MagnifyMoney

Relationships are tricky enough without adding money to the mix. In fact, a 2020 MagnifyMoney survey found that 45% of Americans would rather discuss their weight than their wallet. For young and older couples alike, talking (or not talking) about debt, or about ways to spend or save, can cause tension.

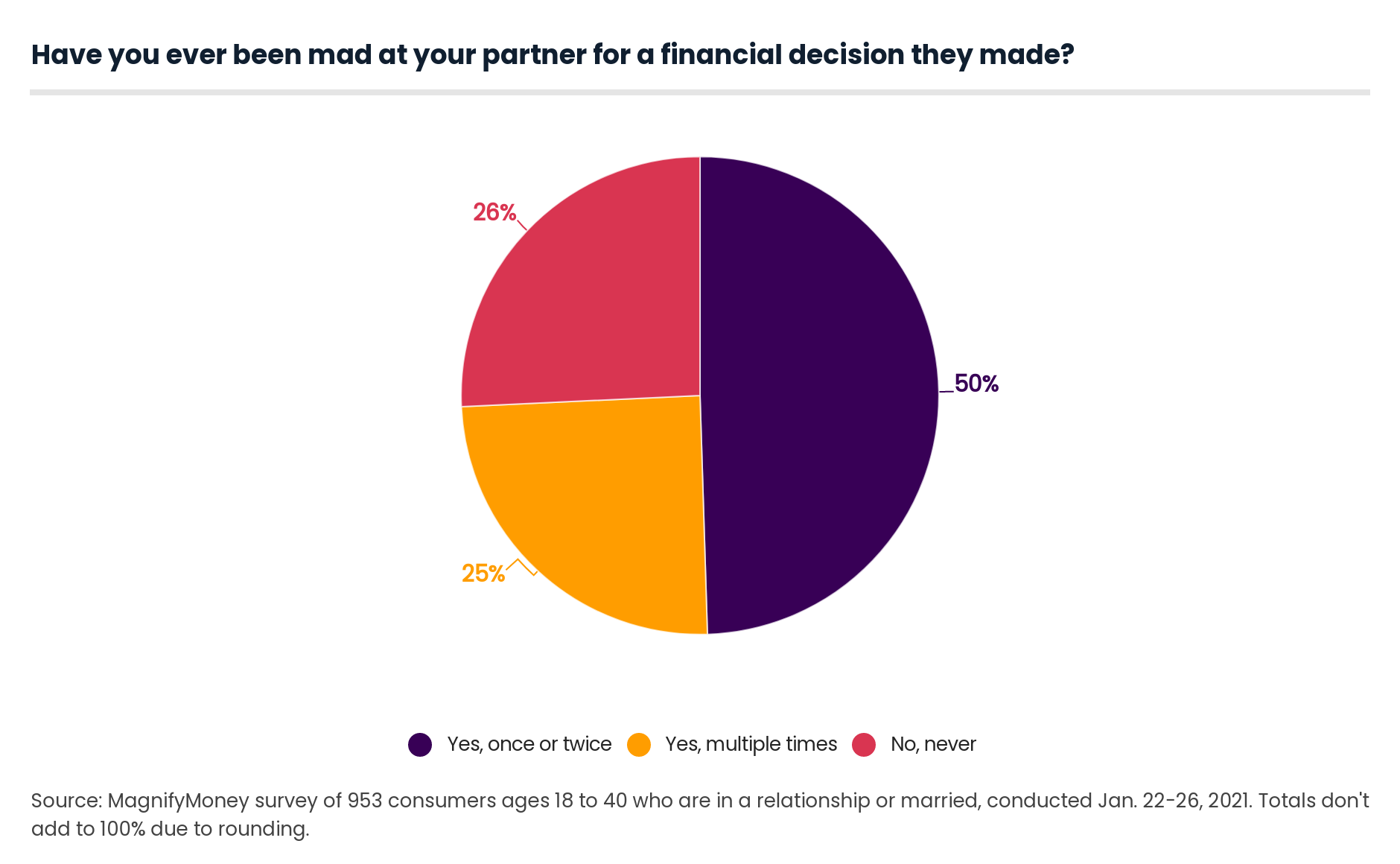

To understand how this impacts younger couples, MagnifyMoney surveyed nearly 1,000 Gen Zers and millennials who are married, engaged or in a relationship. According to our findings, nearly three-fourths said they’d been mad at their partner because of a financial decision they made, while 15% hadn’t yet discussed debt with their partner. Here’s what else we found.

Nearly 3 in 4 millennial and Gen Z couples — which includes married and engaged couples and those in relationships — have been mad at their partner for a financial decision they made:

Those who earned between $50,000 and $74,999 were the most likely (84%) to have been mad at their partner for a financial decision. Conversely, just 16% of that income group said they never felt that way, compared with a range of 22% to 35% in the other brackets.

Among those who said they’d been mad at their partner for a financial decision, the most common circumstances were either that their partner made a big purchase without telling them or the partner spent a lot of money on something they consider frivolous:

Interestingly, older millennials (ages 33 to 40) were most likely to report hiding debt as the financial decision that made them mad at their partner (11%), versus 6% of younger millennials (25 to 32) and 8% of Gen Zers (18 to 24).

We also asked whether a partner had been mad at the survey respondent for a financial decision they made, and 67% said yes. However, there was a variation among gender, as 78% of men said they had made their partner mad at them for a financial decision, versus 58% of women.

As for the reasons why a partner had been mad at a respondent’s financial decision, the top two argument drivers were the same as when the respondent was the one who was mad:

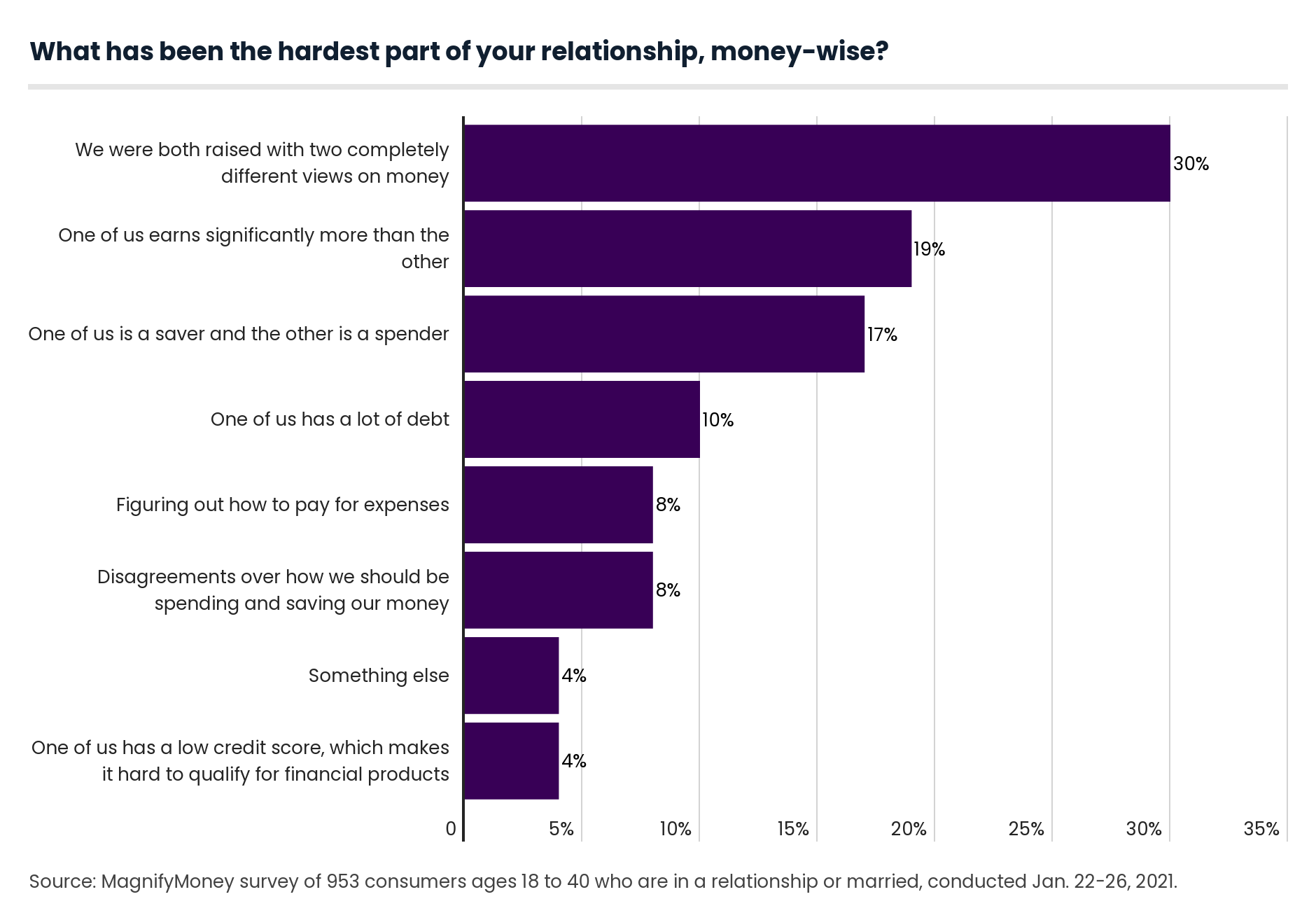

Money can be a source of relationship challenges, and there can be a lot of reasons for that:

For many, the most difficult part of dealing with finances while being a couple came down to being raised with different views on money.

A point of contention could be frivolous spending, said Lauren Perez, a MagnifyMoney deposits writer. With video games, for example, one partner might not agree with the other’s spending decisions because they feel the money could be spent elsewhere.

“Someone who is used to living paycheck to paycheck may not understand the money views of someone who comes from generational wealth and vice versa, which can certainly lead to disagreements,” Perez said.

She also cited the gender pay gap as a potential reason, in which men can make significantly more than women. Among all respondents, 19% said one partner outearning the other was the hardest difficulty.

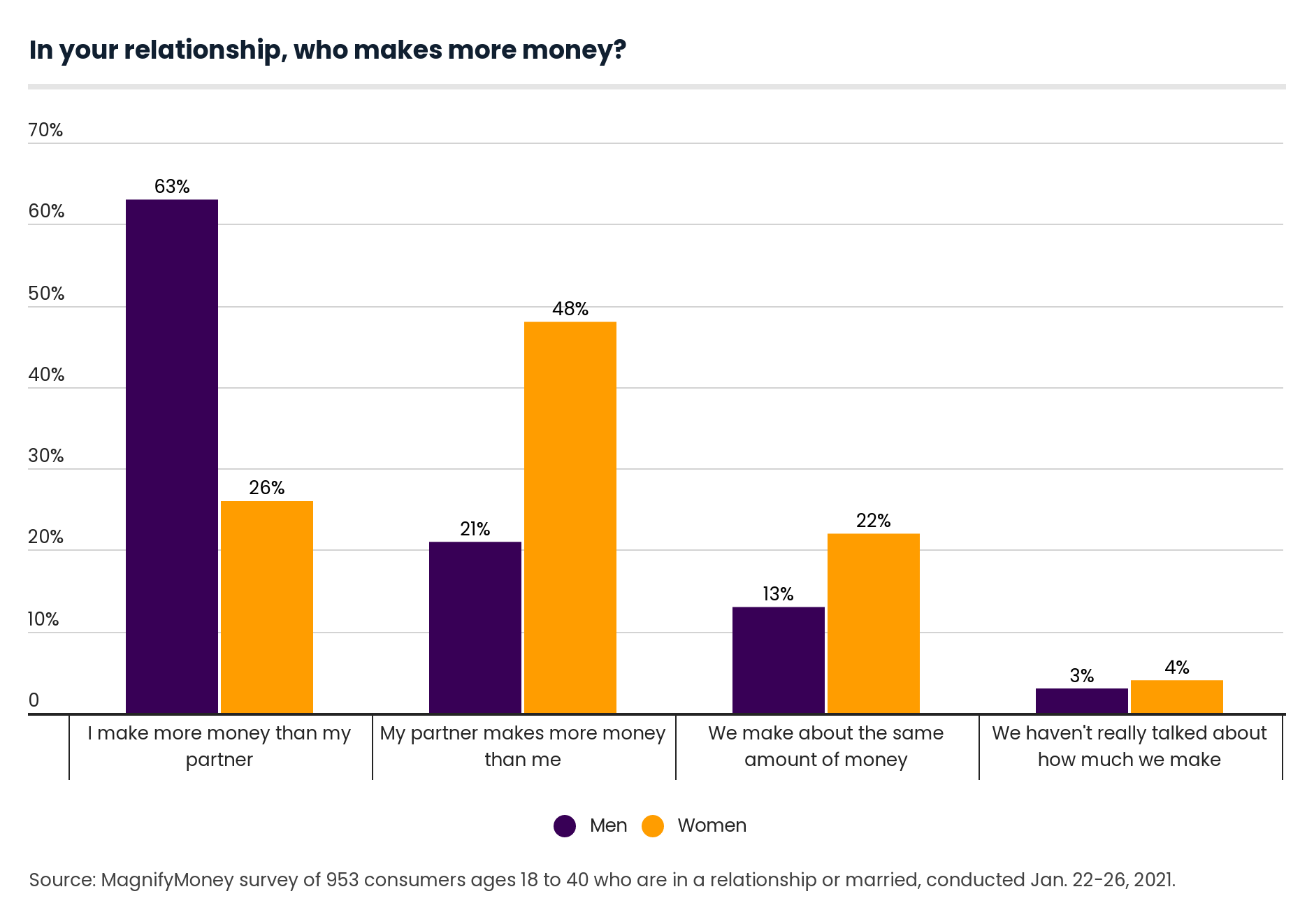

Building off what we just discussed, more than 6 in 10 (63%) men in these millennial and Gen Z couples make more money than their partner, compared with 26% of women.

Older millennials were also more likely to report earning more than their partner (55%), as well as married people (52%) and those earning $100,000 or more a year (66%).

These kinds of earnings differences can cause tension, especially when one partner makes significantly more than the other. In fact, 51% of those in relationships or marriages where one person outearns the other said there has been tension because of it — and men were more likely to say so than women.

Notably, those earning less than $25,000 a year were the least likely to report tension coming from an income difference (40%), while 61% of those earning $100,000 or more said they had experienced this.

Men Have Nearly $1,200 More in Their Checking Accounts Than Their Wives, Live-In Girlfriends

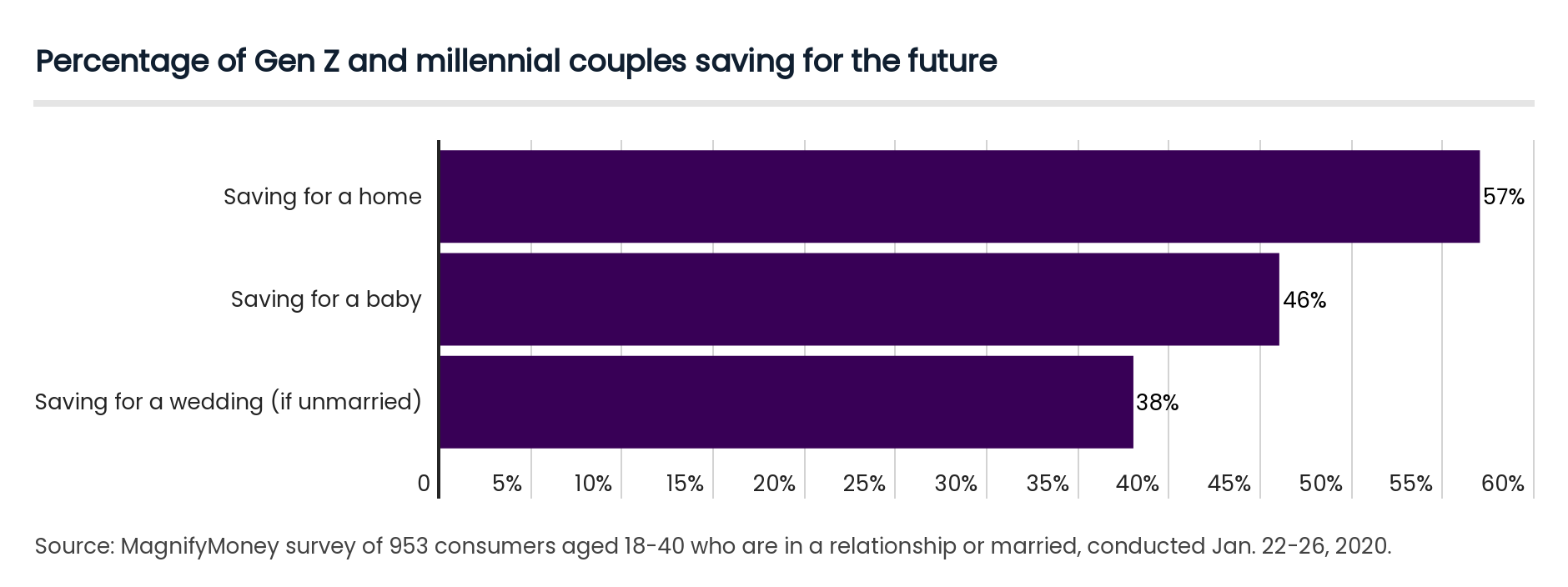

When it comes to saving for a home, baby or wedding, more millennial and Gen Z couples were saving to buy a house (57%):

Younger millennials (60%) are more likely than their older counterparts (56%) to say they’re saving for a house.

Meanwhile, 46% of millennial and Gen Z couples are saving for a baby, but that percentage jumps to 55% for those who are married. And 69% of those earning $100,000 or more also said they were — largest among the income brackets.

Lastly, we asked those who were dating (but not engaged) whether they were saving for a wedding. In total, 38% said they were. Breaking it down further, 67% of those earning $100,000 or more were doing so, versus 26% of those earning less than $25,000.

Talking about debt with a partner is the norm, with only 7% saying they never had — and that they had no plans to do so. However, it is more common among Gen Z couples (10%).

And while about two-thirds (65%) said both partners know all about each others’ debts, 20% noted they haven’t gotten into specifics on how much each person owes. Let’s look at this among those who are married, living together and not living together:

While most married respondents said they didn’t get a prenup — a legal agreement that outlines how assets and debts are handled in the event of divorce or death — about a third did. That figure jumps to 52% for households that earn more than $100,000 a year.

That could signal a change in the perception of this financial tool, which has often been thought of negatively as it kicks in post-divorce. This may be facilitated by the prevalence of talking about finances with a partner in general.

“Although taboo, prenups can be a worthwhile conversation before getting married,” Perez said. “A prenup can help you protect your financial assets, including assets like inheritances and estates. It can also help ensure the financial situation for any dependents the couple might have.”

That could help explain why the prenup trend seems to be gaining more traction. Among those who were engaged, for example, more than half said they were at least considering getting one:

If you and your partner are considering a prenup, it’s important to make sure you specify what it’ll cover. That should include both parties’ assets, including those gained individually before the relationship and any joint assets, like a house, Perez said. And it should also cover any inheritances and trusts, as well as any businesses you may own.

“Not talking about finances may work for some, but couples who don’t discuss finances likely have a tough road ahead,” Perez said. “Relationships require honesty and candor, especially about money, and especially when those finances are coming together. With something as important as money, it pays to communicate and work together.”

While 57% of married couples have joint accounts, 65% of those living together unmarried keep separate accounts.

Among those who have separate accounts and live together, however, the vast majority split the bills in some form:

Still, 53% of these couples also said they’ve fought over who’s paying for what.

If you’re going to get a joint account, it may help to establish its purpose and how each person will contribute to it, Perez said. For example, each person could contribute half their income to the account, which will cover the couple’s rent, utility bills and groceries. Or, perhaps, the person with a higher income will contribute more.

That said, it isn’t always necessary to get joint bank accounts, as it can be easier to track spending by keeping things separate. The most important thing, Perez said, is to understand what your financial and bank account needs are as a couple.

MagnifyMoney commissioned Qualtrics to field an online survey of 1,523 Americans ages 18 to 40, conducted Jan. 22-26, 2021. Of the total sample size, 953 respondents were married, engaged or in a relationship. The survey was administered using a non-probability-based sample, and quotas were used to ensure the sample base represented the overall population. All responses were reviewed by researchers for quality control.

We defined generations as the following ages in 2021:

Devon Delfino

Devon DelfinoDevon Delfino is an independent journalist with work featured in the Los Angeles Times, U.S. News & World Report, Teen Vogue, Forbes, MarketWatch, CNBC and USA Today, among others.

Read More