MagnifyMoney

Patience is a virtue, especially when it comes to the stock market. As much as we might feel compelled to jump ship when we see headlines about pandemics, invasions, Supreme Court rulings, insurrections and thousand-point market declines, usually your best move is to stay the course, confident that better times will come.

However, a new MagnifyMoney survey shows that’s been far easier said than done for millions of Americans in the past year. About 4 in 10 investors (38%) say they’ve pulled money from the stock market in the past year in response to current events — and of that group, 40% say they regret their decision.

This survey was fielded through April 20, 2022: On that day, the Dow Jones Industrial Average closed at 35,160.79. Less than three weeks later, the Dow sat at 31,834.11, losing more than 3,000 points.

Those numbers are a classic example of what this survey is about. It’s perfectly rational to react to these types of declines by wanting to get out of the market and cut your losses. However, for most of us — those in it for the long haul, aiming to build wealth through the stock market in hopes of perhaps retiring or owning a home someday — it’s best to hang in there. As hard as it may be, it’s likely the best move for your financial future.

While nearly 4 in 10 (38%) investors say they pulled some money out of the stock market in the past year due to current events, some consumers were far more likely to have done so. Unfortunately, this includes folks who would be best served by leaving their money in: younger investors.

Two-thirds of Gen Z investors ages 18 to 25 (67%) and over half of millennial investors ages 26 to 41 (57%) took money out of the market, compared with just 28% of Gen X investors ages 42 to 56 and 12% of baby boomer investors ages 57 to 76.

This is troubling, as time is an enormously powerful asset in investing. Gen Z and millennial investors have decades ahead of them to let compound interest work its magic and ride out the market’s ups and downs. While markets are inherently volatile, they tend to rise over the long term. However, by panicking and pulling money out of the market during a downturn when they’re young, these investors risk missing future upswings in the market, potentially costing themselves thousands of dollars in lost funds over the years.

As far as regrets, millennials were most likely to have them, with 45% of those who pulled money out saying they wish they hadn’t. The same was true for 39% of Gen Zers, 29% of Gen Xers and 22% of baby boomers.

Meanwhile, men are far more likely than women to have withdrawn their money (49% versus 24%). Among those who had taken out money, men were more likely than women to say they regretted doing so (44% versus 29%). That shouldn’t be surprising, given that MagnifyMoney data has typically shown women to be more cautious about their finances than men.

Current events don’t just affect our views of the stock market: They can help shape our thoughts and actions in virtually every aspect of our financial lives. Our survey shows that this has happened for most Americans in recent years.

Seven in 10 Americans say world news and current events have factored into their financial decisions or money management choices. Those with annual household incomes of $50,000 to $74,999 (80%), Democrats (77%), investors (77%) and millennials (76%) are most likely to say so.

Which specific events have had the biggest impact in the past year? Not surprisingly, the rapid growth of inflation and the pandemic.

Still, inflation and COVID-19 were far from the only news stories impacting Americans’ financial decisions. Others included changes in U.S. economic policy, the Russian invasion of Ukraine and climate change. However, among all age groups, income levels and genders, inflation and the pandemic were the top two concerns.

By far, the aspect of people’s finances that was most impacted by current events in the past year was their emergency funds. Nearly half (46%) of those who say current events had impacted a financial decision in the past year were more likely to focus on building an emergency fund.

The most likely to say they focused on building an emergency fund? Gen Xers and baby boomers — at 51%. Meanwhile, Gen Zers (29%) and millennials (27%) were most likely to say current events had affected their living situation or plans to buy or sell a home.

People’s investment choices were impacted as well. More than a third (34%) of those who said that current events affected their financial choices noted an impact on the amount of money they invest, 20% say it affected the level of risk in their investments and 16% report an effect on their purchases or sales of specific stocks.

Not all news is created equal — some events happen out of the blue, with no warning, while others can be seen coming. Rate movements by the Federal Reserve tend to fall in the latter category.

When the Fed raised the federal funds target rate by 50 basis points in early May, virtually every observer expected it. In the weeks leading up to the increase, there was debate about how much rates would go up — a quarter of a percentage point, a half-point, maybe even three-quarters of a point — but there was no question that it would go up. And in the final days leading up to the announcement, even the mystery around the size of the jump had faded, with virtually every observer rightly expecting a half-point increase.

These rate increases generally make borrowing more expensive for consumers, impacting the cost of credit cards, mortgages, personal loans, auto loans and more, to varying degrees. While any rate increase is unwelcome for those with card debt, the predictability around these increases means people can prepare for them in advance — as long as they know about them. And our survey indicates that half of consumers do.

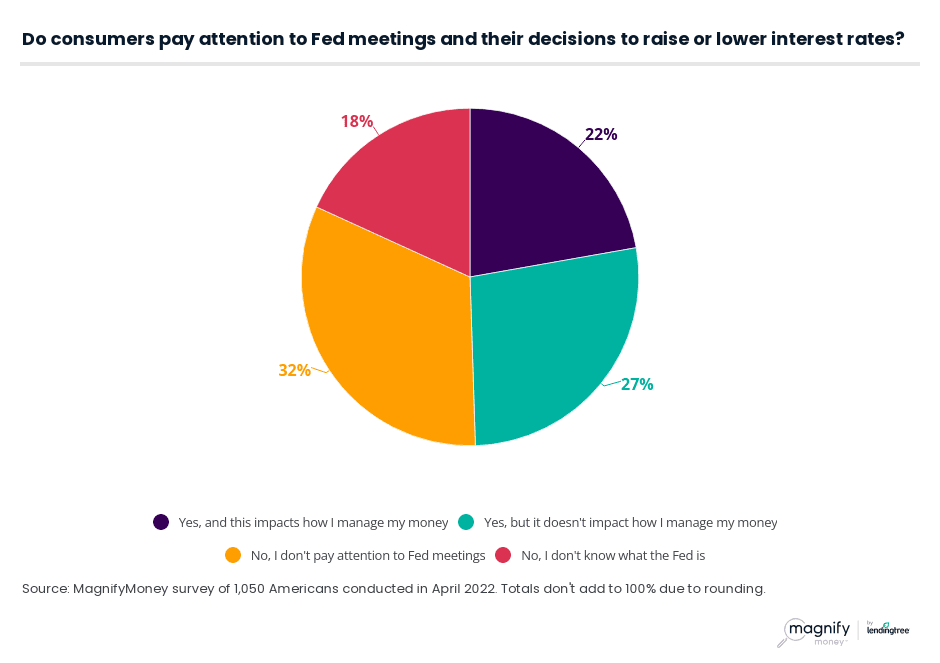

Half of consumers say they pay attention to news about Federal Reserve meetings, including 22% who say the Fed’s moves impact how they manage their money. That’s important, since those folks can take action to lower their interest rates — applying for a 0% balance transfer credit card, getting a low-interest personal loan, calling their card issuer to request a lower interest rate are among their options— before the Fed pushes them higher.

Unfortunately, another 50% don’t pay attention to Fed meetings, including 18% who say they don’t know what the Federal Reserve is.

The last few years have been exhausting and challenging for most everyone. Yet, we’ve all found ourselves watching too much cable news, doom-scrolling through social media and generally being swept up in the latest troubling news story. Given that, it’s no surprise that so many of us have let the day’s events impact our financial decisions.

The problem is that money and emotion are a volatile mix. People tend to make bad financial decisions when emotions play too big a role, which is likely the case for many of the folks we surveyed. Instead of trying to protect themselves and limit their losses, they’re likely increasing them, as they’ll miss out on future growth that could be far greater than any losses they’ve suffered.

However, we also know that standing pat when the market is plunging may be difficult to follow through on. Here are some tips on keeping your cool when tough times hit the market:

RELATED: Younger Americans have been abandoning savings bonds and CDs for 30 years, turning more to stocks

MagnifyMoney commissioned Qualtrics to conduct an online survey of 1,050 U.S. consumers, fielded April 15-20, 2022. The survey was administered using a nonprobability-based sample, and quotas were used to ensure the sample base represented the overall population. All responses were reviewed by researchers for quality control.

We defined generations as the following ages in 2022:

While the survey also included consumers from the silent generation (those 77 and older), the sample size was too small to include findings related to that group in the generational breakdowns.

Matt Schulz

Matt SchulzMatt Schulz is a personal finance expert who has been quoted in or appeared on Good Morning America, NBC Nightly News, the Wall Street Journal, the New York Times and other reputable outlets.

Read More