than those who are divorced. When taking into account the average assets of married couples ($1,252,854) and average liabilities ($153,995), which includes debts like mortgages, credit cards and auto loans, the average total wealth of married couples is $1,098,859.

In comparison, people who are divorced or separated have an average of $391,322 in assets and $95,484 in liabilities, equaling an average total wealth amount of $295,838.

The average cost of divorce is $12,900, according to a nationwide survey from Nolo, but that can vary based on where you live, whether you have children, how long the divorce takes and other factors. That nearly $13,000 includes attorney fees and other court costs, including real estate appraisers and tax advisors.

While that number can be much higher or lower, it’s often a significant amount, and it may contribute to the common theme we found: When it comes to savings and assets, those who are divorced are lagging behind their married couple cohorts.

Such steep — and likely unanticipated — expenses are likely to take a toll on most people’s finances. Things like retirement savings and the purchase of assets may be put on hold as funds are needed to cover those expenses. None of this is to say that anyone should stay married just to fare better financially, but it’s important for those who are considering a divorce to understand the potential financial impact and to prepare for it as best as possible.

There are often ways to save when it comes to divorce. To lower the potential cost of a separation, we recommend negotiating terms with your spouse before filing, getting a postnuptial agreement and partaking in mediation.

Saving for retirement is important, no matter your marital status. Here are five tips to help.

Analysts analyzed data from the Federal Reserve’s 2019 Survey of Consumer Finances — the latest available data — to examine the financial health of divorced people and married couples. We also used data from the supplementary module of the Survey of Consumer Expectations, collected between 2015 and 2018.

Julie Ryan Evans

Julie Ryan EvansJulie Ryan Evans is a writer and editor who has covered small business, real estate and personal finance for nearly a decade. She has written for an array of publications, including USA Today, Realtor.com, LendingTree and Debt.com.

Read More