MagnifyMoney

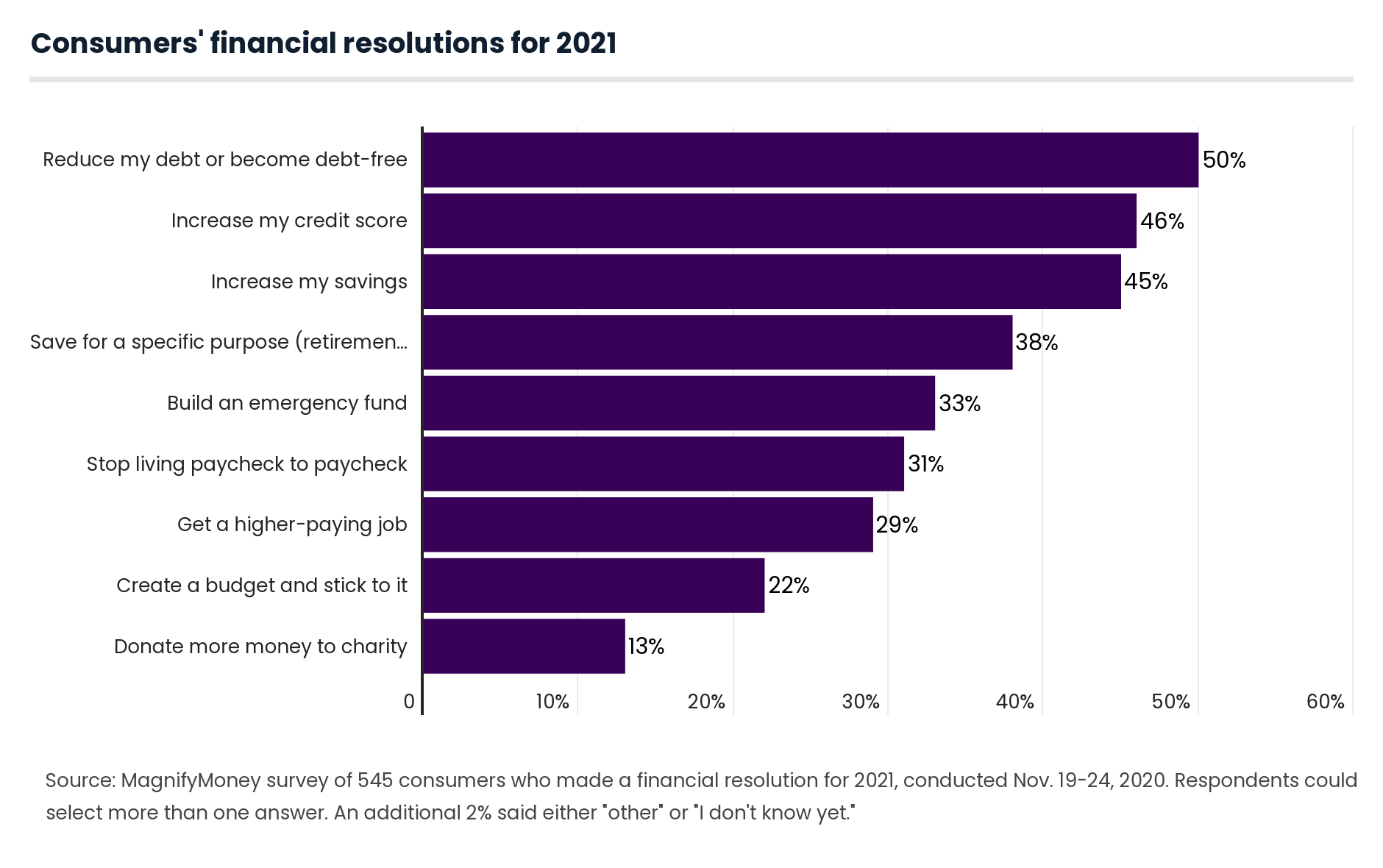

Despite the general chaos of 2020, more than half of Americans will make a money resolution for 2021, and another 16% are undecided, according to the latest MagnifyMoney survey. Among those planning a 2021 money resolution, about half said they want to reduce debt or become debt-free.

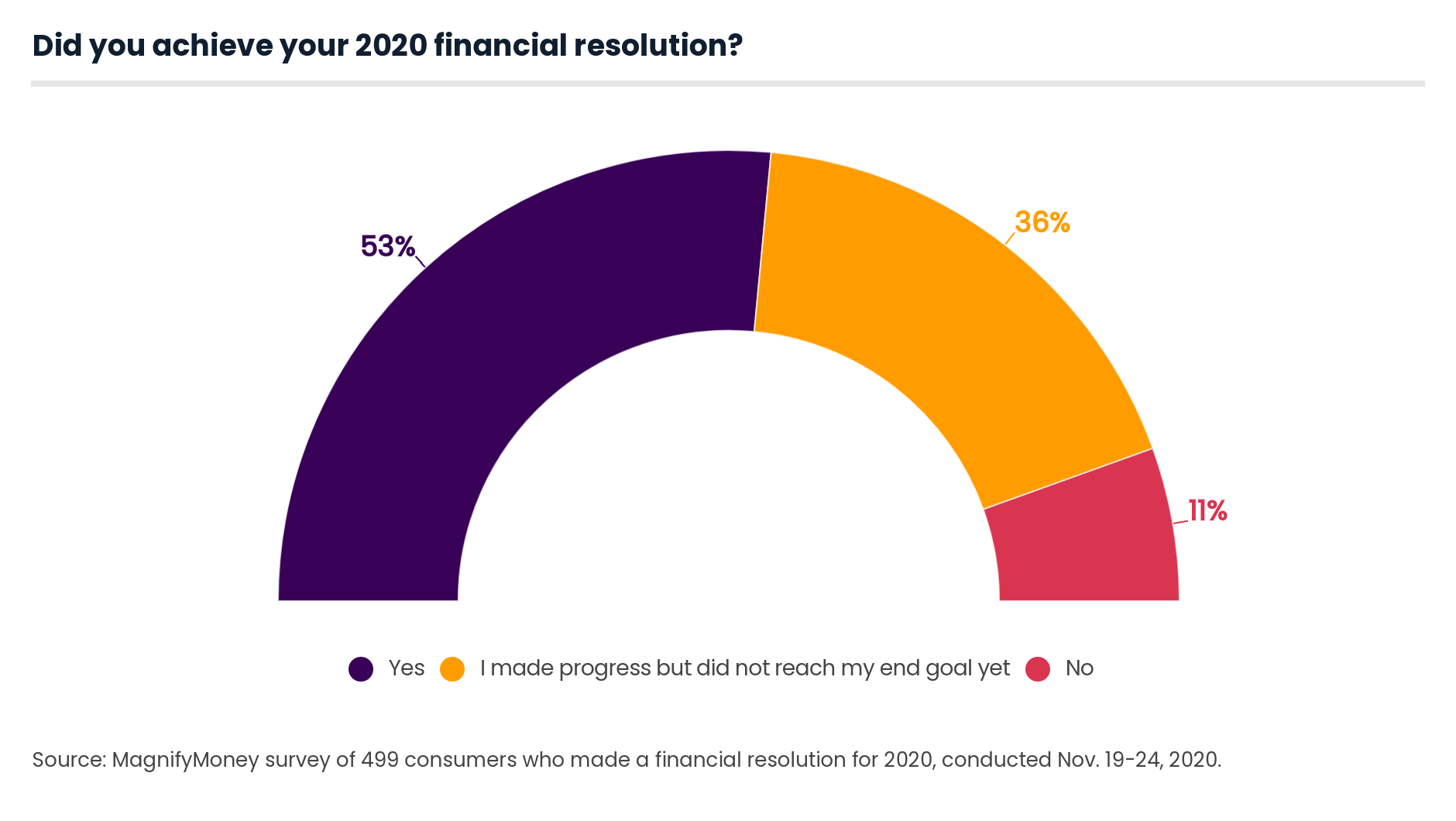

In light of the COVID-19 pandemic, we also looked at how people did with their 2020 money resolutions. According to our survey of more than 1,000 Americans, 53% of those who set a money resolution for 2020 achieved it, and another 36% have made progress.

Here’s what else we discovered.

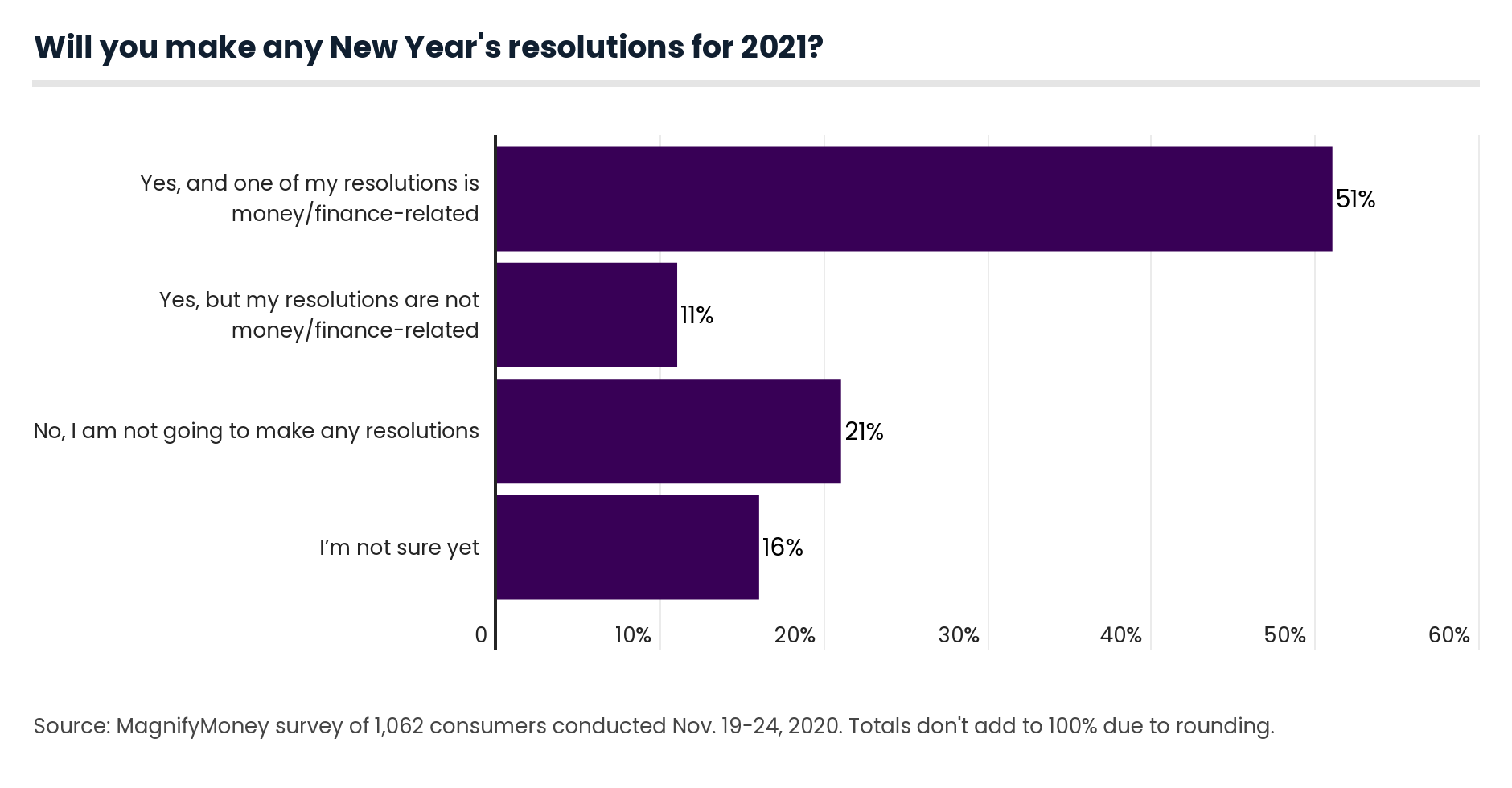

More than half (51%) of Americans will make a money resolution for 2021, while 21% say they won’t make any resolutions at all.

Among the generation groups, millennials have the highest percentage (62%) of Americans planning to set a financial resolution for the upcoming year.

“Many millennials are reaching the point in their lives where major milestones are on the horizon, such as marriage, buying a home or starting a family,” said Sarah Berger, MagnifyMoney’s millennial finance columnist. “Setting financial goals is a critical component to being able to pay for those milestones, even if they are still a few years away.”

Gen Zers and Gen Xers followed close behind at 58% and 55%, respectively, compared with just 21% of baby boomers.

Financial goals seem to be more popular among those who earn more and have more education. For example, 64% of those with at least a four-year college degree said they intended to set a money goal, versus 45% of those with some college and 43% with no college.

Resolution-setting is popular in the U.S., and Americans will have various resolutions for 2021.

“New Year’s resolutions are all about improving and feeling better about yourself,” said Matt Schulz, LendingTree chief credit analyst. “The truth is that little makes people feel better about themselves than getting out of debt. That’s why it is always one of the most common resolutions each year, along with improving your health.”

Half of Gen Zers said their main goal is to get a higher-paying job, while about half of millennials and Gen Xers (as well as 58% of baby boomers) cited reducing debt or becoming debt-free as their top financial goal for 2021. Younger generations have had less time to take on debt — and a higher income could be their answer to getting out of any debt they do have. Older generations may be retired and living on a fixed income, making debt more difficult to overcome.

Among those who said they wanted to save for a specific purpose, the most common goals were:

In general, people are optimistic about their upcoming resolutions. A little less than half (48%) of Americans think they’re extremely likely to achieve their 2021 resolution, and 42% think they’re somewhat likely. There is, however, a rather wide gender split here, as 60% of men said they’re extremely likely, while only 37% of women said the same.

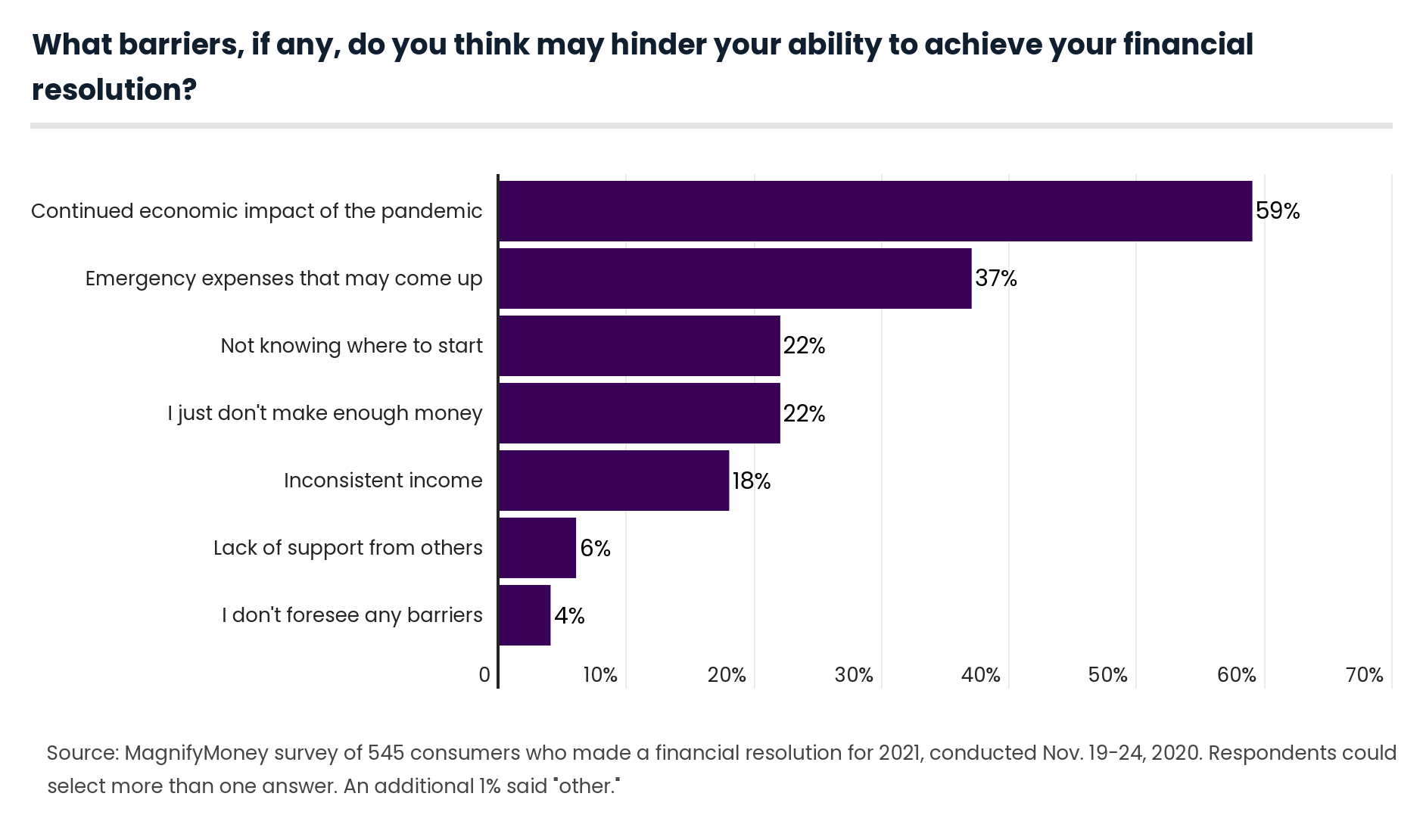

Of course, optimism and achieving a goal are two separate things, so it pays to plan for the worst, as 97% of resolution setters acknowledged. And the top obstacle cited was continued economic impact from the coronavirus pandemic (59%).

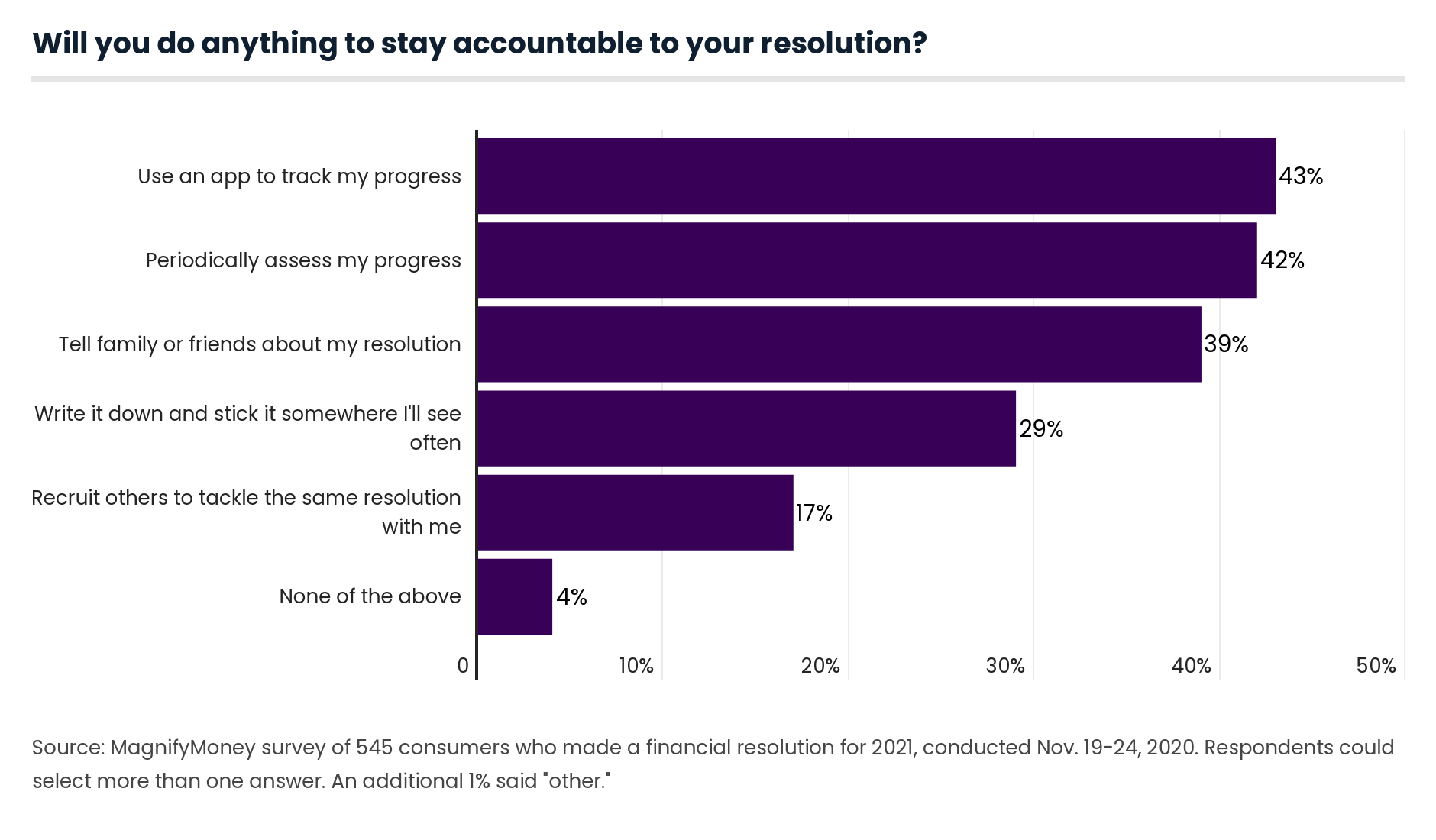

While the pandemic remains the chief concern across generations, 49% of baby boomers cited potential emergency expenses as an obstacle. To combat potential obstacles, many consumers said they’ll take action to stay accountable.

“Apps can be useful, but there are privacy and security concerns with apps that have your financial information,” said Ken Tumin, founder of DepositAccounts.

One alternative, Tumin said, is to choose a digital bank — such as Simple or Empower — that offers budgeting features in their mobile banking apps.

Check out MagnifyMoney’s list of best online banks

Of the 47% of consumers who made a financial resolution at the beginning of 2020, 53% achieved the resolution. And an additional 36% have made progress but haven’t reached their end goal.

Millennials (56%) had the best luck achieving their financial goals in 2020, while baby boomers (23%) had the least luck. (This is perhaps unsurprising as baby boomers were also less likely to set financial goals in 2021.)

The most common financial resolutions in 2020 were:

Unlike 2021, Gen Xers (48%) were the most likely generation in 2020 to cite reducing debt or becoming debt-free as their financial resolution. In 2020, millennials (42%) were most focused on increasing their credit score.

Of those who achieved their 2020 money resolution, the majority (70%) did so by the summer, despite the impact of the COVID-19 crisis. And among those who haven’t yet achieved their 2020 resolution, 83% said they will continue to work on it in 2021.

The pandemic’s impact has been widespread. Unfortunately, that also means it’s impacted people’s resolutions. In fact, 62% of those who set a 2020 resolution changed it because of the crisis. The way that plays out can vary widely based on individual circumstances.

One respondent wrote that they had originally resolved to stop living paycheck to paycheck, but ended up changing the resolution to simply survive. Another respondent initially hoped to increase their income, but later resolved to just keeping their income stable.

Job status is closely tied to how the pandemic impacted finances and resolutions. For instance, the following segments said they changed their money resolutions because of the pandemic:

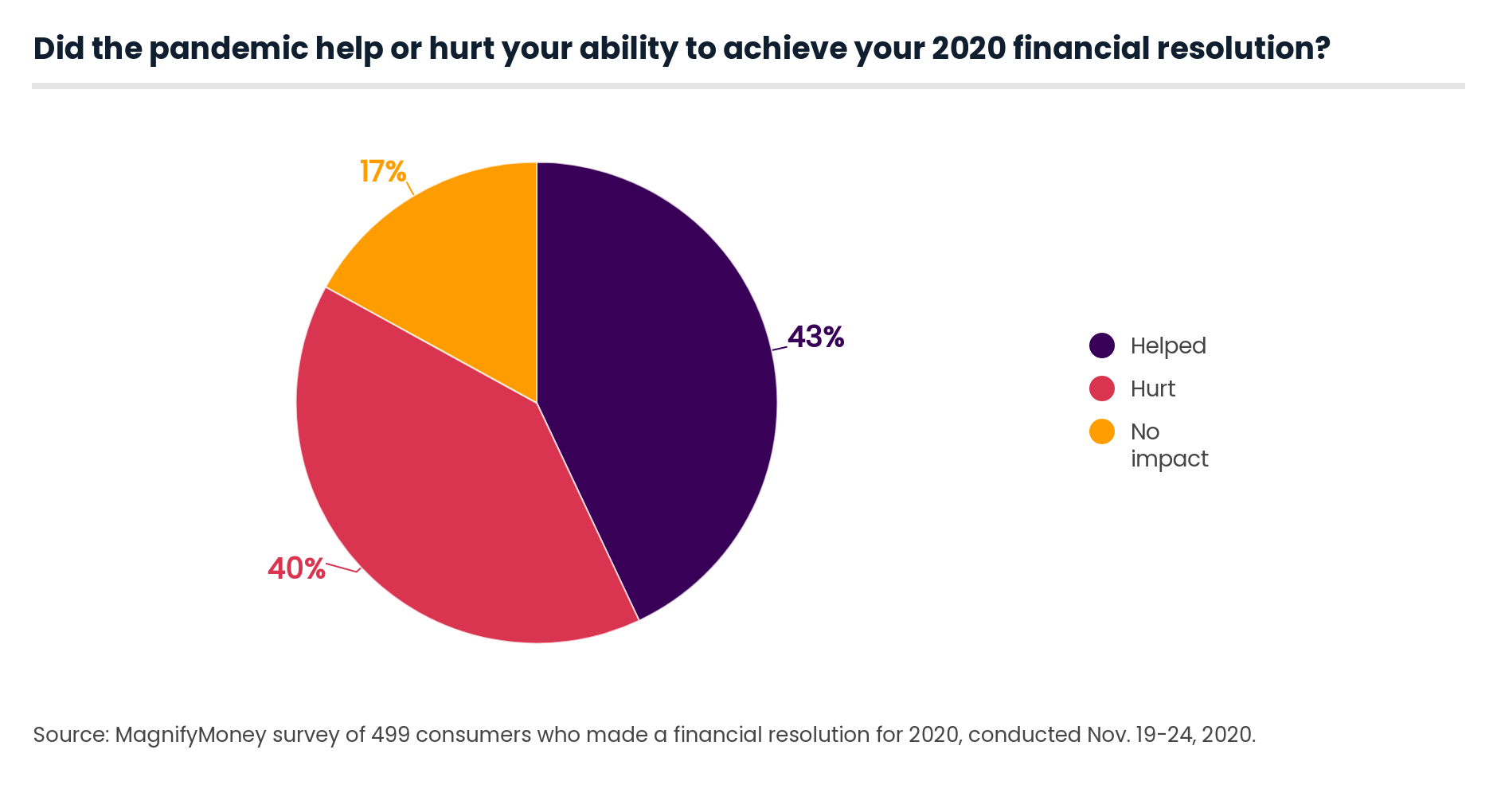

Despite this, 43% said the pandemic helped their ability to achieve their 2020 resolutions as they were able to save more money through reduced spending, economic impact payments and enhanced unemployment benefits. But 40% said the pandemic has hurt them, resolution-wise, because of a loss of income.

While those with a higher income tended to be impacted less severely by the pandemic in general, 23% of those earning less than $25,000 said the pandemic didn’t have any impact on their financial resolutions — the highest among any group.

Of course, whether you lost your job or had medical issues will dictate how the pandemic impacted your overall resolutions, as well as your finances.

“Those who were able to keep their jobs and avoid contracting the virus may have found that the pandemic helped their resolutions,” said Tumin, noting that reduced travel and entertainment expenses could also be a helpful factor. “The low-interest rate environment that took hold when the pandemic began has made it possible for people to save money by refinancing mortgages and other loans. All of these may have made it easier to accomplish money resolutions this year.”

Check out MagnifyMoney’s list of best savings account rates

MagnifyMoney commissioned Qualtrics to conduct an online survey of 1,052 Americans, with the sample base proportioned to represent the overall population. The survey was fielded Nov. 19-24, 2020.

We defined generations as the following ages in 2020:

While the survey also included consumers from the silent generation (defined as those 75 and older), the sample size for that group was so small that findings related to that group weren’t included in the generational breakdowns.

Devon Delfino

Devon DelfinoDevon Delfino is an independent journalist with work featured in the Los Angeles Times, U.S. News & World Report, Teen Vogue, Forbes, MarketWatch, CNBC and USA Today, among others.

Read More